WalkMe Ltd. (NASDAQ:WKME) shareholders have had their patience rewarded with a 70% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 48%.

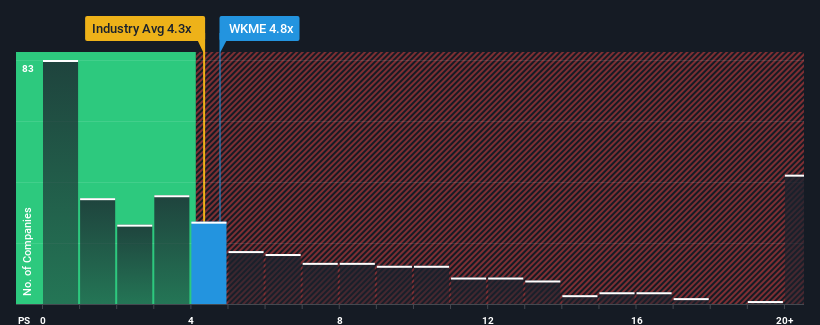

Although its price has surged higher, you could still be forgiven for feeling indifferent about WalkMe's P/S ratio of 4.8x, since the median price-to-sales (or "P/S") ratio for the Software industry in the United States is also close to 4.3x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

How Has WalkMe Performed Recently?

With revenue growth that's inferior to most other companies of late, WalkMe has been relatively sluggish. One possibility is that the P/S ratio is moderate because investors think this lacklustre revenue performance will turn around. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on WalkMe.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, WalkMe would need to produce growth that's similar to the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 6.1%. The latest three year period has also seen an excellent 72% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 9.7% per annum as estimated by the eight analysts watching the company. With the industry predicted to deliver 15% growth per year, the company is positioned for a weaker revenue result.

With this information, we find it interesting that WalkMe is trading at a fairly similar P/S compared to the industry. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Bottom Line On WalkMe's P/S

WalkMe appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

When you consider that WalkMe's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. A positive change is needed in order to justify the current price-to-sales ratio.

You always need to take note of risks, for example - WalkMe has 3 warning signs we think you should be aware of.

If you're unsure about the strength of WalkMe's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.