① On May 22, Minsheng Bank posted an article on its official website stating that the bank will adjust RMB unit agreement deposits, RMB liquid profit products, and smart notification deposits. ② Since late April, a number of banks have continued to lower interest rates on Chinese unit agreement deposits to 1.15%. ③ A number of banks have lowered interest rates on unit agreements, which is closely related to the requirements of the regulatory authorities. I believe more banks will follow suit in the future.

Financial Services Association, May 23 (Reporter Peng Kefeng) Following the centralized removal of smart notification deposit products, many banks continued to centrally adjust “high-interest” deposit products such as public agreement deposits. On May 22, Minsheng Bank posted an article on its official website stating that due to policy changes, product agreement agreements, and business adjustment needs, the bank will adjust RMB unit agreement deposits, RMB liquid profit products, and smart notification deposits.

Today, a Financial Services Association reporter's inquiry found that since late April, many banks have continued to lower interest rates on deposit agreements in people's units to 1.15%. This means that high-interest deposit collection products common in the banking industry in the past will lose another “powerful tool.”

Minsheng Bank issued a document to adjust three types of high-interest deposit products

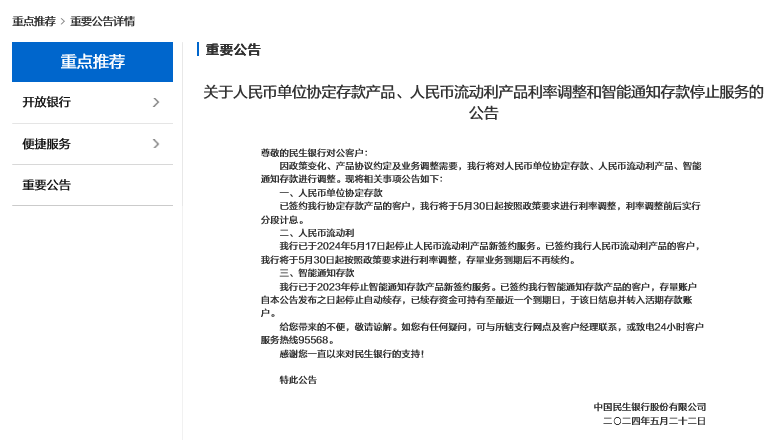

Yesterday, Minsheng Bank posted an article on its official website stating that it will adjust RMB unit agreement deposits, RMB liquid profit products, and smart notification deposits.

Among them, for RMB unit agreement deposits, the bank will adjust interest rates in accordance with policy requirements starting May 30, and implement instalment interest accrual before and after the interest rate adjustment; for RMB liquid products, the bank will stop the new contract service for RMB liquidity products on May 17, 2024. For customers who have signed up for our RMB liquidity products, banks will adjust interest rates in accordance with policy requirements starting May 30, and will not renew their contracts after the stock business expires.

Furthermore, for smart notification deposit products, Minsheng Bank stopped the new contract service for smart notification deposit products in 2023. Customers who have signed up for the bank's smart notification deposit products will stop automatically renewing their stock accounts from the date of publication of this announcement. Renewed funds can be held until the most recent maturity date, and interest will be settled and transferred to current deposit accounts on that day.

A Financial Services Association reporter noticed that there is not much difference between RMB unit agreement deposit products and RMB liquid profit products; they can basically be viewed as similar products. According to the official website of Minsheng Bank, “liquid profit” includes various types of product segments such as liquid profit B, liquid profit C, liquid profit E, and liquid profit D.

Among them, “Liquid Profit C” provides customers with smart RMB deposit value-added services. On the basis of notifications and time deposits within one year (inclusive), value-added income is settled in segments according to the corresponding deposit interest rate during the actual life period of the fund, helping customers obtain higher value-added benefits (RMB only) on the premise of maintaining capital liquidity. This product is suitable for customers with large capital and strong capital liquidity;

Public “Liquidity B” provides customers with value-added services for smart capital and foreign currency deposits. On the basis of notification deposits, each collected fund is automatically notified and automatically transferred, which avoids extensive manual operation by customers and helps customers obtain higher value-added benefits while maintaining capital liquidity. It is suitable for customers with large capital and strong liquidity. However, “Liquid Interest B” applies to various currencies such as RMB, USD, EUR, HKD, and JPY.

Recently, a number of banks have continued to issue documents to lower interest rates on unit agreements

According to our understanding, an agreement deposit is a type of unit deposit where a unit customer opens a settlement account according to the deposit amount agreed upon with the bank. The bank transfers the portion of the account to the agreement account in RMB units and accrues interest at preferential interest rates.

This morning, a Financial Services Association reporter made an inquiry and found that Minsheng Bank is not the first to lower interest rates on RMB unit agreement deposits. Huaxia Bank, Industrial Bank, etc. have also recently begun to lower interest rates on public deposit products.

On May 13, Huaxia Bank posted an article on its official website stating that it will adjust the maximum interest rate limit for RMB unit agreement deposits. Specifically: Starting from May 15, 2024, the bank's maximum interest rate limit for RMB unit agreement deposits will be adjusted to 1.15%.

On May 15, Industrial Bank issued an announcement on the adjustment of RMB unit agreement deposits. Industrial Bank said that in order to implement the relevant policy requirements, the Bank will adjust RMB unit agreement deposits and single rollover type ordinary notice deposit products for corporate finance customers. For agreement deposits in RMB units, from the date of publication of the announcement, if the customer's agreed deposit interest rate is not the Bank's listed interest rate, the following adjustments will be made: agreement deposits that do not have an agreement validity period of one year; if the customer's RMB agreement deposit interest rate is higher than 1.15%, the agreed deposit interest rate will be uniformly adjusted to 1.15%, and the agreement validity period for a period of one year will be uniformly set. The unified agreement will be effective from May 15, 2024.

Societe Generale Bank also stated that for contract deposits with an agreement validity period: if the customer agreement deposit is signed before December 24, 2023 (based on the Bank's system contract date), and the interest rate is higher than 1.35%, the contract deposit interest rate will be uniformly adjusted to 1.35%; if the customer agreement deposit is signed after December 24, 2023 (based on the Bank's system contract date), and the interest rate is higher than 1.15%, the agreement deposit interest rate will be uniformly adjusted to 1.15%.

In addition, Everbright Bank also recently issued an announcement stating that the bank will make adjustments to products such as RMB agreement deposits and public weekly plans. Starting May 15, if the customer's RMB agreed deposit interest rate is higher than 1.15%, the system will automatically accrue interest in installments and adjust the agreed interest rate to 1.15%. Accounts that have signed Everbright Bank's automatic rollover notification deposit, such as Gongzhou Plan, Gong Smart Deposit A (37-day deposit period), and Gong Smart Deposit B (7-day deposit period), will stop automatically rolling back notification deposits on May 15, and the funds will be transferred back to the contracted current account after the notice deposit that has already been rolled over expires.

Policies continue to suppress high-interest savings accounts, analysts say more banks will follow suit in the future

In response, a banking analyst at a brokerage firm told the Financial Federation reporter that unit agreement deposits are generally placed in settlement accounts. According to current rules, settlement accounts are current accounts. Since banks mainly provide contract deposit services to corporate customers, agreement deposits are also included in the category of corporate current deposits. Therefore, in principle, interest rates on unit agreement deposits cannot be higher than the upper limit of interest rates on current RMB deposits. However, from an objective point of view, banks were constrained by pressure to collect savings, and large enterprises and large units were naturally more capable of bargaining on deposits than individuals, so many banks had to give higher interest rates to unit agreement deposit products. In layman's terms, this is also a high-interest savings package for the public version.

According to an earlier report by a Financial Services Association reporter, in May of last year, the regulation issued a notice to major banks requiring that the self-regulation limits for agreed deposits and notification deposits be implemented from May 15. Among them, some banks in China (specifically referring to the four major banks in industry, agriculture, China, and construction) implement the benchmark interest rate plus 10 BP, while other financial institutions implement the benchmark interest rate plus 20 BP.

However, Wang Yifeng, deputy director of the Everbright Securities Research Institute and chief financial analyst, previously released a research report saying that the bank's cost ratio for official time deposits was clearly high. The interest rate on official time deposits at the end of 2023 was 2.7%. Although there was a slight decrease from mid-year, the decline was significantly lower than the adjustment of listed interest rates. According to a comprehensive assessment, “excessive self-regulation” of public deposit pricing is still quite common.

It is worth noting that at the beginning of April this year, the self-regulatory mechanism for market interest rate pricing issued the “Initiative on Prohibiting Maintaining Competitive Order in the Deposit Market through Manual Interest Rate Compensation and High-Interest Savings Collection”. The initiative clearly requires that banks “must not promise or pay to customers any form of interest that exceeds the authorized limit of deposit interest rates,” and requires banks to rectify this accordingly.

Regarding this, the analysts mentioned above believe that the reduction of interest rates on unit deposits by many banks, such as Minsheng Bank and Industrial Bank, is closely related to the requirements of the supervisory authorities, and it is believed that more banks will follow suit in the future. From the perspective of the regulatory authorities, such high-interest deposit products drive up banks' capital costs and have a negative impact on net interest spreads. From a bank's perspective, lowering interest rates on related products is also beneficial to reducing the pressure on debt costs.

Seen from another perspective, while various forms of high-interest savings packages are constantly being cracked down, some banks are indeed under financial pressure. In response, a macro analyst at a brokerage firm also told the Financial Federation reporter that in the first half of this year, downgrades are still likely to occur, which will further release liquidity for banks.