UBS pointed out that the Chinese market sentiment tends to buy when the price of gold recovers. As a result, future investors may be more likely to react flexibly to the price and be willing to buy at a decline of around $2,250 per ounce.

With the record rise in gold prices this year, the market generally believes that Chinese investors have played an important role. The Central Bank of China has increased its gold reserves for 18 consecutive months and has become one of the major central bank buyers receiving much attention; retail investors have shown strong enthusiasm for buying gold ETF products; gold jewelry sales in gold stores are also extremely booming.

At the end of April last year, Wall Street bank UBS visited Beijing and Shanghai, the center of China's gold market, and obtained first-hand market intelligence and customer feedback. Nine months later, at a time when the price of gold was soaring historically, UBS conducted another in-depth investigation into the Chinese market.

UBS pointed out that Chinese investors tend to buy when the price of gold recovers. As a result, future investors may be more likely to react flexibly to the price and be willing to buy at a decline of around $2,250 per ounce.

According to UBS, some investors tend to think that the Fed will not cut interest rates and will maintain a higher level for a longer period of time. This will further support the correction in gold prices, and the reason for holding gold for a long time is still valid.

Chinese market sentiment - buying on dips

China is one of the world's largest consumers and producers of gold: the world produces about 3,500 tons of gold every year, one-third of China's consumer stations produce about 350 tons, and the remaining gap needs to be met by imports.

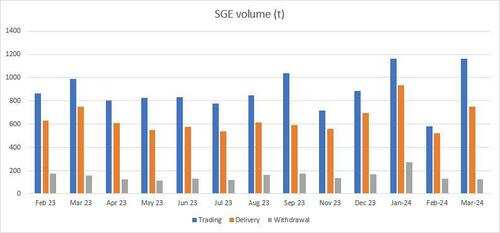

The Shanghai Gold Exchange (SGE) is the main channel for retail imports of Chinese gold. Currently, 15 domestic banks hold gold import licenses, and they import gold through SGE. The standard gold bar required by SGE is a 99.99% pure 1 kilogram gold bar, about the size of an iPhone.

Additionally, four foreign bank subsidiaries in China have import licenses — they are obligated to meet the needs of Chinese companies and carry out SGE/London gold arbitrage transactions when appropriate.

Market demand usually peaks before Lunar New Year and Golden Week. By controlling the amount and timing of import quotas, the People's Bank of China has had a significant impact on market activity.

UBS customers point out that during the recent surge in gold prices, the SGE premium was strong in the London market. At the end of 2023, the SGE premium was once close to $150 per ounce, but it remains above $30 per ounce.

UBS pointed out that the Chinese New Year gold import quota has been used up, but since gold is still irreplaceable for retail investors, potential demand will continue.

Chinese investors tend to buy when the price of gold recovers. As a result, future investors may be more likely to react flexibly to the price and be willing to buy at a decline of around $2,250 per ounce.

Customers are more likely to believe that the Fed will not cut interest rates and will maintain a higher level for a longer period of time. This will further support the correction in gold prices, and the reason for holding gold for a long time is still valid.

The price of gold broke through 2400. Isn't SHFE the key driver?

Recently, the Western view is that the Shanghai Futures Exchange (SHFE) gold contract is a key factor driving the gold price above 2,400 US dollars per ounce. Some commentators pointed out that the trading volume of its gold contracts has risen sharply, and the number of open long positions is surprisingly large.

However, after investigating most customers during the trip to China, UBS discovered that the so-called “effect of the previous period” seemed to be a pure coincidence, and there was no definitive causal relationship.

Domestic banks are the main market makers in the Shanghai Futures Exchange (SHFE) gold futures market. The proprietary trading departments of these banks often carry out a type of arbitrage transaction, that is, a gold spread transaction between SGE and SHFE (similar to gold EFP trading in Western markets). Domestic banks are deeply involved in the SHFE and SGE markets, making their views credible enough.

It is worth noting that in SHFE's gold futures market, most participants do not obtain physical gold, but for the purpose of hedging risks, etc. They usually don't choose to withdraw physical gold when the contract expires.

Instead, these participants tend to “roll” their positions into the next delivery month's contract or close their positions in cash before the contract expires. This means that although SHFE's gold futures trading volume is very large, it actually rarely involves the delivery of physical gold.

Since SHFE's gold futures contracts rarely involve physical delivery, it lacks direct links and interchangeability with other major global physical gold markets (such as the London Gold Market and COMEX Gold Futures Market).

This lack of interchangeability means that although SHFE's gold futures trading volume is high, its impact on actual global gold supply, demand, and price is very limited.

Notably, in SHFE's gold market, participants rarely make physical deliveries, and positions are usually rolled or closed in cash. As a result, given the lack of interchangeability with the London gold and COMEX gold futures markets, SHFE's impact is minimal.

Earlier media articles pointed out that in recent months, a large number of long open positions have been accumulated, equivalent to 300 tons of gold, but there is no mention of net long open positions; currently, it is equivalent to 100 tons of gold. In contrast, COMEX Gold, the most liquid global contract, currently has a net speculative long of 700 tons.

Compared to SHFE, the COMEX gold market is much larger.

edit/emily