Cui Dongshu, Secretary-General of China Passenger Car Association, said that the "price war" has slowed down since May. The domestic auto market is expected to return to the normal state of being promotion-oriented, and it is unlikely to see situations where prices are easily reduced by 20%.

With the introduction of the policy execution details at the end of April, the new car price war in the automotive market has temporarily cooled down, and the accumulated consumption purchasing power was released in May. The China Passenger Car Association predicts that the car buying enthusiasm in June is expected to continue, and there may be a good increase on a month-on-month basis.

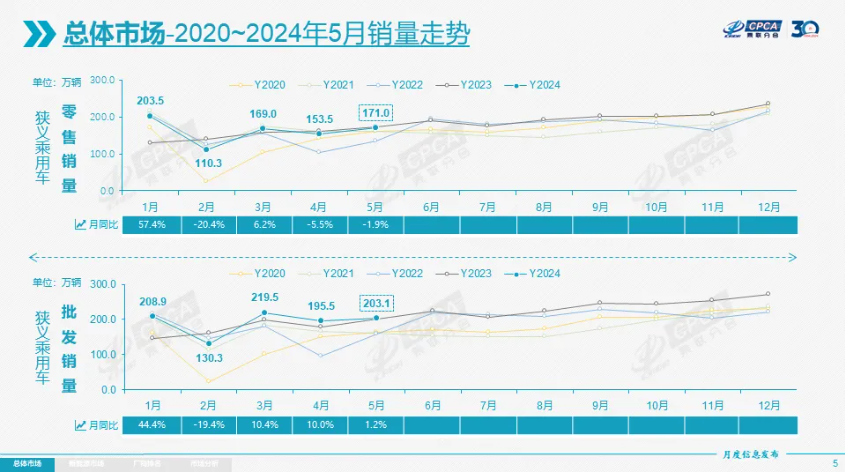

On June 11, the China Passenger Car Association released the analysis report of the passenger car market in May. In May, the national retail sales of passenger cars were 1.71 million units, a year-on-year decrease of 1.9%, and a month-on-month growth of 11.4%. Since the beginning of this year, the cumulative retail sales were 8.073 million units, a year-on-year increase of 5.7%.

In May, the retail sales of new energy vehicles were 804,000 units, a year-on-year increase of 38.5% and a month-on-month growth of 18.7%. The export of new energy vehicles in May was 94,000 units, a year-on-year decrease of 4.0% and a month-on-month decrease of 18.8%. The domestic retail penetration rate of new energy vehicles in May was 47.0%, an increase of 14 percentage points from the 33% penetration rate in the same period last year.

The China Passenger Car Association pointed out:

In May, the national economy operated steadily. Although affected by factors such as the holiday mismatch and the high base of the same period last year, with the implementation of the national policy of "replacing the old with the new", the Beijing Auto Show stimulates consumers' enthusiasm for consumption, various local policies are introduced and followed up, and the price war of new automotive products has temporarily cooled down. The policy of guaranteeing repurchase further dispels users' concerns.

The heavyweight product launch of leading companies has driven the stable expectation of product supply. The consumption enthusiasm of the market observation group in the early stage has been stimulated, and the national new energy passenger car market in May has entered a relatively good development stage.

In addition, the China Passenger Car Association stated that exports continue the strong growth trend at the end of last year. In May, exports increased by 30% year-on-year to 569,000 units. Manufacturers' inventory adjustment remained stable. Due to relatively cautious production by manufacturers in May, but with retail sales warming up, there has been a trend of de-stocking with manufacturers' output of less than 30,000 units.

In May, the sales of new energy vehicles increased by 38.5% year-on-year, and the domestic retail penetration rate of new energy vehicles was 47.0%.

Regarding new energy vehicles, the production and sales growth rate of new energy passenger vehicles in May increased, while exports declined:

In May, the production of new energy passenger vehicles reached 881,000 units, a year-on-year increase of 31.0%, and a month-on-month increase of 9.9%.

In May, the sales of new energy vehicles in the domestic market was 804,000 units, a year-on-year increase of 38.5% and a month-on-month increase of 18.7%.

In May, the export of new energy vehicles was 94,000 units, a year-on-year decrease of 4.0% and a month-on-month decrease of 18.8%.

In May, the domestic retail penetration rate of new energy vehicles was 47.0%, an increase of 14 percentage points from the 33% penetration rate in the same period last year.

From the monthly domestic retail market share, the retail market share of mainstream domestic brand new energy vehicles in May was 71%, a year-on-year decrease of 2.1 percentage points;

The market share of new energy vehicles of joint venture brands was 4.5%, a year-on-year decrease of 0.1 percentage points;

The market share of innovative brands was 16.3%, and brands such as Xiaomi Motors drove the year-on-year increase of the market share of innovative brands by 3.5 percentage points; the market share of Tesla was 6.4%, a year-on-year decrease of 0.5 percentage points.

Regarding exports, the China Passenger Car Association stated that although it has recently been affected by some interference from external countries, the long-term prospect of the new energy export market is still good:

From the monitoring data of retail sales of overseas markets exported by domestic brands, A0-class electric vehicles account for nearly 50%, which is absolutely the main force of independent exports. Independent brands such as SAIC performed well in Europe, and BYD rose in markets such as Southeast Asia and South America.

In addition to the excellent performance of traditional export automakers, the export of new players has gradually increased, and data in overseas markets has also begun to emerge.

In addition, according to the China Passenger Car Association report, from January to April 2024, the world's automobile sales reached 28.36 million units, and the world's new energy vehicles reached 4.49 million units. The penetration rate of new energy vehicles in the world from January to April 2024 reached 15.8%, of which the penetration rate of pure electric vehicles reached 10.4%, and plug-in hybrids reached 5.4%.

From January to April, the profit margin for autos was 4.6%, and there was a temporary cooling in the "price war" phase in May.

The China Association of Automobile Manufacturers (CAAM) said that the auto industry's profit margin remained at 4.6% from January to April, with increased business pressure for enterprises:

In April, as macroeconomic policies were implemented and market demand continued to recover, the effects continued to show. From January to April 2024, the auto industry's revenue was 3.0742 trillion yuan ($474.4 billion), up 8% YoY; costs were 2.6882 trillion yuan, up 8%; profit was 142.8 billion yuan, up 29% YoY; and the profit margin for the auto industry was 4.6%, which is still relatively low compared to the average level of 5% for the entire industrial sector.

In the first four months of 2024, the auto industry benefited from a low base period, but intense competition caused profits to decline sharply for most companies, with profit mainly coming from exports and high-end deluxe models.

Domestic effective demand is still insufficient, and the external environment is still complex and severe. Although profitability still exists with gasoline cars, the market is contracting rapidly, while electric vehicles are growing rapidly but still incurring large losses. This contradiction increases the pressure on enterprises to operate.

CAAM stated that the new car price war in May resulted in a temporary cooling trend, and the policy of minimum vehicle repurchases further dispelled consumer concerns. Regarding the fierce price war in China's auto industry, Cui Dongshu, secretary-general of CAAM, said:

From January to May 2024, nearly 60 electric vehicle models saw price reductions, making it a rare price war. The background of the "price war" is the decline in raw material prices for new energy vehicles, the rapid introduction of new products and the penetration rate of new energy vehicles exceeding 40%.

"Price war" reflects systemic capability and is an inevitable stage in industry development. After May, there has been a tendency for the auto market to return to its normal state of promotion-focused sales, without the occurrence of price cuts of 20% or more.

Vehicle sales in June are expected to continue to grow, achieving good MoM growth:

In anticipation of June, CAAM expects continued demand for vehicle purchases:

June has 19 business days, two fewer than last year, which is not conducive to the mid-year sales rush. With the passenger car market entering the final stage of the year, localities and automakers are striving for strong sales performance. Along with the rapid increase in the capability of manufacturing systems with the delivery of new models, there will be fast release of production capacity, seizing the opportunity. Therefore, June is still a month of good sales.

In 2024, the number of university entrance exam candidates reached 13.42 million, a historical high, which will lead to a surge in demand for driving lessons and tourism after the exam. Moreover, with the improvement of the Third Space experience for intelligent new energy vehicles and the stable expectation of comprehensive usage costs, self-driving in the summer will reach new heights, and personalized, low-cost travel methods such as private car driving will become the choice of more people.

The spring discount season for new cars has ended, and electric vehicle license plates in Beijing were issued at the end of May, triggering a renewal of the market and contributing to the continuation of high demand for vehicle purchases in June.

CAAM also pointed out that the continuing low consumption of gasoline cars is an important factor inhibiting a comprehensive recovery of the auto market. Effective policies such as exchanging old cars with new ones reasonably guarantee the purchasing needs of gasoline car consumer groups, which is of great significance for the smooth development of the auto market. The government's comprehensive consideration for "promoting consumption and boosting internal demand" is becoming increasingly clear and accurate. Gradually releasing the consumer potential for "eliminating old and bringing in new" and "substitutional commerce" will be beneficial for the gradual strengthening of the auto market in the coming months.

In terms of exports, CAAM expects good momentum to continue:

From January to May 2024, Chinese-branded cars exported to overseas markets showed YoY retail sales growth of 57%, and in May, sales growth of Chinese-branded cars to overseas markets reached 57% YoY, continuing to show a strong trend. From this, CAAM predicts that China's passenger car exports will continue to grow in June and drive continued YoY growth in domestic and foreign sales volume.

Editor/new