To the annoyance of some shareholders, Ginkgo Bioworks Holdings, Inc. (NYSE:DNA) shares are down a considerable 34% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 65% loss during that time.

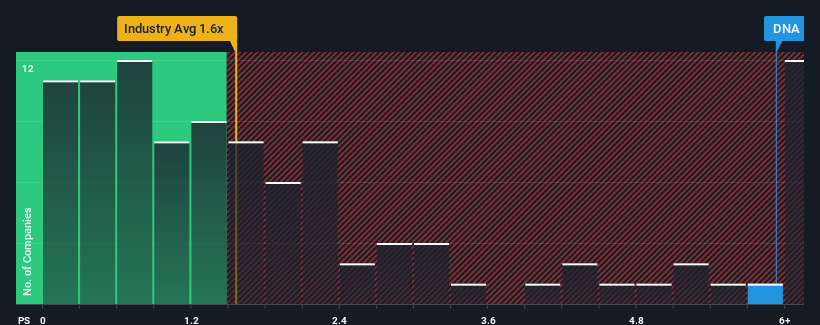

In spite of the heavy fall in price, given around half the companies in the United States' Chemicals industry have price-to-sales ratios (or "P/S") below 1.6x, you may still consider Ginkgo Bioworks Holdings as a stock to avoid entirely with its 5.9x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

What Does Ginkgo Bioworks Holdings' P/S Mean For Shareholders?

Recent times haven't been great for Ginkgo Bioworks Holdings as its revenue has been falling quicker than most other companies. Perhaps the market is predicting a change in fortunes for the company and is expecting them to blow past the rest of the industry, elevating the P/S ratio. If not, then existing shareholders may be very nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Ginkgo Bioworks Holdings will help you uncover what's on the horizon.Is There Enough Revenue Growth Forecasted For Ginkgo Bioworks Holdings?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Ginkgo Bioworks Holdings' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 46% decrease to the company's top line. Still, the latest three year period has seen an excellent 109% overall rise in revenue, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Shifting to the future, estimates from the seven analysts covering the company suggest revenue should grow by 24% per annum over the next three years. With the industry only predicted to deliver 7.5% per annum, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Ginkgo Bioworks Holdings' P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What Does Ginkgo Bioworks Holdings' P/S Mean For Investors?

Ginkgo Bioworks Holdings' shares may have suffered, but its P/S remains high. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Ginkgo Bioworks Holdings maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Chemicals industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Plus, you should also learn about these 4 warning signs we've spotted with Ginkgo Bioworks Holdings.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.