To find a multi-bagger stock, what are the underlying trends we should look for in a business? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after investigating FMC (NYSE:FMC), we don't think it's current trends fit the mold of a multi-bagger.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on FMC is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.057 = US$477m ÷ (US$12b - US$3.6b) (Based on the trailing twelve months to March 2024).

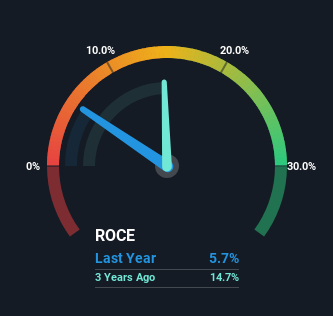

So, FMC has an ROCE of 5.7%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 8.8%.

Above you can see how the current ROCE for FMC compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for FMC .

So How Is FMC's ROCE Trending?

We weren't thrilled with the trend because FMC's ROCE has reduced by 61% over the last five years, while the business employed 27% more capital. However, some of the increase in capital employed could be attributed to the recent capital raising that's been completed prior to their latest reporting period, so keep that in mind when looking at the ROCE decrease. It's unlikely that all of the funds raised have been put to work yet, so as a consequence FMC might not have received a full period of earnings contribution from it.

What We Can Learn From FMC's ROCE

From the above analysis, we find it rather worrisome that returns on capital and sales for FMC have fallen, meanwhile the business is employing more capital than it was five years ago. And long term shareholders have watched their investments stay flat over the last five years. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

On a final note, we found 4 warning signs for FMC (2 are a bit concerning) you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.