Source: Semiconductor Industry Watch

Over the past five years, since Nvidia bought InfiniBand and Mellanox, an Ethernet switch and network interface card supplier for $6.9 billion, people have been wondering what the differences between computing and networking are in Nvidia's data center business, which has exploded and now accounts for most of each quarter's revenue.

Now we know.

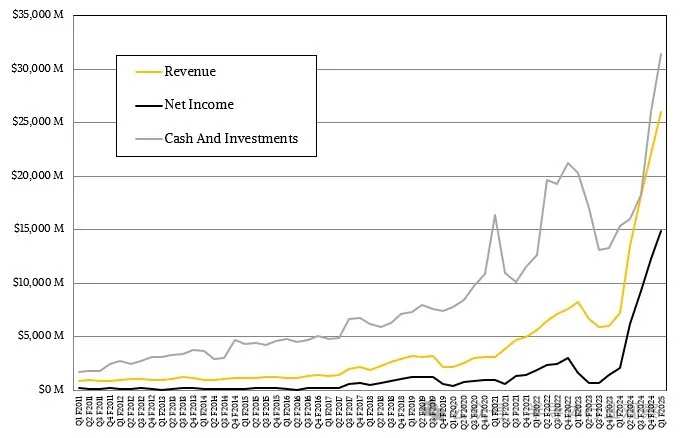

Every quarter, Collette Kress, Nvidia's chief financial officer, publishes a review with financial results for every 13 weeks, which reveals which products are selling well and by how much. As we all know, Nvidia just announced its quarterly results for the end of April, the first quarter of its fiscal year 2025, and these numbers are as good as expected. In the review, Kress revealed the actual revenue of its computing and networking division, which are different from each other and the graphics division.

Actual data for the first and fourth quarters of FY2024 and the first quarter of FY2025 shows that the computing business may be stronger than many expected, while the network business is slightly weaker. But both are clearly strong, and they will continue to strengthen as the 2025 fiscal year begins. The generative AI market is growing so fast that even intense competition can't dampen the market momentum of the CUDA platform that Nvidia has created over the past two decades, which has an incredible advantage over other platforms in the HPC and AI space.

But as we've said before, we think we're now at the peak of Nvidia, and maybe this feast will continue until fiscal year 2026. But eventually, competition will come, the hype and hope for generative artificial intelligence will subside, and AMD, Intel, Arm Group, and others will get their share of the market. Prior to that, this was a time for Nvidia to take advantage of the tall grass and the sun was shining.

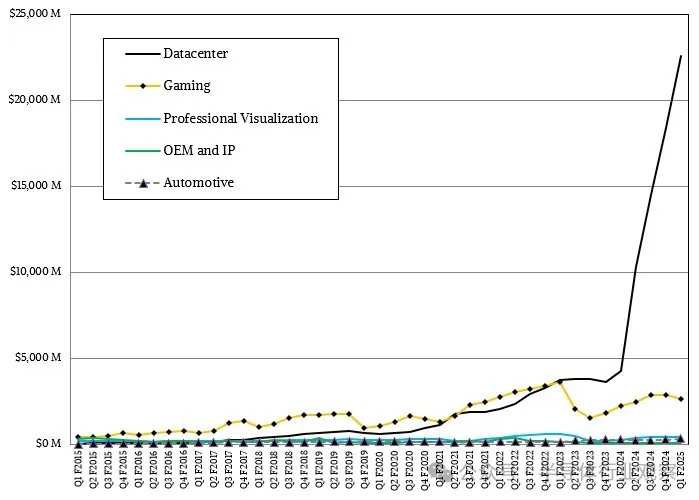

And Nvidia did succeed in the data center space.

Nvidia has two different and nearly identical methods to break down its data center business.

Some computing and networking products are sold outside of data centers, but not many, while some products sold in data centers are based on game cards, so the data center division's revenue is slightly different from the computing and networking division.

To be precise, the data center division's sales for the first quarter were $22.56 billion, up 5.3 times year over year and 22.6% month over month. In a conference call with Wall Street analysts, Kress said that about 40% of the company's data center division's revenue comes from cloud builders, and we estimate this ratio to be about 46%, or $10.38 billion, which is 10 times higher than the same period last year according to our model. This meant that the remaining $12.18 billion in data center product sales went to hyperscale enterprises (such as Meta Platforms), HPC centers, enterprises, and other organizations, growing only 3.8 times. (Do you understand what we mean by standardizing multiples? (In the company's 500-year history, this kind of multiple was uncommon for most companies.)

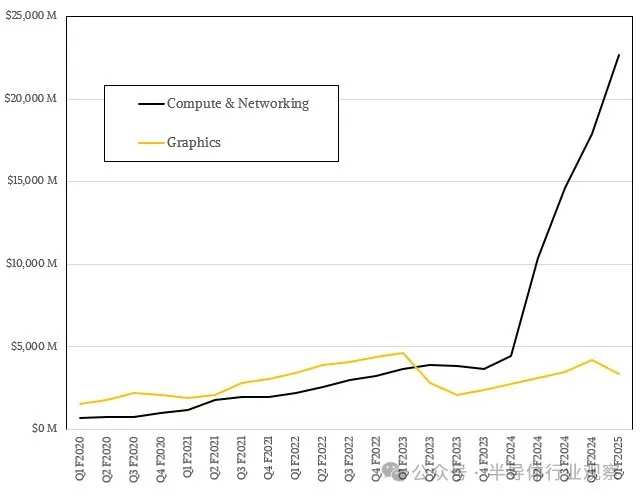

The Computing and Networking Division combines revenue from all graphics products not used in PCs and workstations. In the first quarter, revenue from the computing and networking division was $22.68 billion, up 5.1 times year over year, and up 26.7% from the fourth quarter of 2024, which ended in January. For a short period of time, Nvidia provided revenue for its division, but it hasn't done so in a while.

Nvidia said in its financial report that sales of its data center computing products (mainly “Hopper” GPUs and related platform components) increased 5.8 times in the first fiscal quarter to reach $19.39 billion, and also increased 28.7% month-on-month compared to the first quarter of the previous fiscal year. If a company is hugely successful, it's lucky to have this kind of growth every year.

For networking products, revenue increased only 2.4 times to $3.17 billion, but revenue declined 4.8% from the previous quarter due to the supply of InfiniBand products falling short of demand and production of Spectrum X Ethernet products not yet reaching a significant level.

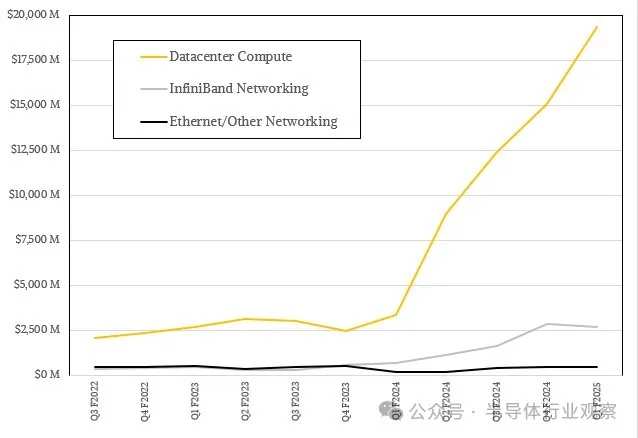

Our model shows that in the first quarter of 2025, InfiniBand's sales increased 2.7 times to $2.71 billion, but fell 5% month-on-month, accounting for 85.5% of network sales. Ethernet and NVSwitch sales accounted for the remaining portion of network sales of $459 million, up 2.14 times year over year but down 3.6% month over month.

Nvidia is fully embracing Ethernet in the data center with Spectrum X, and as we've indicated before, it has no choice because hyperscale enterprises and cloud builders want it now, and most businesses are absolutely allergic to InfiniBand. They wanted a network, and that was Ethernet. As a result, Ethernet switching from all major vendors will become more like a single fabric.

“Spectrum-X sales are growing, and customers include multiple customers, including a large cluster with 100,000 GPUs,” Kress said during the Wall Street conference call. “Spectrum-X opens up a whole new market for Nvidia networks and enables Ethernet data centers to accommodate AI at scale. We expect Spectrum-X to jump to a multi-billion dollar product line within a year.”

Nvidia didn't talk about how the adoption of Ethernet would affect InfiniBand sales, but it would clearly have a cannibalizing effect. It remains to be seen how big the impact will be.

Meanwhile, Nvidia spent $7.8 billion this quarter on share buybacks (not only as an investment, but as a way to give away shares as part of a compensation plan) and dividends, and will split the stock by 10 to 1 on June 10, bringing its share price closer to the $100 mark. This is a comfortable figure for institutional and individual investors, which will help further push Nvidia's stock price higher. However, Nvidia's huge success in FY2025 and 2026 is what really drove Nvidia's stock price to rise further. Nvidia's sales for the second fiscal quarter are expected to be $28 billion, fluctuating 2%, and we think Nvidia's sales will easily surpass $100 billion this year. Anyone who can draw four dots on a line would think so.

This journey isn't over yet. But that's definitely the exciting part.

Nvidia co-founder and CEO Wong In-hoon briefed everyone on the current situation at the end of the conference call, so let's talk about it:

“We have a rich ecosystem of customers and partners who will announce the launch of our entire AI factory architecture to market. So for companies that want ultimate performance, we have the InfiniBand computing structure. InfiniBand is a computing structure, and Ethernet is a network. Over the years, InfiniBand began as a computing structure and later became a better and better network. Ethernet is a network, and with Spectrum-X, we're going to make it a better computing structure. We are committed — fully committed — to all three. From an NVLink compute structure for a single compute domain to an InfiniBand compute structure to an Ethernet network compute structure. Therefore, we will promote the development of these three links at a very rapid pace. As a result, you'll see new switches, new NICs, new features, and a new software stack running on all three. New CPUs, new GPUs, new network NICs, new switches — lots of chips are coming soon. Best of all, they all run CUDA, and they all run our entire software stack. So if you invest in our software stack today, it will get faster and faster without having to do anything. If you invest in our architecture today, you don't have to do anything, it will go into more and more clouds and more data centers, and everything will work. As a result, I think the pace of innovation we are bringing will increase capacity on the one hand, and lower TCO on the other. So we should be able to use the Nvidia architecture to expand this new era of computing and launch this new industrial revolution. We're not just making software, we're making artificial intelligence tokens, and we're going to do that on a large scale.”

This market is growing so fast that everyone can participate in it. But Nvidia will still be the biggest winner for at least the next few years.

edit/lambor