After the US stock market on Thursday May 30, Dell Technology, a leading PC and server manufacturer that has been in business for 40 years, released its financial report for the first quarter of the 2025 fiscal year. Before the earnings report, mainstream Wall Street investment banks raised their target prices one after another.

Although Dell's total revenue and segmented business revenue both exceeded expectations, the backlog of AI server orders reached 3.8 billion US dollars or a 30% quarter-on-quarter increase, it failed to impress investors with high expectations for AI, and adjusted EPS profits declined, and the stock price plummeted by nearly 18% after the market.

Other analysts say that Dell did not directly provide performance guidance for the next quarter in the earnings statement, which also led to a sharp drop in stock prices, but Dell said it will provide guidance during the earnings call.

Dell closed down 5.18% on Thursday, stopping the longest ten-month cycle of six consecutive gains. Yesterday, it reached a record high for four consecutive trading days. Since this year, Dell's stock price has doubled and increased by more than 120%, far exceeding the 11% increase in the S&P 500 market during the same period.

According to some analysts, with the AI “Dongfeng”, the continued improvement in Dell's growth prospects will continue to support the stock price hovering at a new high. The fact that its valuation is lower than other popular AI technology stocks, and market speculation that it will soon be included in the S&P 500 index will benefit the stock price.

Currently, Dell's price-earnings ratio is 22 times the expected earnings. Compared to the Nasdaq 100 Index, which has more technology stocks, and other AI companies such as Nvidia, Ultramicomputer, and Microsoft, all have significant discounts, but it is already 5.8 times higher than Dell's five-year average and is at its highest level.

According to this, asset management agency Deepwater Asset Management refers to Dell as “both a growth stock and a value stock”. Compared to other artificial intelligence companies, the price-earnings ratio is still very low, and the growth potential of its PC and server business is underestimated.

Q1 revenue increased year over year for the first time in two years, but adjusted EPS profit was slightly lower than some market expectations

The market is paying close attention to Dell's ability to expand its AI business. In fact, Dell's current quarterly report has completely surpassed market expectations.

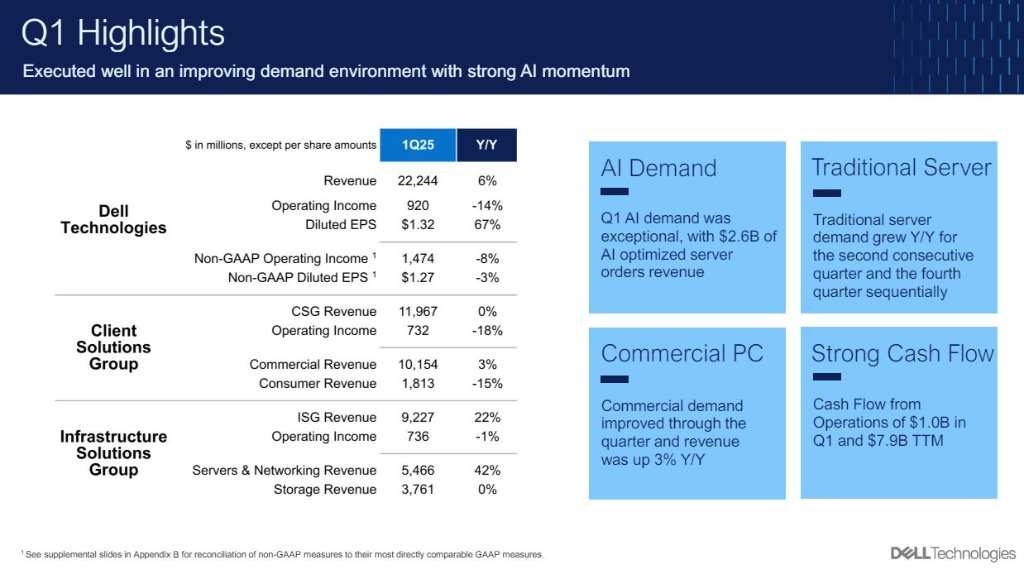

Quarterly revenue increased 6% year over year to US$22.2 billion, higher than market expectations of US$21.6 billion, and above the upper limit of the range of US$21 billion to US$22 billion according to the company's official guidelines. According to some analysts, this is Dell's first year-on-year increase in revenue since 2022.

Adjusted earnings per share were $1.27, down 3% year over year, but higher than market expectations of $1.23 and the company's official guidance of $1.15. However, there are also analysts who want EPS at $1.29. Earnings per share under GAAP increased 67% year over year to $1.32.

Meanwhile, quarterly operating profit was US$920 million, and non-GAAP operating profit was US$1.47 billion, down 14% and 8%, respectively, from the previous year, and the latter fell short of expectations of US$1.48 billion. Cash flow from operating activities was $1 billion. Shareholders were returned $1.1 billion through share repurchases and dividends, and total cash and investments at the end of the quarter were $7.3 billion.

Shipments of AI-optimized servers doubled month-on-month, driving server and network revenue to a new high of 42%

Dell's business consists mainly of two parts: Customer Solutions Group (CSG) and Infrastructure Solutions Group (ISG). The former is mainly personal computers and PCs, which are subdivided into commercial customer and consumer revenue, while the latter is divided into server, network, and storage revenue.

Infrastructure Solutions Group's revenue for the first fiscal quarter increased 22% year over year to US$9.2 billion, higher than market expectations of US$9.06 billion. Among them, server and network revenue increased 42% year over year to a record high of 5.5 billion US dollars. Storage revenue remained flat at $3.8 billion.

According to the company, this is mainly due to strong demand for AI-optimized servers and traditional servers:

Shipments of AI-optimized servers increased by more than 100% from the previous quarter, or doubled to US$1.7 billion. The backlog of orders for such servers jumped 30% month-on-month to US$3.8 billion from US$2.9 billion at the end of January.

However, some analysts pointed out that although Dell's AI server backlog is growing rapidly quarterly, as can be seen from the sharp double-digit stock price dive after the market, the current $3.8 billion backlog order failed to impress investors who had high hopes for the company's AI technology.

Meanwhile, Client Solutions Group's revenue remained flat at $12 billion year over year, but higher than Wall Street's estimate of $11.7 billion. Among them, commercial customer PC revenue increased 3% year over year to 10.2 billion US dollars, while consumer PC revenue fell 15% to 1.8 billion US dollars. According to some analysts, this indicates that some commercial customers have begun to replace aging PC hardware.

The Dell CFO notes that artificial intelligence continues to drive new growth, and financial reports prove the company's ability to execute and provide strong cash flow. The past 12 months generated $7.9 billion in cash flow from operations.

The company's chief operating officer emphasized:

“No company is better equipped to bring artificial intelligence to the enterprise than Dell. Servers and networks hit record revenue in the first fiscal quarter. Our AI-optimized server orders grew to $2.6 billion quarter over quarter, and shipments increased by more than 100%.”

What do you think of Wall Street?

The day before the earnings report was released, Bank of America securities analyst Wamsi Mohan raised Dell's target price from $130 to $180 and reiterated the “buy” rating. The reason was that Dell was undervalued and underheld by investors. The company had potential growth catalysts such as artificial intelligence, and the stock price had room to rise due to possible inclusion in the S&P market.

Last week, Dell launched five new artificial intelligence personal computers (AI PCs), AI servers, all-flash file storage, and network architectures. It also announced an expansion of cooperation with Nvidia to build large-scale end-to-end systems for enterprises through the Dell AI Factory (Dell AI Factory).

Based on this, Bank of America believes that the expansion of the AI product portfolio, as well as the demand for artificial intelligence servers, storage requirements driven by IBM mainframe updates, and the switching cycle of personal computers assisted by AI will all support Dell's growth in 2025:

“Dell benefits from data centers being upgraded infrastructure to support generative artificial intelligence, as well as the introduction of AI PCs. A broad product portfolio, the advantages of artificial intelligence, faster growth than the market, continued share acquisition, and profit growth opportunities brought about by the migration of storage, PC and server configurations to the high-end in the next few years can offset risks such as a slowdown in the global economy and high financial leverage.”

Morgan Stanley expects the penetration rate of artificial intelligence PCs to be 2% this year, rise sharply to 16% next year, and increase to 28% by 2026. Research firm Canalys is more optimistic. It is estimated that by 2025 there will be 100 million personal computers equipped with artificial intelligence, accounting for about 40% of the market share. This will benefit PC manufacturers such as HP and Dell. Yesterday's earnings report said that HP PC sales will increase for the first time in two years.

Hunter Wolf Research notes that Dell has been collaborating with major GPU manufacturers to launch AI-optimized servers, which may change its growth prospects. For example, Dell recently announced that it will provide Nvidia's next generation of the most powerful Blackwell GPUs in servers.

Investment bank Evercore ISI recently raised Dell's target price from 140 US dollars to 165 US dollars, saying that Dell has won a large part of Tesla's artificial intelligence server construction business, or brought revenue opportunities of 2.5 billion to 3 billion US dollars, which may be realized this year.

Investment management company Neuberger Berman said “Dell is becoming an increasingly important strategic supplier to the AI ecosystem,” but the strong growth momentum of AI may also slow down with the macroeconomic downturn, that is, the demand for AI systems is still cyclical.

edit/ruby