Source: Guojun Overseas Macro Research

Author: Zhou Hao, Sun Yingchao

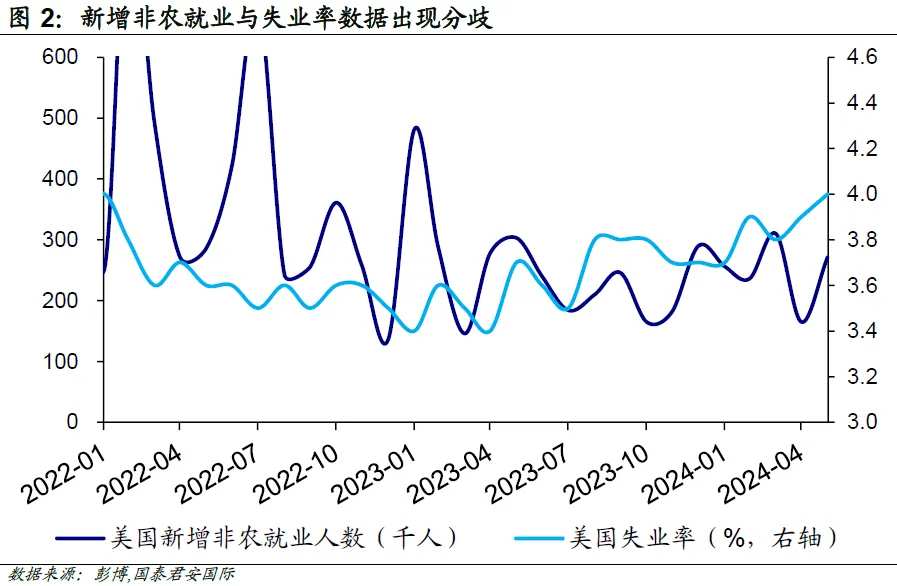

Recently, the conflict between employment data has not brought a clearer direction to the market. Looking ahead, the market's attention has now shifted to this week's inflation data and the Fed's interest rate meeting. Due to the recent sharp drop in oil prices, the May CPI data should cool down to some extent, which will alleviate the market's concern about inflation. In terms of product structure, the operating income of products valued between 10 and 30 billion yuan were respectively 401/1288/60 million yuan.

The weather is good today

The weather is good today.

Please use your Futubull account to access the feature.

Considering the unclear outlook for inflation in the short term, the Federal Reserve will most likely adjust its interest rate guidance for the whole year to be in line with market expectations (2 rate cuts). In addition, the probability of a rate cut by the Fed in July is already very low, and the market is more focused on the September monetary policy meeting.

Do not underestimate the resilience of the US economy, nor the resilience of US stocks. This seems to be the biggest revelation the market gave us last week. Since the end of May, the performance of US economic data has been generally sluggish. The revised GDP for Q1, the ISM manufacturing index, JOLTS job openings, ADP employment figures, etc. were all below expectations. The continuous cooling of economic data has once again ignited the market's desire for a rate cut, but the Non-Farm payrolls report that was released last Friday (June 7) greatly exceeded expectations, forcing investors to lower their bets on a rate cut in September.

Overall, there are still some issues worth discussing in the May Non-Farm Payrolls report. For example, in the case of a significant increase in new jobs, the unemployment rate has slightly risen above the 4.0% threshold. We believe that there may be two factors that have led to this conflict: (1) the proportion of multiple job holders has increased, which has led to a significant increase in the number of new jobs; (2) the increase in immigration (including illegal immigration) has led to an expansion of the employment population, so while the employment population is rising, the overall unemployment rate is also rising. However, from a different perspective, an increase in immigration is a good thing, not only beneficial for consumption, but also helpful in reducing inflation.

The conflict between employment data has not brought a clearer direction to the market. Looking ahead, the market's attention has now shifted to this week's inflation data and the Fed's interest rate meeting. Due to the recent sharp drop in oil prices, the May CPI data is expected to cool down compared to previous figures, which may relieve the market's concerns about inflation. From these data, it seems that the market should not be overly optimistic or too pessimistic about the US economy. The trend of US treasury yields also reflects this, the softness of the data pushed the 10-year treasury yield to a low of below 4.3% before Friday, but after the Non-Farm payrolls report was released, it directly rose by several tens of basis points to above 4.45%.

Unexpectedly, the US stock market has shown extreme stability during this period, continuing to rise during the few days when interest rates were lowered. Although interest rates have since risen rapidly, US stocks only fell slightly at the close. All in all, the US stock market has shown a trend of taking two steps forward and one step back, proving that it is still a market that investors favor very much.

Regarding Europe, the European Central Bank announced a 25 basis point rate cut at its June interest rate meeting, consistent with market expectations. In addition, the Bank of Europe gave a hawkish and vague indication, stating that it would not make any specific forecasts on the path of interest rates, and that it will depend on the situation in September. Against the backdrop of rising inflation in the eurozone, the cautious remarks of the European Central Bank are reasonable. The forward-looking guidance also indicates that the European Central Bank does not have a grasp on the future direction of the economy and inflation, which is also the current attitude of major central banks around the world: in today's era of unpredictable inflation, vague guidance and dynamic adjustment appear to be an inevitable choice.

In the upcoming Fed interest rate meeting this week, the latest dot plot and economic growth forecasts will be released. Under normal circumstances, the Fed is likely to adjust its interest rate reduction guidelines for the whole year to be in line with market expectations (i.e., around two interest rate cuts) and at the same time demonstrate its determination and patience to control inflation. Under this expectation, the probability of a rate cut by the Fed in July is extremely low, and the market's focus is more concentrated on the September interest rate meeting. Powell is also likely to reiterate that the interest rate hike cycle has ended, and that whether a rate cut will occur in September still depends on more data, etc.

The foreign exchange and interest rate markets are unlikely to gain much nutrition from the Fed interest rate meeting this week. Similar to the rise and fall of the euro before and after the European Central Bank's interest rate meeting, the market has basically digested the relevant information and closed its previous positions after the "shoe drop". Overall, in a foreseeable future, foreign exchange traders are likely to choose range-bound trading, and both the US dollar index and the euro will maintain a moderate upward trend. Under this circumstance, the main driving force for the rise of the US dollar index is actually the yen, which has a low weight but has fallen sharply.

Editor/Somer