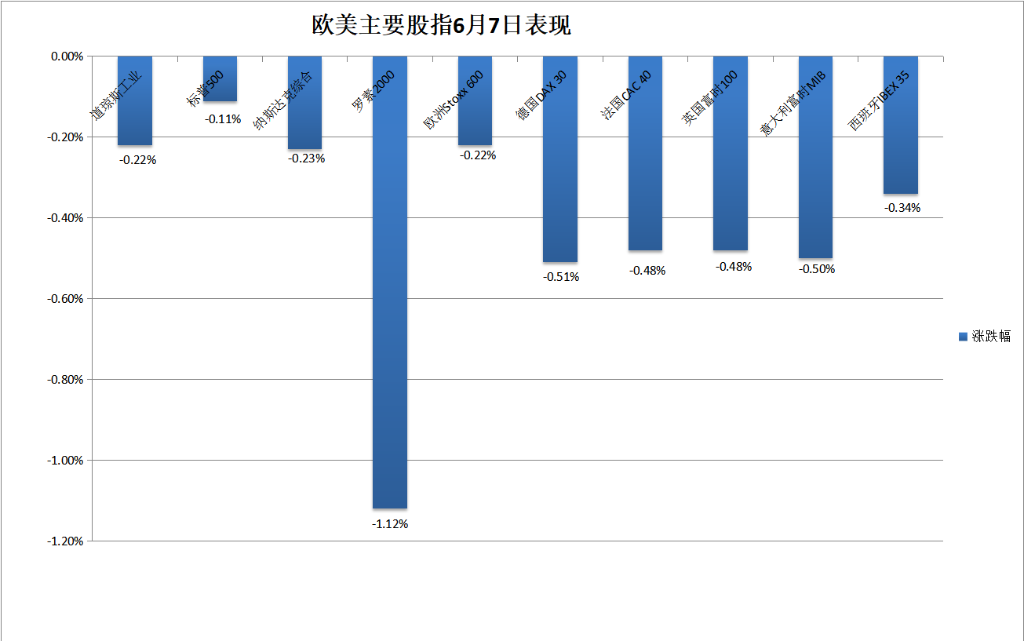

The three major US stock indices fell slightly, but all rebounded intraday and rose throughout the week. Nvidia rebounded unsuccessfully and fell for two consecutive days; Apple rose more than 1% before its heavyweight conference; Gamestop's losses widened after the live broadcast of the retail investor leader. The China concept stock index fell nearly 2% for two consecutive days. Daqo New Energy and Bilibili fell more than 5%.

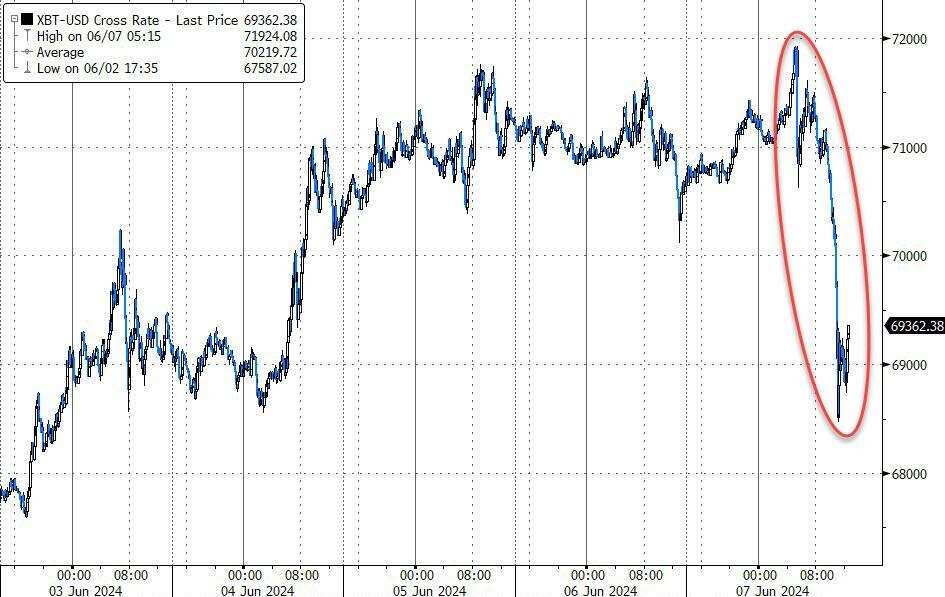

After the US employment report, US bond yields rose more than 10 basis points; the US dollar index, which had approached its two-month low, rose sharply and hit a new high in more than a week; offshore renminbi fell 180 points and lost 7.26. Bitcoin dropped more than $3,000, approaching the $72,000 mark in intraday trading.

Gold fell more than 3% in intraday trading, the largest drop in over two years. Silver fell more than 6%, while NYMEX copper fell more than 4% to a six-week low. LME zinc fell nearly 5%, the largest drop in over a year and a half. LME nickel fell 8.5% in a week. Crude oil slightly reversed and fell for three consecutive weeks, while US natural gas rebounded nearly 13% throughout the week.

Friday's release of the heavyweight US non-farm payroll report showed that both employment and wage growth were stronger than expected: 272,000 new jobs were added to the US non-farm payroll in May, exceeding consensus expectations by 92,000, and average hourly wages increased by 4.1% year-on-year, failing to stabilize at April's expected rate of 3.9%. The month-on-month growth rate also exceeded expectations, rising by 0.4%. However, the unemployment rate unexpectedly failed to stabilize in April and rose for the first time in over two years to 4.0%.

Commentary indicates that this is a report unfriendly to monetary easing. The strength of the labor market reflected in the report may keep upward pressure on inflation stubborn and strengthen the Federal Reserve's cautious attitude towards interest rate cuts, so the fed may maintain high interest rates unchanged in the coming months. Mohamed El-Erian, former Pimco CEO, commented that the report closed the door to the July rate cut.

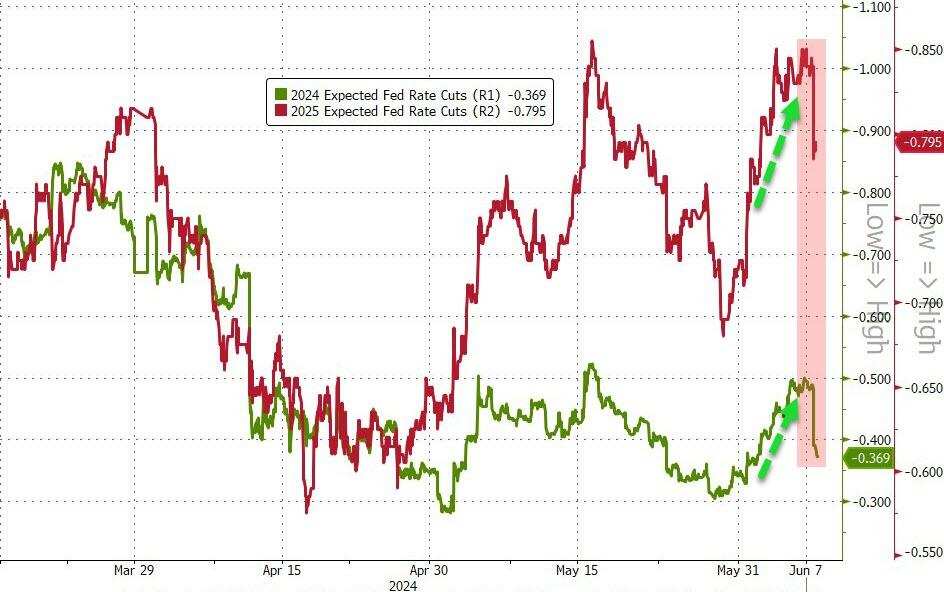

The non-farm payroll report dealt a heavy blow to expectations of rate cuts later this year that had risen earlier this week. Prior to the report's release, derivative contract pricing fully anticipated rate cuts in November. After the report was released, traders' estimate of the probability of a rate cut in November dropped to about 80%, and their estimate of the total rate cuts for the year fell from 47 basis points before the report to about 37 basis points.

After the employment report was released, US Treasury prices plummeted, with the benchmark 10-year US Treasury yield and the two-year US Treasury yield, which is more sensitive to the prospect of interest rates, rising more than 10 basis points intraday; the US dollar index, which had approached its lows over the past two months earlier today, soared in a straight line, rising to a high of more than a week later; US stocks opened lower; precious metals such as gold, silver, and copper all accelerated their decline, with NYMEX gold and spot gold both falling more than 3%, the largest drop in more than two years, while silver futures fell more than 6% and copper futures fell more than 4%.

However, the decline in US stocks eased during trading. Seven technology giants, including Nvidia, which fell by more than 2% at the beginning of trading, all rebounded intraday. The only rising stock, Apple, rose by more than 1% after being exposed to AI features in iOS 18 before the global developer conference WWDC next Monday. Nvidia rose by double digits throughout the week, helping to rebound all major indexes of the US stock market, which fell back last week. However, Gamestop, which unveiled a possible sale of up to 75 million shares, plummeted more than 40% during trading, wiping out most of the gains after the news that Keith Gill, a retail investor leader, resumed his YouTube live show after a three-year hiatus, and its losses remained unimproved even after Gill went live.

Compared with metals, the international crude oil market has had a more limited decline in commodity prices and has rebounded several times during the session. Expectations for Federal Reserve interest rate cuts were impacted by oil demand prospects. Baker Hughes data for this week showed that the number of active oil and gas rigs in the US fell to a near-two-and-a-half-year low. In addition, Saudi Arabia's Energy Minister hinted on Thursday that the production agreement reached by OPEC+ last weekend may be adjusted or even scrapped. This partially offset downward pressure on oil prices. Crude oil continued to decline throughout the week, mainly due to the OPEC+ agreement showing that eight countries, including Saudi Arabia, will gradually lift their voluntary production cuts from October. On the first trading day after the agreement was announced, oil prices plummeted this Monday. Precious metals such as gold also fell throughout the week. In addition to concerns about the prospect of rate cuts triggered by the employment report, some commentators noted that China's gold reserves stopped rising for the first time in 18 months, which was also negative news for gold on Friday.

All three major US stock indices rebounded intraday. Nvidia rebounded unsuccessfully for two consecutive days, while Gamestop, after the live broadcast of the retail investor leader, continued to widen its losses.

All three major US stock indices opened lower and rebounded intraday. The Dow Jones Industrial Average initially fell more than 130 points or more than 0.3%, but rebounded and maintained its upward trend. The index rose nearly 220 points or nearly 0.6% intraday, refreshing its daily high before noon. The S&P 500 initially fell 0.4%, but overturned the decline less than an hour after the opening. The NASDAQ Composite Index initially fell nearly 0.5%, but rebounded more than an hour after the opening, and refreshed its daily high at noon, rising separately from the S&P.

All three major indices fell during the afternoon session, ultimately closing lower. The S&P fell 0.11% to 5,346.99 points, and the Nasdaq fell 0.23% to 17,133.13 points, both continuing to fall from the record closing high set on Wednesday. The Dow, which had risen for three consecutive days and hit a new closing high since May 24, closed down 87.18 points, or 0.22%, at 38,798.99 points.

The small-cap stock index Russell 2000, which focuses on value stocks, fell by 1.12% and has fallen for two consecutive days, underperforming the broader market, and hit a new closing low since May 2, which was set on Tuesday. The Nasdaq 100 index, which is dominated by technology stocks, fell 0.11%. The related ETF Invesco QQQ Trust Series 1 (QQQ) fell 0.09%. The Nasdaq Technology Market Cap Weighted Index (NDXTMC) measuring the performance of technology stocks in the Nasdaq 100 index fell 0.03%. Both indices fell for two consecutive days after hitting a new record closing high for three consecutive days, with the latter rose 3.78% for the week.

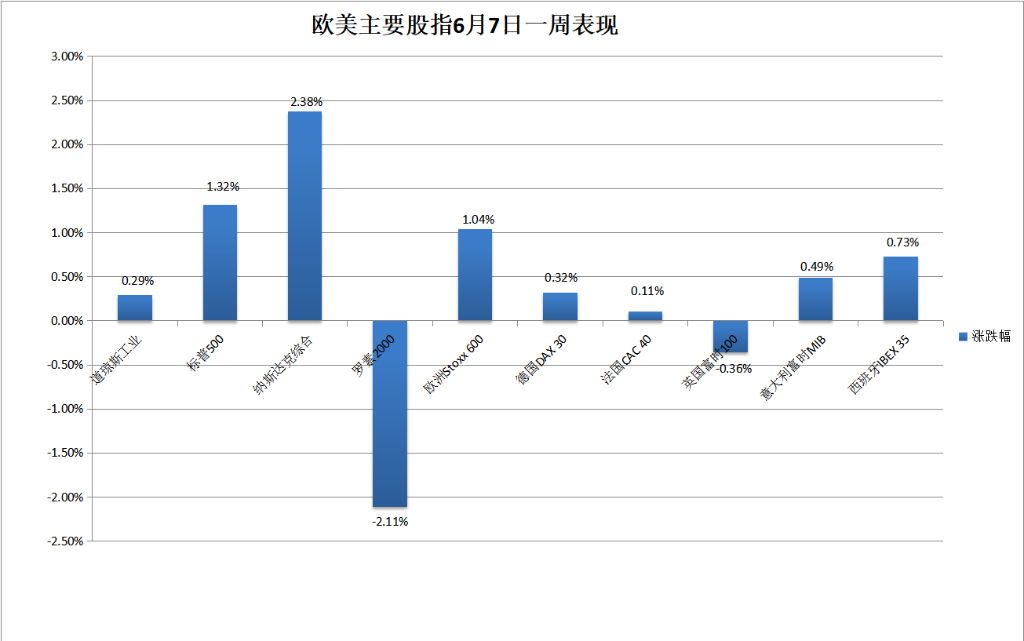

This week, major US stock indices rebounded collectively. The S&P rose 1.32%, the Nasdaq rose 2.38%, and the Nasdaq 100 rose 2.5%, all experiencing their sixth week of gains within the past 7 weeks. The Dow, which had fallen for two consecutive weeks, rose 0.29% for the week. However, the Russell 2000, which had a slight increase last week, fell and dropped 2.11% for the week.

Among the Dow components, UnitedHealth, the healthcare giant, fell more than 2% on Friday, leading the decliners. Walmart fell nearly 2%, and Home Depot and McDonald's fell more than 1%. 3M rose over 2%, while Travelers, Apple, JPMorgan, IBM, and Intel all rose more than 1%. Only four of the major sectors in the S&P 500 rose on Friday. The financial sector rose nearly 0.4%, the IT sector, which includes Apple, rose 0.2%, while the healthcare and industrial sectors rose 0.1%. Among the seven sectors that declined, the real estate and utility sectors affected by high interest rates fell by nearly 0.9% and 1.1%, respectively. And the materials sector, which suffered a large drop in metals, fell by about 1%.

This week, six sectors of the major US stock indices rose, with the IT sector rising more than 3.8%, healthcare rising nearly 2%, and communications services rising more than 1.7%, followed by non-essential consumer goods rising 1.5% and essential consumer goods rising nearly 0.5%. The four sectors that fell were utilities, which fell nearly 4%, energy, which fell nearly 3.5%, materials, which fell 2%, and industry, which fell nearly 1%. Finance fell nearly 0.5% and real estate fell more than 0.2%.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Meta, and Tesla, the seven technology giants, all had turned higher at some point in intraday trading but most fell by the end of the day. Tesla, which had risen for two consecutive days, fell 1.1% at the start of trading, then rose nearly 0.8% in the morning but fell 1.3% at noon and closed down nearly 0.3% for the week, declining slightly for two consecutive weeks.

Among the top six FAANMG technology stocks, Microsoft hit a new high for three consecutive days since May 29, then rose 0.4% after a intraday rise, but still fell nearly 0.3% at the close. Alphabet hit a new high for five consecutive days since May 21, but fell repeatedly during intraday trading and fell nearly 1.4% at the close. Amazon hit a new high for three consecutive days since May 15, then fell nearly 0.9% at the start of trading, but rose as much as 0.7% in the intraday session before falling nearly 0.4% at the close. Meta rose after an intraday rise, then rose 1% at noon but fell nearly 0.2% at the close, dropping for two consecutive days after rebounding on Wednesday to a high since April 23. Netflix initially fell and fell nearly 1.1% at the close, continuing to fall from the high of nearly 3% rebound on Wednesday. Apple initially fell sharply, but closed up more than 1.2%, hitting the highest closing price since December 19, 2023, after ending an eight-day rally on Thursday.

Most of the six major FAANMG technology stocks rose this week. Meta rose nearly 5.5%, Amazon rose more than 4%, Apple and Microsoft rose more than 2%, Alphabet rose more than 1%, while Netflix fell by less than 0.1%.

Semiconductor stocks fluctuated in the session, with the Philadelphia Semiconductor Index and Semiconductor Industry ETF SOXX falling nearly 0.7% at the beginning of the day, with early and mid-day gains reversing several times and closing down about 0.3%, following a two-day decline after rebounding to a closing high on Wednesday, with increases of 3.2% and nearly 2.6% respectively this week. Among semiconductor stocks, Nvidia fell nearly 2.5% at the opening, rose slightly at noon, and finally closed down less than 0.1%, continuing to fall from the record closing high set on the third consecutive day on Wednesday, and still up 10.3% this week; at the close, Semtech (SMTC), which announced the departure of its CEO, fell 17.9%, while Intel and Taiwan Semiconductor rose more than 1%, and AMD and Micron Technology rose nearly 0.7%, while Broadcom rose nearly 0.4%.

Most AI concept stocks fell. The AI and robotics ETF Glb X Robotics & Afl Intelligence ETF (BOTZ). At the close, SoundHound.ai (SOUN) fell nearly 4%, Dell (DELL) fell 3%, Palantir (PLTR) fell 2%, Super Micro Computer (SMCI) and Astera Labs (ALAB) fell more than 1%, while BigBear.ai (BBAI) rose 5.9%, Oracle (ORCL) rose nearly 2%, and C3.ai (AI) rose 0.2%.

Overall, popular China concept stocks fell, underperforming the broader market. The Nasdaq Golden Dragon China Index (HXC) opened lower and traded lower in the morning, down nearly 2% at noon and closing down more than 1.7%, falling for two consecutive days, hitting a closing low since May 1 created on Monday this week, with a cumulative decline of more than 1.6% this week. KWEB and CQQQ, two China concept ETFs, both closed down about 2.9%. Among the new car manufacturers, XPENG Auto fell more than 2.5% at the close, while NIO Inc and ECARX fell more than 1%, and Li Auto Inc rose more than 1%. Among other individual stocks, Daqo New Energy and Bilibili fell more than 5%, JinkoSolar fell more than 4%, Tencent Music fell more than 3%, Alibaba fell 2%, Baidu fell nearly 2%, JD.com fell more than 1%, while PDD Holdings rose slightly and NetEase closed flat.

Among the stocks with significant fluctuations, GameStop (GME), which rose 47.5% on Thursday, opened down 19%, rose 3.1% briefly in the short term, fell more than 30% in the morning after turning downward, and fell nearly 44% after Keith Gill's live broadcast at noon; Vail Resorts (MTN), a ski resort operator whose third-quarter profits and revenues fell below expectations, closed down 10.3%; and despite better-than-expected first-quarter results, electronic signature company DocuSign (DOCU) still closed down 4.7%, while biopharmaceutical company Planet Labs (PL), with lower-than-expected first-quarter losses and higher-than-expected revenue, rose about 11% after being approved by the US regulatory agency FDA for its blood disease treatment drug Rytelo earlier than analysts expected; and biopharmaceutical company Geron (GERN), which benefited from the approval, rose about 18%.

Following the US employment report, the broad European stock index remained on a downward trend for a second consecutive day. The Stoxx Europe 600 index fell from its closing high on May 15 on Thursday. The benchmark stock indices of the four major eurozone economies and the UK fell overall on Friday after a joint rise for two days.

In various sectors of the Stoxx 600, real estate, which is sensitive to interest rates, led the decline, falling nearly 3% among constituents, with Vonovia, a German-listed real estate company downgraded by Morgan Stanley, plunging 7.2%; while the healthcare sector rose nearly 0.5%, with Novo Nordisk, the highest market capitalization drug company in Europe, up 1.1%, setting new historical highs along with its own and the Danish stock indices; and the technology sector rose nearly 0.4%, with ASML, the highest market capitalization technology stock in Europe listed in the Netherlands, up nearly 0.2%, setting new historical highs for three consecutive days along with the Dutch stock indices.

The Stoxx 600 index rose about 1% this week, rebounding after two consecutive weeks of decline. Most national stock indices rose, with German and French stocks, which fell nearly 3% for three consecutive weeks, and Italian stocks, which rose strongly last week, being stable this week, while the Spanish stock index rose for two consecutive weeks and the British stock index fell for four consecutive weeks.

In various sectors, technology, which led the decline by nearly 3.5% last week, rebounded strongly this week, with an overall gain of over 6%, and ASML rose sharply by 10.1% throughout the week, while the healthcare sector rose more than 3% this week, with Novo Nordisk up 6.1% overall; while the resource sector, which was dragged down by a cumulative decline of commodities such as crude oil, had the biggest decline among sectors, with basic resources stocks in the oil and gas and mining sectors down 3.1% and 2.9% respectively, and the real estate sector fell 1.8% overall this week due to a big drop on Friday.

Following the employment report, US bond yields rose more than 10 basis points, but the ten-year yield still fell throughout the week.

Before the nonfarm payroll report was released, the yield of the 10-year benchmark Treasury bond in the United States hit a daily low. After the report was released, it quickly climbed above 4.40%. At the beginning of the regular trading hours, it rose above 4.43%, increasing nearly 15 basis points intraday, far away the low level since April 1 that it had continuously refreshed for two days away from dropping below 4.28% on Thursday. After the opening of US stocks, the increase slightly narrowed, still above 4.40%, and reached about 4.43% at the end of the bond market. After falling for five consecutive days, it rose for two consecutive days. It has accumulated a decrease of about 7 basis points this week, and fell back after rising for two weeks.

The yield of the 2-year US Treasury bond, which is more sensitive to interest rate prospects, hit a daily low in early Asian trading after the employment report was released. It quickly rose above 4.80% after the report, and the US stock market's gains expanded at noon. It rose above 4.88% at the end of the bond market, far away from the low level since April 5th that it had continuously refreshed for four days away from dropping below 4.72% the next day after the US CPI release. It was about 4.89% at the end of the bond market and rose by about 17 basis points intraday after roughly stable on Thursday. It rose for the first time in the recent eight trading days due to Friday's rally, and the yield accumulated an increase of about 2 basis points this week after falling back last week.

After the employment report, the US dollar index rose sharply to a new high of more than a week, and Bitcoin once approached the 72,000 mark in intraday trading and fell more than 3,000 US dollars afterwards.

The ICE US Dollar Index (DXY), which tracks the exchange rates of six major currencies against the US dollar, has fluctuated slightly downward several times on Friday morning during the European market session, and fell below 104.00 at the beginning of the European market, extremely approaching the low since April 9th hit on Tuesday, and it rose rapidly after the US non-farm payroll report and the US stock market's early gains rose above 104.90 before noon, approached 104.95 at noon, hitting a high since May 30th, and rose more than 0.8% intraday.

By the end of Friday's foreign exchange market, the US dollar index was reported above 104.90, rising 0.8% intraday after falling back on Thursday, accumulating an increase of about 0.2% after falling back last week. The Bloomberg US Dollar Spot Index, which tracks the exchange rates of ten other currencies against the US dollar, rose 0.8% intraday, rose for two consecutive days, and was located at a high level since May 1st at the same time this week, with an increase of nearly 0.9% this week and two consecutive weeks of rise.

After the US employment report, the euro against the US dollar and the British pound against the US dollar both fell sharply among non-US currencies. The euro dropped below 1.0800 at noon, hitting a low since May 30th, and fell by 0.8% intraday. The British pound fell nearly 0.6% after US stocks fell below 1.2720 in the morning, hitting a low since Monday of this week and tumbling since the employment report. The yen rebounded on Thursday and fell during the trading session; it rose more than 0.9% intraday after the USD/JPY turned upward after the employment report. US stocks rose above 157.00 in the morning, returning to the intra-day level on Monday, escaping from the low of 154.60-154.55 hit since May 16th, and intraday rose more than 0.9%.

Offshore yuan (CNH) against the US dollar hit a daily high of 7.2474 before the US employment report was released, and plunged after the report was released. The US stock market hit a daily low of 7.2654 in the morning, dropping by 180 points from the daily high, and failed to approach the intraday high since May 21st set on the day when it rose above 7.24. At 4:59 Beijing time on June 8, the offshore yuan against the US dollar reported 7.2631 yuan, down 38 points from the New York closing last Thursday, and cumulatively fell slightly this week, unable to reverse the downward trend of last week.

Bitcoin (BTC) once rose above 71,900 US dollars in the European stock market, hitting a high since May 20, and fluctuated downwards after the US nonfarm payroll report was released. The US stock market accelerated its decline in midday trading and fell below 70,000 US dollars. It fell by nearly 5% and fell by nearly 3000 US dollars and nearly 5% compared to the daily high. It was slightly higher than 69,000 US dollars at the close of US stocks, falling nearly 2% in the past 24 hours and rising more than 2% in the past seven days. Ethereum (ETH), the second largest cryptocurrency with a market capitalization only second to Bitcoin, fell below $3620 and part of the platform tested $3600, hitting a low since May 21st, and fell by about 6% from the intraday high in the European stock market. US stock market closed at less than 3680 US dollars, falling nearly 3% in the past 24 hours and falling more than 2% in the past seven days.

London zinc fell nearly 5%, New York copper fell more than 4%, gold hit the biggest drop in more than two years, and silver fell more than 6%.

The basic metal futures in London all fell by nearly 2% at least after rebounding on Thursday, with zinc falling by more than 4.9%, hitting the biggest drop since October 2022, and hit a new low since early April, while tin and nickel both fell for the sixth time in recent seven trading days. Copper fell by 3.8%, just recovering the 10,000 US dollar mark on Thursday, just fell to less than 9800 US dollars at the closing after falling to a low since late April. Nickel fell 2.7% to a low since mid-April. Aluminum fell to a low since mid-May. Zinc fell back most of its gains from nearly 3% on Thursday, approaching the low since early May set on Wednesday.

Due to the decline on Friday, the basic metals collectively fell this week. London nickel fell by about 8.5%, while London zinc fell by more than 6.8%, and London tin fell by 4.8%, all falling for three consecutive weeks. London copper and London aluminum fell by nearly 2.8%, falling for three and two weeks respectively, and London lead fell by more than 3%, falling for two consecutive weeks.

After rising for two consecutive days, New York copper futures fell sharply, breaking below $4.4470 during the day and falling by nearly 5% during the day, with COMEX July copper futures eventually falling by nearly 4.2% to $4.4835 per pound, hitting a low since April 24 and falling for three consecutive weeks this week.

After the US employment report, gold accelerated its decline, with spot gold falling below $2,290 at the end of the US stock market, hitting a monthly low, and falling more than 3.7% during the day, the largest intraday drop since March 2022. New York gold futures fell below $2,304 after the US stock market closed, down about 3.6% during the day.

At the close of the US stock market, COMEX August gold futures, which had risen for two consecutive days and reached a two-week high since May 22, fell by nearly 2.8%, hitting the largest closing drop in the main contract since April 22, 2022, at $2325 per ounce, hitting a closing low since May 8. It fell nearly 0.9% this week and fell back after rebounding last week.

After the US stock market closed, New York silver futures hit a daily low of $29.22, falling by more than 6.8% during the day. When the US stock market closed at noon, COMEX July silver futures fell by more than 6.1%, hitting a closing low since May 14, down nearly 3.9% this week and falling for three consecutive weeks.

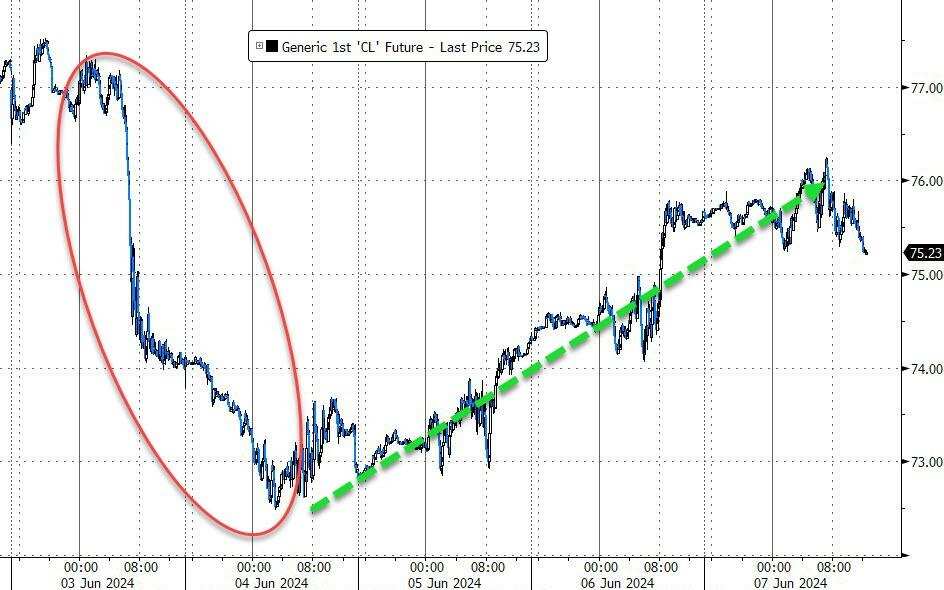

Crude oil fell slightly for three consecutive weeks. US natural gas rebounded nearly 13% throughout the week.

International crude oil futures fluctuated downward several times during Friday's session. At the beginning of the European session, US WTI crude oil approached $75.20, down nearly 0.5% during the day, while Brent crude oil approached $79.30, down nearly 0.7% during the day. When the US stock market surged, US oil rose above $76.20, up more than 0.9% during the day, and Brent oil approached $80.40, up more than 0.6% during the day. It then fell several times. In the end, crude oil, which rebounded for two consecutive days, closed slightly down, failing to continue to break away from the closing low since early February, which was refreshed after five consecutive declines on Tuesday. WTI July crude oil futures fell by 0.02 US dollars, a drop of more than 0.02%, to 75.53 US dollars per barrel; Brent August crude oil futures fell by 0.25 US dollars, a drop of more than 0.31%, to 79.62 US dollars per barrel.

In the end, crude oil, which rebounded for two consecutive days, closed slightly down, failing to continue to break away from the closing low since early February, which was refreshed after five consecutive declines on Tuesday. WTI July crude oil futures fell by 0.02 US dollars, a drop of more than 0.02%, to 75.53 US dollars per barrel; Brent August crude oil futures fell by 0.25 US dollars, a drop of more than 0.31%, to 79.62 US dollars per barrel.

This week, US oil fell by about 1.9%, and Brent oil fell by more than 1.8%, both falling for three consecutive weeks. Brent oil has fallen for the fifth week out of the past six weeks. Since the outbreak of the Israeli-Palestinian conflict, US oil has accumulated a decline for 20 weeks, and Brent oil has accumulated a decline for 17 weeks. The main reason for the accumulative decline in crude oil this week was the sharp drop on Monday, when it fell more than 3%, hitting the largest daily drop since Saudi Arabia unexpectedly lowered its official crude oil selling price to Asia on January 8.

US gasoline and natural gas futures rose and fell unevenly. NYMEX July gasoline futures, which rebounded for three consecutive days after falling to the lowest point since more than two months on Monday, fell by more than 0.6%, to $2.3826 per gallon, down about 1.4% this week and falling for three consecutive weeks; NYMEX July natural gas futures rose by 3.44%, to $2.9180 per million BTUs, rising for three days, hitting a high since May 23, and rose by about 12.8% this week after falling for two consecutive weeks.

Editor/Emily