The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Frontier Group Holdings, Inc. (NASDAQ:ULCC) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does Frontier Group Holdings Carry?

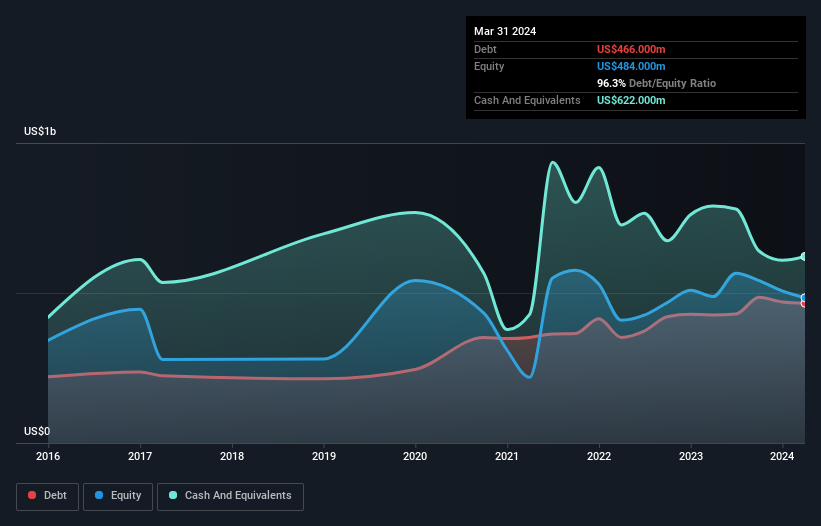

As you can see below, at the end of March 2024, Frontier Group Holdings had US$466.0m of debt, up from US$427.0m a year ago. Click the image for more detail. But on the other hand it also has US$622.0m in cash, leading to a US$156.0m net cash position.

How Strong Is Frontier Group Holdings' Balance Sheet?

We can see from the most recent balance sheet that Frontier Group Holdings had liabilities of US$1.80b falling due within a year, and liabilities of US$2.93b due beyond that. On the other hand, it had cash of US$622.0m and US$173.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.93b.

We can see from the most recent balance sheet that Frontier Group Holdings had liabilities of US$1.80b falling due within a year, and liabilities of US$2.93b due beyond that. On the other hand, it had cash of US$622.0m and US$173.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.93b.

This deficit casts a shadow over the US$1.37b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Frontier Group Holdings would probably need a major re-capitalization if its creditors were to demand repayment. Given that Frontier Group Holdings has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Frontier Group Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Frontier Group Holdings's revenue was pretty flat, and it made a negative EBIT. While that's not too bad, we'd prefer see growth.

So How Risky Is Frontier Group Holdings?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Frontier Group Holdings had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$351m of cash and made a loss of US$24m. However, it has net cash of US$156.0m, so it has a bit of time before it will need more capital. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Frontier Group Holdings that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.