Unfortunately for some shareholders, the KLX Energy Services Holdings, Inc. (NASDAQ:KLXE) share price has dived 30% in the last thirty days, prolonging recent pain. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 41% in that time.

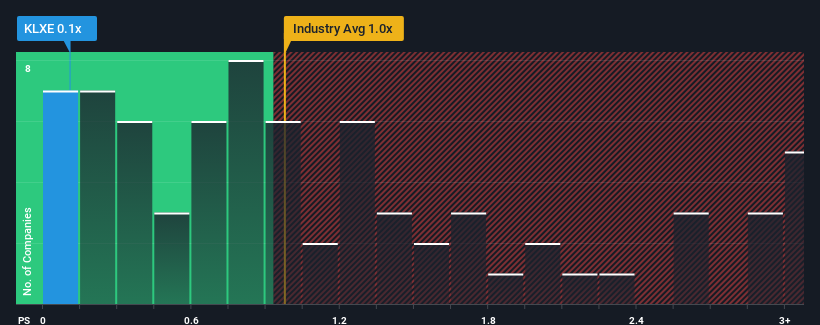

Since its price has dipped substantially, considering around half the companies operating in the United States' Energy Services industry have price-to-sales ratios (or "P/S") above 1x, you may consider KLX Energy Services Holdings as an solid investment opportunity with its 0.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

NasdaqGS:KLXE Price to Sales Ratio vs Industry May 23rd 2024

What Does KLX Energy Services Holdings' Recent Performance Look Like?

KLX Energy Services Holdings could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on KLX Energy Services Holdings.

Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, KLX Energy Services Holdings would need to produce sluggish growth that's trailing the industry.

Retrospectively, the last year delivered a frustrating 5.2% decrease to the company's top line. Even so, admirably revenue has lifted 189% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the two analysts covering the company suggest revenue growth is heading into negative territory, declining 6.9% over the next year. That's not great when the rest of the industry is expected to grow by 11%.

With this information, we are not surprised that KLX Energy Services Holdings is trading at a P/S lower than the industry. However, shrinking revenues are unlikely to lead to a stable P/S over the longer term. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Key Takeaway

KLX Energy Services Holdings' recently weak share price has pulled its P/S back below other Energy Services companies. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

With revenue forecasts that are inferior to the rest of the industry, it's no surprise that KLX Energy Services Holdings' P/S is on the lower end of the spectrum. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 4 warning signs for KLX Energy Services Holdings (1 is concerning!) that you need to be mindful of.

If these risks are making you reconsider your opinion on KLX Energy Services Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.