Source: CICC Strategy

summary

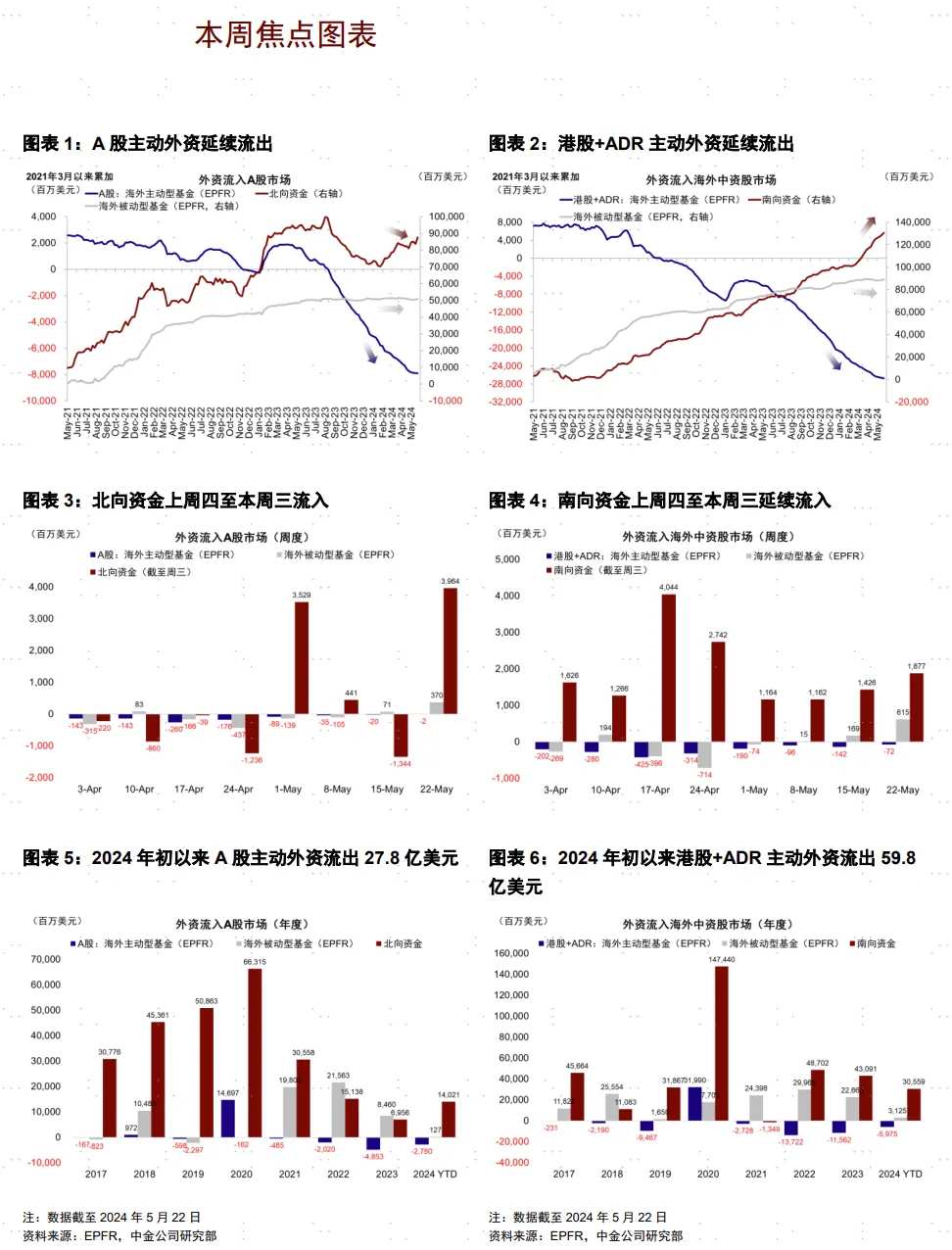

Notable changes in global capital this week are: 1) The EPFR capital data we are tracking shows that as of Wednesday (May 22), active overseas capital continued to flow out of A-shares and Hong Kong stocks, and passive capital flows clearly returned; 2) in terms of connectivity, north-south capital inflows have slowed this week; 3) global markets, stocks and bonds have maintained inflows, and the money market has turned out; 4) US stocks have turned into inflows, and outflows from Japan, developed Europe and emerging markets have continued.

In terms of domestic capital, outflows of active foreign capital have narrowed, while inflows of passive foreign capital have accelerated. As of this Wednesday (May 16 to May 22), the total outflow of active capital from the A-share and Hong Kong stock markets was US$70 million, a slowdown from last week's outflow of US$162 million. At the same time, passive capital inflows into US$980 million were the most obvious.

However, looking at the market, there was a clear correction last week. Why was there such an obvious divergence? We think the reason is that, on the one hand, the EPFR statistical period is from Thursday to Wednesday. The Hang Seng Index rose 0.6% and the Shanghai and Shenzhen 300 Index rose 1.6% during this period. On the other hand, it also shows that capital inflows are lagging behind. We have suggested in previous reports that the first stage of the Hong Kong stock market is around 19,000-20,000 points if it is only driven by an improvement in risk appetite and rebalancing capital in some regions. Currently, this view is also basically confirmed, and subsequent larger and more continuous capital inflows and increases will still require significant improvements in fundamentals.

In terms of global capital, foreign capital has actively flowed out of Japanese stocks, US stocks have turned into inflows, and India's inflows have narrowed. As of this Wednesday (May 16 to May 22), active foreign capital inflows to the Indian market have slowed this week, with an overall inflow of 120 million US dollars (vs. last week's inflow of 270 million US dollars); in terms of Japanese stocks, active foreign capital continued to outflow 320 million US dollars this week, which is narrower than last week (vs. 460 million US dollars outflow last week). At the same time, active foreign capital was transferred to US stocks, and the inflow volume was about 890 million US dollars.

body

Large inflows of passive foreign capital

Chinese market

Overseas capital: Overall inflows continued, and active foreign capital outflows narrowed. As of this Wednesday (May 16 to May 22), active foreign capital outflows from A-shares were US$2.41 million (vs. last week's outflow of US$20.04 million), and passive capital inflows accelerated to US$370 million, with an overall inflow of US$370 million (vs. last week's net outflow of US$50 million). Meanwhile, overseas capital from Hong Kong stocks and ADR continued to flow in US$540 million (vs. last week's net inflow of US$0.3 million), with active capital outflows of US$70 million (vs. US$140 million last week), and passive capital inflows of US$610 million.

Interconnected capital: Northbound inflows have slowed, and banks have increased their holdings a lot. This week (May 20 to May 24), the total net inflow of northbound capital was RMB 840 million, with an average daily inflow of RMB 170 million (vs. average inflow of RMB 2.19 billion on Sunday from May 13 to May 17). By industry, the market value of shares held by banks and other sectors has risen a lot, while the market value of shares held by sectors such as household appliances and automobiles has declined. In terms of individual stocks, this week, Northbound Capital increased its holdings of Ningde Times, Changjiang Electric Power, and Anke Innovation a lot, and reduced its holdings of shares such as Guodian Nanrui, Hengrui Pharmaceutical, and Well shares.

Southbound inflows continued, with mainland banks and energy/raw materials having the highest growth rate. This week (May 20 to May 24), the total southbound inflow was HK$10.64 billion, with an average daily inflow of HK$2.13 billion (vs. the average daily inflow of HK$4.66 billion from May 13 to May 17). At the industry level, mainland banks and energy/raw materials sectors led the rise in market value, while diversified finance and other sectors saw the highest decline in market value of shareholding. In terms of individual stocks, Southbound Capital increased its holdings in stocks such as Bank of China, China Construction Bank, and Zhongtong Express, and reduced its holdings in stocks such as Meituan, CNOOC, and Xiaomi Group.

Global market

Cross-markets and assets: US stocks turned into inflows, and outflows from developed Europe, Japan, and emerging markets continued. In terms of active foreign investment, US stocks turned to inflows of 891 million US dollars this week (vs. last week's outflow of 523 million US dollars), developed Europe outflows of 382 million US dollars (vs. last week's outflow of 505 million US dollars), the Japanese stock market continued to outflow 316 million US dollars (vs. last week's outflow of 459 million US dollars), and emerging markets continued to have outflows of 466 million US dollars (vs. last week's outflow of 433 million US dollars). In terms of assets, the global stock and bond markets continued to flow in, and the money market turned to inflows.

Allocation ratio: As of March 31, the allocation ratio of active funds to China was about 0.2% lower than the benchmark. Since 2021, global active funds have switched from overallocation to underallocation to China and India, South Korea has maintained overallocation, and Japan's underallocation has declined. Since January 2022, China's allocation ratio has declined a lot (-0.2%), while the United Kingdom (+1.0%), France (+0.5%), and Japan (+0.3%) have received the biggest increases. In terms of regional types, funds from managers from Europe are the main outflows; at the sector level, overseas capital is overallocated to China's healthcare, consumption, semiconductors, hardware, and capital goods, and is underallocated to the Internet, finance, and real estate.

Chart: Passive capital inflows drive the overall return of foreign capital

editor/tolk