Last week saw the newest first-quarter earnings release from Lululemon Athletica Inc. (NASDAQ:LULU), an important milestone in the company's journey to build a stronger business. Lululemon Athletica reported US$2.2b in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of US$2.54 beat expectations, being 5.1% higher than what the analysts expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Lululemon Athletica after the latest results.

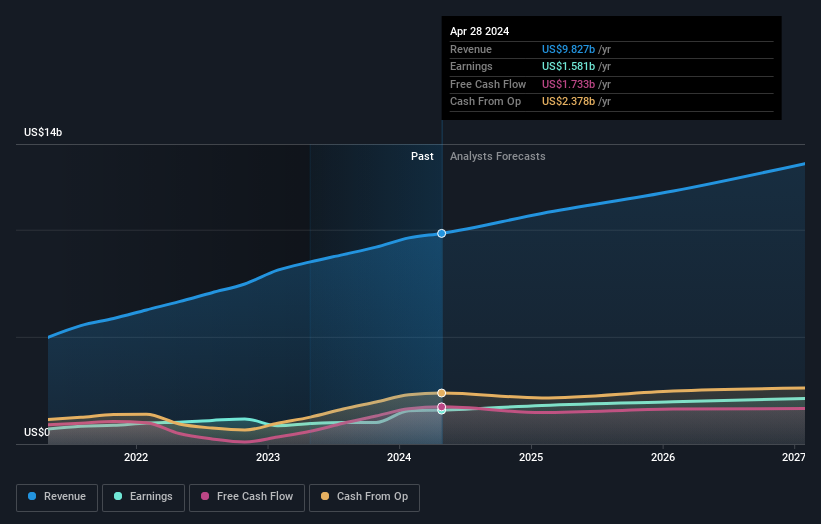

NasdaqGS:LULU Earnings and Revenue Growth June 8th 2024

Taking into account the latest results, the most recent consensus for Lululemon Athletica from 34 analysts is for revenues of US$10.8b in 2025. If met, it would imply a notable 9.5% increase on its revenue over the past 12 months. Per-share earnings are expected to grow 14% to US$14.39. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$10.8b and earnings per share (EPS) of US$14.19 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

With no major changes to earnings forecasts, the consensus price target fell 5.5% to US$405, suggesting that the analysts might have previously been hoping for an earnings upgrade. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Lululemon Athletica, with the most bullish analyst valuing it at US$525 and the most bearish at US$240 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Lululemon Athletica's past performance and to peers in the same industry. We would highlight that Lululemon Athletica's revenue growth is expected to slow, with the forecast 13% annualised growth rate until the end of 2025 being well below the historical 23% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.3% per year. So it's pretty clear that, while Lululemon Athletica's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Lululemon Athletica's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Lululemon Athletica. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Lululemon Athletica analysts - going out to 2027, and you can see them free on our platform here.

We also provide an overview of the Lululemon Athletica Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.