Source: Wall Street See News Author: Bu Shuqing.

Bank of America Merrill Lynch pointed out that with the huge demand for copper due to energy transition and AI investment trends, the copper supply-demand gap is expected to double by 2026. It gives buy ratings to multiple giants such as Zijin Mining Group and Jiangxi Copper, and believes that once copper prices go up, the profit growth of smaller and higher-cost companies like KGHM may be more significant. The product structure of 100-300 billion yuan products sees operating incomes of 401/1288/60 million yuan respectively.

After Goldman Sachs and Citigroup, Bank of America Merrill Lynch also expressed the strongest bullish voice for copper prices.

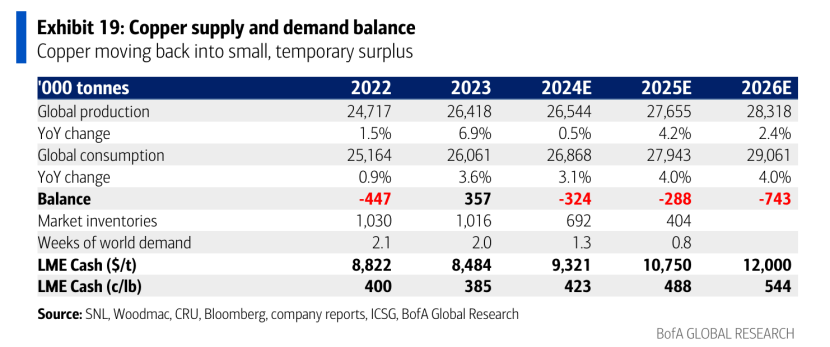

On Friday local time, analysts such as Jason Fairclough from Bank of America Merrill Lynch released a deep industry report, stating that copper prices are expected to rise to $12,000 per ton by 2026, more than 20% higher than current levels and closest to Citigroup's prediction. Goldman Sachs believes that copper prices are likely to reach this level ahead of schedule at the end of the year. The report pointed out that due to energy transition, the growth of Indian demand, and the rise of AI and data center construction trends, demand for copper is soaring. It is predicted that by 2026, the global supply-demand gap will double to reach 743,000 tons.

The report pointed out that due to energy transition, the growth of Indian demand, and the rise of AI and data center construction trends, demand for copper is soaring. It is predicted that by 2026, the global supply-demand gap will double to reach 743,000 tons.

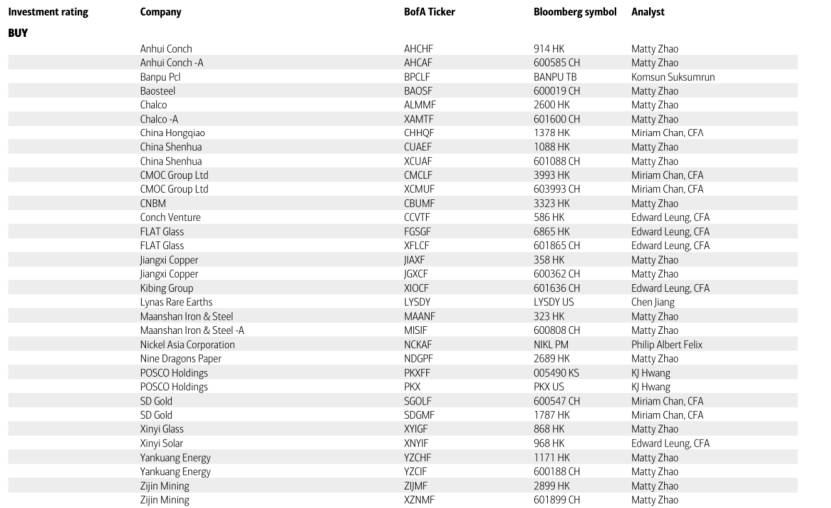

Bank of America Merrill Lynch is bullish on copper mining companies, giving Buy ratings to giants such as Freeport-McMoRan, Antofagasta Mining, Zijin Mining Group, Jiangxi Copper, Teck Resources and integrated miners such as BHP Group Ltd, Anglo American Plc and Glencore Plc which have hidden high-quality copper assets worth paying attention to.$Freeport-McMoRan (FCX.US)$Ivanhoe Mines$Zijin Mining Group (601899.SH)$, $Jiangxi Copper (600362.SH)$and other giants are given buy ratings.$Teck Resources (TECK.US)$, $ANGLO AMERI PLC (NGLOY.US)$, $GLENCORE PLC (GLNCY.US)$The high-quality copper assets of these integrated miners which are “hidden” are worth paying attention to.

The institution also believes that once copper prices go up, the profit growth of smaller and higher-cost companies like KGHM may be more significant.

The gap is expected to double by 2026.

The report topic, "Everybody wants copper," shows its optimism for copper demand.

Bank of America Merrill Lynch pointed out that$BHP Group Ltd (BHP.US)$recently launched a century acquisition bid against Anglo American Plc. This makes market fully aware of one thing: under the expectation of soaring copper prices, high-quality copper mining assets become increasingly scarce, and the value of controlling copper resources is increasing day by day.

The report pointed out that the global energy transformation is accelerating, and the core of this process is the "decarbonization". To achieve this goal, the demand for copper and other metals will significantly increase.

In addition, the rise of emerging economies such as India, and the rapid development of emerging industries such as AI and data centers will also provide strong support for copper prices.

Against the backdrop of tight copper supply, Bank of America Merrill Lynch predicts that there will be a shortfall of 324,000 tons of copper supply and demand in 2024. By 2026, this gap will reach 743,000 tons.

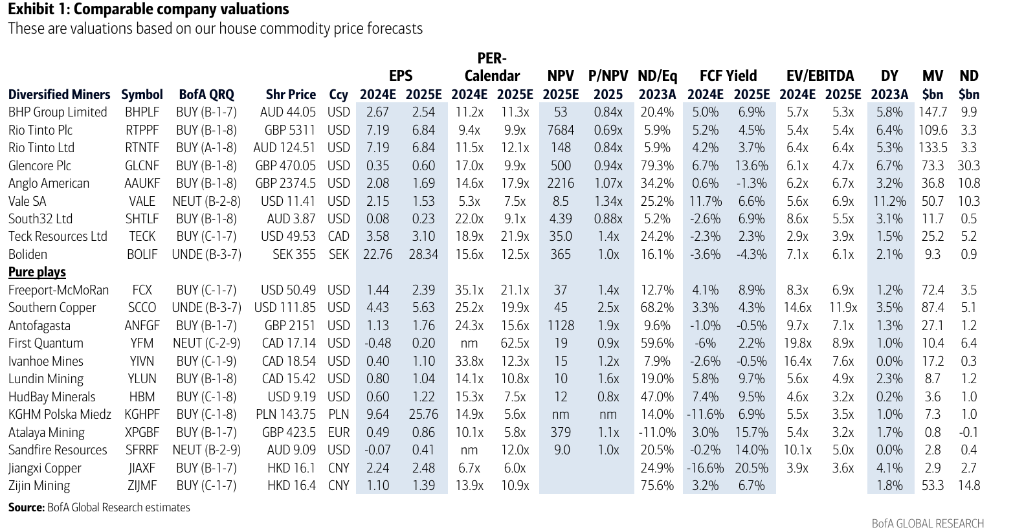

High-quality pure copper mining enterprises, pay attention to free ports and$Southern Copper (SCCO.US)$

Bank of America Merrill Lynch pointed out that the valuation of copper mining companies is affected by multiple factors, which should value fundamental factors such as cost and reserves, as well as market factors such as scale and liquidity. Those high-quality companies with outstanding performance in all aspects will receive a higher valuation premium and deserve investors' attention.

For the valuation analysis of major copper mining companies in the world, Bank of America Merrill Lynch introduced a new valuation indicator: the enterprise value (EV) corresponding to the annual production capacity of copper per ton, referred to as EV / ton.

Through calculation, Bank of America Merrill Lynch found that the value of each ton of copper production capacity on average is about $55,000.

However, the EV / ton of different companies varies greatly, mainly depending on the following factors:

Cost position-the lower the cost, the higher the EV / ton.

Mine life-the longer the mine life, the higher the EV / ton.

Location-the political and economic risks of different countries and regions are different, and the EV / ton will also vary.

Equity "packaging"-the EV / ton of listed companies are usually higher than that of non-listed companies.

Specific to the enterprise level, Bank of America Merrill Lynch pointed out that the EV / ton of the two large listed copper mining giants in the United States, Freeport-McMoRan and Southern Copper, exceeds $90,000, which is far higher than the industry average level.

Integrated mining giants: "hidden" high-quality copper assets should be seen

For large diversified mining companies, Bank of America Merrill Lynch continues to use the EV / ton indicator to deduce the implied value of high-quality copper businesses in these companies.

The analysis results show that the value of copper business under these integrated mining giants is considerable, but it is often overlooked by investors:

BHP Group Ltd, its copper business has an annual production equity ton of about 1.4 million tons, and the estimated value according to the EV / ton indicator may be between 79 billion and 96 billion US dollars.

As for Anglo American, although the scale of its copper business is not as good as BHP, its annual production equity ton is about 700,000 tons, but its valuation may also reach 41 to 50 billion US dollars.

As for Glencore, its annual production equity ton of copper business is about 860,000 tons, and the implied value may be between 49 billion US dollars and 59 billion US dollars.

These figures fully demonstrate that the copper business of comprehensive mining companies is not just a "sideline", but a real "value oasis". However, due to the many business of these companies, the value of the copper business is often underestimated by the market.

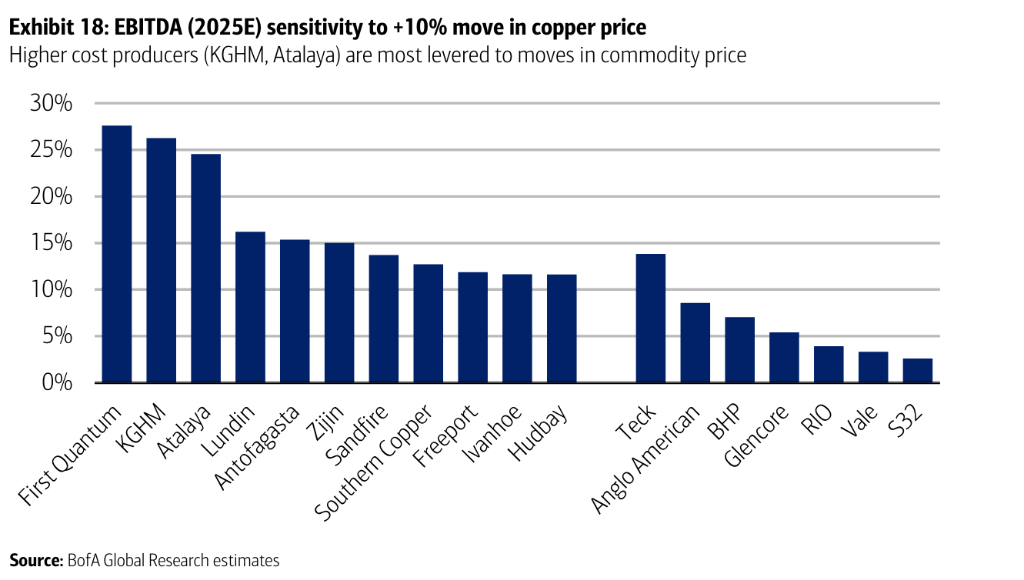

These copper enterprises have high profit elasticity.

Bank of America Merrill Lynch report specifically mentions a type of copper mining enterprise, namely "non-first-tier" copper mining enterprises that have high production costs.

Compared with industry leaders, they have higher costs, which means relatively lower profit margins. The mining asset has a shorter life cycle, and the future sustainable profitability is doubtful. They are smaller in scale and lack economies of scale. The asset-liability ratio is relatively high, and the financial risk is relatively greater.

From an investment perspective, these producer companies seem to have low "quality". For example, the EV/ton of companies like the Polish KGHM and the Spanish Atalaya Mining is less than 20,000 US dollars.

However, once copper prices rise, the profit growth potential may be greater. Bank of America Merrill Lynch points out that these stocks may have another attraction, which is a higher price leverage.

The so-called price leverage refers to the degree to which changes in copper prices affect corporate profits. Bank of America Merrill Lynch believes that for production companies with high costs, their profit growth may be more significant when copper prices rise.

Assuming that copper prices rise by 10%, KGHM's EBITDA in 2025 may increase by 26%; Atalaya Mining's EBITDA increase next year may also reach 25%.

Of course, this "high leverage" also means higher risks. Once copper prices fall, the stock prices of these companies may also fall more.

Editor/Lambor