Source: Zhang Yidong Strategic World

1. The share of short sales transactions has declined significantly. The first phase of the Hong Kong stock market is over, and we will wait for “refueling in the air”

1.1. Short recovery and expected recovery drive the first phase of the Hong Kong stock market

The March 21 report “The Spring of Hong Kong Stocks: Investing with a High Win Rate is the Way to Win” emphasizes that Hong Kong stocks are expected to rise at the bottom in 2024 and gradually return to the long market from the short market in the past few years. On May 14, “The Core Assets of Hong Kong Stocks in the New Era” pointed out that the market since April was the first stage in the Hong Kong stock market. Foreign capital “switched highs and lows” back into Hong Kong stocks, and short-term domestic and foreign investment resonance drove Hong Kong stocks to strengthen.

1.2. After the sharp rise, Hong Kong stocks entered a period of instability, waiting for “refueling in the air” in June and July

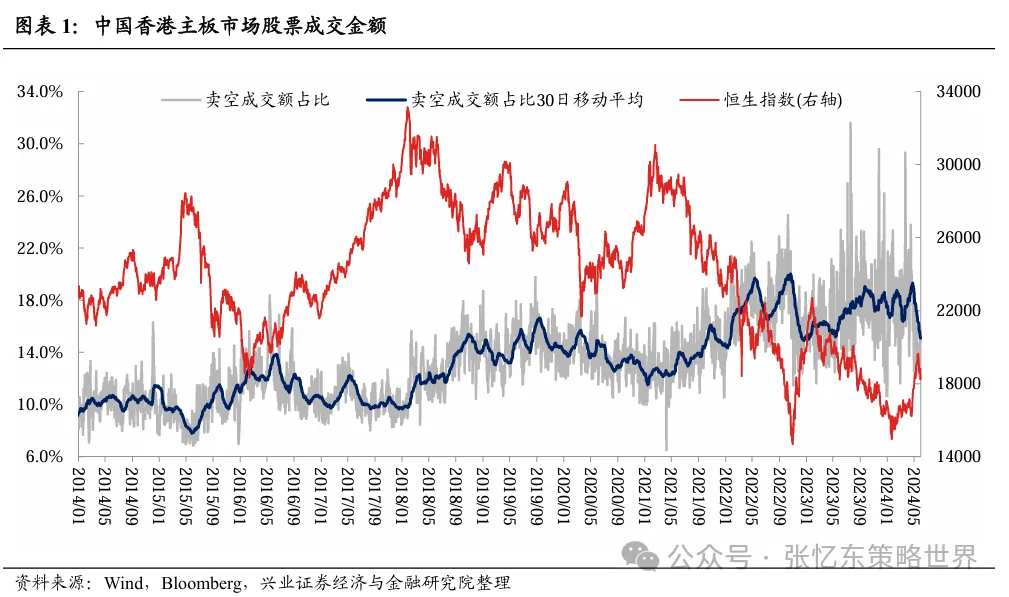

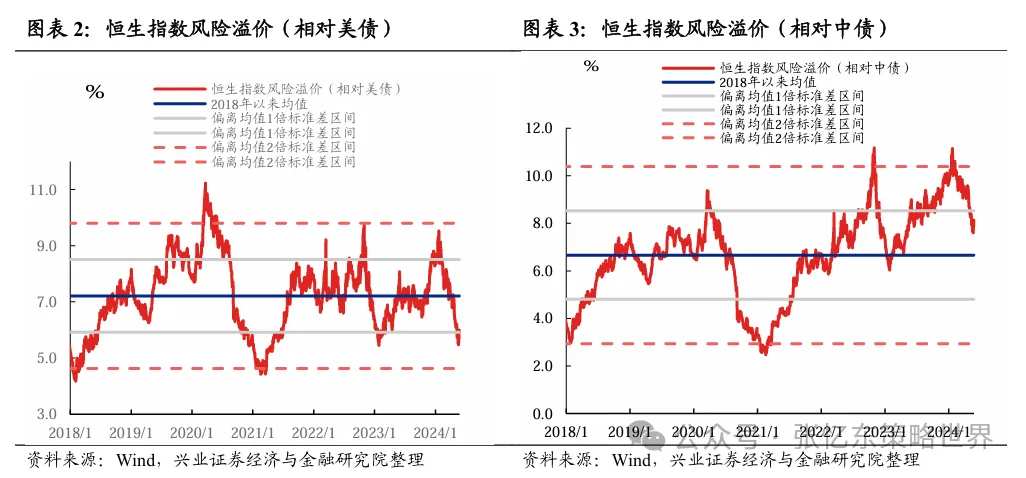

First, after a sharp rise, profit trading back is normal as the share of short sales transactions and risk premiums fall. The share of short sales in Hong Kong stocks has declined significantly recently. The correction of “poor expectations” has come to an end, and the market will enter a period of turbulence.

1) The share of short sales fell to 15.8% on May 30, which is below the center since 2018.

2) The risk premium relative to US bonds has fallen back to 6%, near the low point of the risk premium during the round of rebound from the fourth quarter of 2022 to the beginning of 2023. The further decline in risk premiums depends on stronger fundamentals being driven.

3) The AH premium fell back to its low level since 2020, and the price-performance ratio of A-shares improved. Hang Seng's Shanghai-Shenzhen-Hong Kong Stock Exchange AH share premium fell from over 55% in February 2024 to 36% on May 24, 2024, the lowest level since 2020. However, it is still in the 61.4% quartile since 2014.

Second, overseas investors must wait for data verification of improvements in fundamentals after the policy is implemented.

Third, considering the resilience of the US economy and the stickiness of high inflation, long-term interest rates on US bonds remained high above 4% in June and July. The traditional foreign-funded holiday season in June and July may trigger an increase in risk aversion due to “falling into the bag of profits.”

2. The current round of the Hong Kong stock market is more sustainable than the rebound from the end of 2022 to the beginning of 2023. Changes in fundamentals and capital will drive the second phase of the market

2.1. First, compared with the rebound from the end of 2022 to the beginning of 2023, the fundamental trend may not be the same

The end of the rebound from the end of 2022 to the beginning of 2023 was accompanied by the PMI falling again and returning to within the 50 range after two months of rapid backdrawing. In 2023, the Hang Seng Index unanimously expects EPS to continue to decline at the beginning of the annual reporting season. At the end of 2023, EPS is expected to drop 8.4% from the high at the beginning of the year.

The core characteristic of the second phase of the current Hong Kong stock market is that it is driven by fundamentals. In particular, improvements in core asset fundamentals may exceed the expectations of overseas investors, triggering a double attack on Davis.

First, the advantages of China's economic decision-making mechanism will begin to be re-recognized and praised. Strength in strategic transformation and tactical flexibility at the bottom line of risk prevention will help the Chinese economy to successfully get out of the painful period of switching between old and new momentum.

Second, at the mesoscopic level, enterprises have entered a stage where overall inventory removal has ended and the peak growth rate of production capacity expansion has passed, which is conducive to price recovery and a steady recovery in nominal GDP growth. The improvement in the profit growth rate of leading listed companies is even more obvious.

Third, during the mid-reporting season for Hong Kong stock listed companies in August, the performance guidelines of Hong Kong stock leaders were more optimistic, thus attracting more domestic and foreign investors to increase their holdings of Hong Kong stocks.

2.2. Second, compared with the rebound from the end of 2022 to the beginning of 2023, the funding trend may not be the same

In 2023, the Federal Reserve is still in an austerity cycle. Interest rates on US bonds are rising, and local interest rates in Hong Kong remain high, which has had a great impact on the liquidity of the Hong Kong stock market.

In 2024, the top interest rate on US bonds confirmed, and US inflation and economic data are expected to decline in the third quarter. The Federal Reserve is expected to usher in “forward-looking and preventative interest rate cuts” in September. Even if interest rates are not cut in September, weakening data will help raise expectations of interest rate cuts, thus driving the decline in interest rates on US 10-year treasury bonds. The Hong Kong Interbank Discount (HIBOR) generally follows the trend of interest rates on US bonds. Therefore, when interest rates on US bonds decline, it is also conducive to a decline in capital interest rates in Hong Kong, making the capital side of Hong Kong stocks easier. The inversion of interest spreads between China and the US is also expected to improve, which will not only help stabilize the RMB exchange rate, but also help increase the attractiveness of allocating RMB assets.

3. Investment Strategy: Safely hold high-dividend assets in Hong Kong stocks during periods of shock and place core assets on dips

3.1. Allocation of high-dividend assets in Hong Kong stocks: dividend ratios are still attractive, benefiting from the potential possibility of optimizing tax arrangements for connected dividends

The high-dividend assets of Hong Kong stocks are still very attractive to allocation-based capital in mainland China. We will continue to focus on high-yield stocks in the energy, telecommunications and other industries where the AH dividend ratio gap is still large. As of May 29, 2024, the dividend rate of the Hang Seng Hong Kong Stock Connect High Dividend Low Volatility Index was 6.63%. The spread with the 10-year Chinese Treasury Bond yield reached 4.35 percentage points, and is still at a historically high quantile level.

Compared with the high-dividend “pure debt” allocation strategy of central state-owned enterprises that we have continued to recommend since the beginning of 2022, 2024 can be optimized into a “convertible bond” allocation strategy to allocate high-dividend assets with improved fundamentals or that can exceed expectations.

1) Benefit from factors such as price increases and positive free cash flow, and profits have upward elasticity, which can increase dividends, such as utilities.

2) “Poor expectations” repair high-dividend assets of Hong Kong stocks with high momentum, such as the real estate industry chain. If real estate inventory removal progresses smoothly, then real estate, properties, non-ferrous metals, construction, and building materials related to the real estate industry chain are likely to exceed expectations.

3.2. Core assets of Hong Kong stocks in a new era with a more flexible layout on dips

The core assets of Hong Kong stocks in the new era refer to having good cash flow to support the sustainability of dividends and performance (dividend rate+repurchase yield above 3%), and supporting the sustainability of dividends and performance with good cash flow. It is also a sign that equity culture is maturing; in the future, it can have a significant performance growth rate (performance growth rate of not less than 10%, high standards above 15%).

After more than 4 years of in-depth adjustments, the restructuring of the valuation system of the most competitive leaders in the Hong Kong stock industry has been completed. Even in terms of pessimistic performance expectations, the valuation is not high.

As the economy stabilizes and improves in the second half of the year, good companies are expected to usher in a moment where “fundamental data is not as bad as previously expected” to “fundamentals continue to improve.”

The core assets of Hong Kong stocks in the new era focus on TMT leaders such as the Internet, beneficiaries of new trends in domestic demand, winners in the overseas industry chain, and “leftovers are king” opportunities in fields with good upstream supply and demand relationships.

Risk warning: the risk of a game between major powers; the risk that the US monetary policy exceeds expectations; the risk that the decline in economic growth exceeds expectations.

Report text

1. The share of short sales transactions has declined significantly. The first phase of the Hong Kong stock market is over, and we will wait for “refueling in the air”

1.1. Short recovery and expected recovery drive the first phase of the Hong Kong stock market

The March 21 report “The Spring of Hong Kong Stocks: Investing with a High Win Rate is the Way to Win” emphasizes that Hong Kong stocks are expected to rise at the bottom in 2024 and gradually return to the long market from the short market in the past few years. On May 14, “The Core Assets of Hong Kong Stocks in the New Era” pointed out that the market since April was the first stage in the Hong Kong stock market. Foreign capital “switched highs and lows” back into Hong Kong stocks, and short-term domestic and foreign investment resonance drove Hong Kong stocks to strengthen. The reason is:

1) Hong Kong stocks have continued to be adjusted for many years, and the timing and extent of the adjustments are rare in history. The Hang Seng Index's risk premium compared to the US 10-year Treasury yield was over 9% at the beginning of 2024, which is significantly higher than the overseas equity market.

2) China's economic policy tone is more positive, and economic expectations are picking up. As the economy stabilizes, good companies are expected to usher in a moment where “fundamental data is not as bad as previously expected” to “fundamentals continue to improve.”

3) The 2024 airport stock transaction was reversed. Since April, US bond yields have fluctuated at a high level, suppressing highly-valued assets such as the US and Japan but not raising concerns about systemic risks. Overseas institutional investors are willing to find more cost-effective opportunities, return to the “depression” of Hong Kong stocks, push Hong Kong stocks to make up for bears, and thus attract domestic investors to increase their positions.

1.2. After the sharp rise, Hong Kong stocks entered a period of instability, waiting for “refueling in the air” in June and July

The bear market mentality developed over the past few years has made the improvement in risk appetite in Hong Kong stocks not happen overnight. Hong Kong stocks are expected to spiral upward. Currently, the first phase of the market, driven by bearish correction and expected recovery in Hong Kong stocks, has basically come to an end. First, after a sharp rise, profit trading back is normal as the share of short sales transactions and risk premiums fall. Second, overseas investors must wait for data verification of improvements in fundamentals after the policy is implemented. Third, considering the resilience of the US economy and the stickiness of high inflation, long-term interest rates on US bonds remained high above 4% in June and July. The traditional foreign-funded holiday season in June and July may trigger an increase in risk aversion due to “falling into the bag of profits.”

The share of short sales in Hong Kong stocks has declined significantly recently. The correction of “poor expectations” has come to an end, and the market will enter a period of turbulence. When shorting was most crowded in March 2024, single-day short sales accounted for nearly 30% of motherboard transactions. As of May 30, the share of short sales had dropped to 15.8%, which is already below the center since 2018.

The risk premium relative to US bonds has fallen back to 6%, near the low point of the risk premium during the round of rebound from the fourth quarter of 2022 to the beginning of 2023. The further decline in risk premiums depends on stronger fundamentals being driven. The risk premium compared to Chinese bonds was 8.1% as of May 24, and is still above the average since 2018. There is still room for a low risk premium compared to the 2023 round of rebound.

The AH premium fell back to its low level since 2020, and the price-performance ratio of A-shares improved. Hang Seng's Shanghai-Shenzhen-Hong Kong Stock Exchange AH share premium fell from over 55% in February 2024 to 36% on May 24, 2024, the lowest level since 2020. However, it is still in the 61.4% quartile since 2014.

2. The current round of the Hong Kong stock market is more sustainable than the rebound from the end of 2022 to the beginning of 2023. Changes in fundamentals and capital will drive the second phase of the market

2.1. First, compared with the rebound from the end of 2022 to the beginning of 2023, the fundamental trend may not be the same

The end of the rebound from the end of 2022 to the beginning of 2023 was accompanied by the PMI falling again and returning to within the 50 range after two months of rapid backdrawing. In 2023, the Hang Seng Index unanimously expects EPS to be lowered continuously at the beginning of the annual reporting season after a brief period of improvement at the beginning of the year. At the end of 2023, the EPS is expected to drop 8.4% from the high at the beginning of the year.

The core characteristic of the second phase of the current Hong Kong stock market is that it is driven by fundamentals. In particular, improvements in core asset fundamentals may exceed the expectations of overseas investors, triggering a double attack on Davis.

First, the advantages of China's economic decision-making mechanism will begin to be re-recognized and praised. Strength in strategic transformation and tactical flexibility at the bottom line of risk prevention will help the Chinese economy to successfully get out of the painful period of switching between old and new momentum.

The policy was further strengthened to promote the steady and healthy development of the real estate market. On May 17, the central bank issued four new policies to eliminate stocks and optimize the real estate sector, including the establishment of new reloan instruments to collect and save, lower the down payment ratio on the demand side, abolish the lower limit of mortgage interest rates, and lower interest rates on provident fund loans.

Local bond issuance has been slow since 2024. The April Politburo meeting mentioned “speeding up the issuance and use of special bonds”. The issuance of treasury bonds and local bonds began to accelerate in May, and fiscal policy is expected to be further strengthened.

Second, at the mesoscopic level, enterprises have entered a stage where overall inventory removal has ended and the peak growth rate of production capacity expansion has passed, which is conducive to price recovery and a steady recovery in nominal GDP growth. The improvement in the profit growth rate of leading listed companies is even more obvious.

Judging from the 2024 A-share quarterly report, the inventory removal of non-financial companies has ended, and the 2024Q1 inventory slowdown has subsided. The production capacity expansion cycle may also have peaked and declined. Capex's year-on-year growth rate has fallen to a low level, and may turn negative next quarter, driving the fixed asset growth rate downward.

Judging from historical data, the year-on-year growth rate of net profit of Hong Kong stock listed companies is more consistent with the year-on-year PPI growth cycle. When PPI rebounds, it is often accompanied by an improvement in the profit growth rate of Hong Kong stock listed companies.

Third, during the mid-reporting season for Hong Kong stock listed companies in August, the performance guidelines of Hong Kong stock leaders were more optimistic, thus attracting more domestic and foreign investors to increase their holdings of Hong Kong stocks. Currently, investors' profit growth expectations for Hong Kong stocks are not high. The consensus estimate provided by Bloomberg is that the 2024 EPS growth rate is only 5.78% year-on-year, which is even lower than the EPS growth rate in 2023. As nominal GDP steadily rebounds, there is a high probability that subsequent profits of leading companies will exceed expectations.

2.2. Second, compared with the rebound from the end of 2022 to the beginning of 2023, the funding trend may not be the same

The Federal Reserve is still in an austerity cycle in 2023. Interest rates on US bonds are rising, and local interest rates in Hong Kong remain high, which has had a great impact on the liquidity of the Hong Kong stock market.

The top interest rate on US bonds in 2024 confirmed that US inflation and economic data are expected to decline in the third quarter. The Federal Reserve is expected to usher in “forward-looking and preventative interest rate cuts” in September. Even if interest rates are not cut in September, weakening data will help raise expectations of interest rate cuts, thus driving the decline in interest rates on US 10-year treasury bonds.

In the second half of the year, US consumer demand was suppressed by high interest rates and excess savings were exhausted in the first quarter. As the Federal Reserve's interest rate cut is postponed, the long-term interest rate on US bonds has once again risen to a high level of more than 4%. Financial conditions for US stocks are tightened, and the suppression of the US economy by high interest rates will become more obvious.

As the general election approaches in the third quarter, party disputes influence fiscal stimulus. Last year's US fiscal stimulus, especially the inertial effect brought about by raising the personal tax threshold, gradually weakened, all of which may cause the momentum of the US economy to weaken month-on-month.

From a year-on-year perspective, considering the high base for the second half of 2023, the year-on-year growth rate of the US economy will also decline in the second half of this year.

The Hong Kong Interbank Discount (HIBOR) generally follows the trend of interest rates on US bonds. Therefore, when interest rates on US bonds decline, it is also beneficial for Hong Kong capital interest rates to decline, making the capital side of Hong Kong stocks easier. The inversion of interest spreads between China and the US is also expected to improve, which will not only help stabilize the RMB exchange rate, but also help increase the attractiveness of allocating RMB assets.

3. Investment Strategy: Safely hold high-dividend assets in Hong Kong stocks during periods of shock, and allocate core assets on dips

3.1. Allocation of high-dividend assets in Hong Kong stocks: dividend ratios are still attractive, benefiting from the potential possibility of optimizing tax arrangements for connected dividends

The high-dividend assets of Hong Kong stocks are still very attractive to allocation-based capital in mainland China. We will continue to focus on high-yield stocks in the energy, telecommunications and other industries where the AH dividend ratio gap is still large. As of May 29, 2024, the dividend rate of the Hang Seng Hong Kong Stock Connect High Dividend Low Volatility Index was 6.63%. The spread with the 10-year Chinese Treasury Bond yield reached 4.36 percentage points, and is still at a historically high quantile level.

Compared to the high-dividend “pure debt” allocation strategy of central state-owned enterprises that we have continued to recommend since the beginning of 2022, 2024 can be optimized into a “convertible bond” allocation strategy to allocate high-dividend assets with improved fundamentals or that can exceed expectations. One category is the target of benefiting from rising prices and positive free cash flow. Profits have upward elasticity and can increase dividends, such as utilities. Another category is high-dividend assets in Hong Kong stocks that have more momentum to repair “poor expectations”, such as the real estate industry chain. If real estate inventory removal progresses smoothly, then real estate, properties, non-ferrous metals, construction, and building materials related to the real estate industry chain are likely to exceed expectations.

3.2. Core assets of Hong Kong stocks in a new era with a more flexible layout on dips

The core assets of Hong Kong stocks in the new era mean that they have good cash flow to support dividends and the sustainability of performance (dividend rate+repurchase yield of 3% or more), and can have a significant performance growth rate in the future (performance growth rate of not less than 10%, high standards above 15%). Thus, the comprehensive return from dividends, repurchases, and net profit growth can at least exceed 15%, and the high standard is above 18%. Among them, good cash flow supports dividends and the sustainability of performance, and is also a sign that the equity culture is maturing; if the compound annual growth rate of performance continues to exceed 15%, the dividend rate and repurchase yield can be 0. After all, the 15% performance growth rate is equivalent to 2 or 3 times the GDP growth rate, which is difficult. The point is that the comprehensive return from dividends, repurchases, and net profit growth can at least exceed 15%, and the high standard is above 18%.

After more than 4 years of in-depth adjustments, the restructuring of the valuation system of the most competitive leaders in the Hong Kong stock industry has been completed. Even in terms of pessimistic performance expectations, the valuation is not high. Take Internet companies as an example. The 2024 PE valuation of major Hong Kong stock Internet companies is in the range of 10-20 times, PEG is between 0.28-2, and PS/G is no higher than 0.5 times.

As the economy stabilizes and improves in the second half of the year, good companies are expected to usher in a moment where “fundamental data is not as bad as previously expected” to “fundamentals continue to improve.”

The core assets of Hong Kong stocks in the new era focus on TMT leaders such as the Internet, beneficiaries of new trends in domestic demand, winners in the overseas industry chain, and “leftovers are king” opportunities in fields with good upstream supply and demand relationships.

Selected TMT leaders such as the Internet. The valuations of leading Hong Kong internet companies have entered the logic of value stocks, and the share of short sales is still too high. With the optimization of the competitive landscape of the industry, the profitability and stability of leading Internet companies continues to improve, and dividends and repurchases are increasing.

Beneficiaries of new trends in domestic demand (cost-effective consumption+technological breakthroughs), selected new winners in the textile and clothing, education, service industries, food and beverage, advanced manufacturing, pharmaceuticals, etc.

A selection of overseas “winners”, focusing on the winners of overseas industry chains such as power tools, home appliances and furniture, the Internet, consumer electronics, electric vehicles, and clean energy industries.

Select the “leftovers are king” in the field of upstream resources and energy, which have financial attributes and are in a tight balance between supply and demand.

4. Risk warning

Power game risk: Geopolitical risk, as well as the risk of friction or sanctions in economic, trade, technology, finance, etc.

The risk that US monetary policy exceeds expectations: the risk that the Fed will not cut interest rates and the risk of causing turmoil in local financial markets.

There is a risk that the decline in economic growth will exceed expectations.

edit/lambor