Source: Zhongjin Dim Sum

Authors: Sun Yuanqi, Li Hao, Zhang Yu, etc.

summary

Policy highlights: On May 17, the State Council's policy routine briefing mainly discussed policies in the four areas of insurance delivery, acquisition of existing commercial housing, revitalizing existing land, and mortgages. We believe that the highlight is that the collection and storage mechanism may be effective in mitigating the cash flow risk of housing enterprises and consolidating financial stability; the lower down payment ratio is the lowest in history, and the lower interest rate limit for personal housing loans has been lifted, and the credit policy adjustments have exceeded expectations.

Market outlook: We believe that the downward slope of the market in the early stages has moderated marginally, and the recent centralized introduction of policies is expected to speed up the cycle. We judge that the current real estate cycle within the 6-12 month dimension is expected to usher in a turning point to end the rapid adjustment period of more than 3 years since 2021. In the next 3 years, we believe that China's real estate will enter an aggressive stage of “inventory removal and deleveraging” to gradually restore the industry's production capacity and various activity levels while continuously preventing and securing the bottom line of financial risks.

Investment outlook: We believe that Chinese real estate stocks can confirm the bottom of the long cycle, or in the near future will usher in a valuation repair due to a turning point in the real estate cycle. Recently, due to strong policy adjustments, the deal may be ahead, but we believe there is still room for further upward movement. However, as to whether it will be interpreted as a continuous upward trend similar to 2015-2017, we currently believe that the probability may be limited.

risks

Policy implementation fell short of expectations; housing price adjustments were deeper than expected.

body

The real estate cycle may face a turning point, and sector revaluation is expected to continue

Policy and market outlook

With the recent promulgation of a series of major real estate policies, we believe this cycle is one step closer to the inflection point.

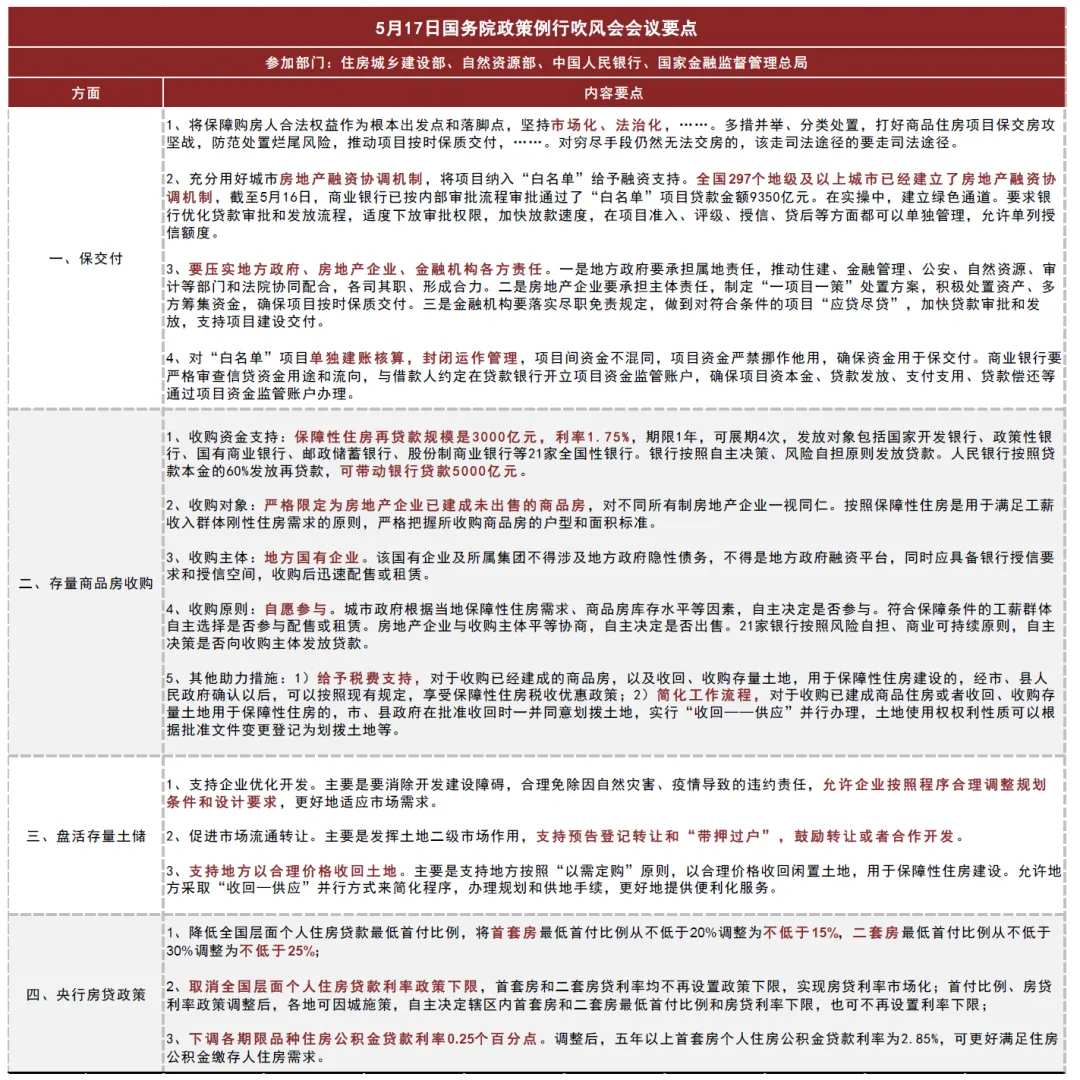

What are the new policies? On May 17, the State Information Office held a regular briefing on the State Council's policies to introduce “the situation relating to the effective implementation of supporting policies for housing delivery”. The main policy elements mentioned during the meeting include (see Chart 1 for details):

► Further promote the implementation of guarantee delivery. The conference emphasized the combination of measures, classification and disposal, making full use of urban real estate financing coordination mechanisms, and compacting the responsibilities of local governments, real estate enterprises, and financial institutions. We believe that the relevant content principles are consistent with the previous ones.

► Purchase of existing commercial housing. In terms of capital, it will provide reloans of 300 billion yuan for affordable housing. The People's Bank of China will issue reloans based on 60% of the loan principal amount, which can drive bank loans of 500 billion yuan. Furthermore, it was clarified that the target of the acquisition is strictly limited to commercial housing that has been built by a real estate company that has not been sold, and that the buyer is a local state-owned enterprise. At this point, we believe that the framework surrounding the acquisition of existing commercial housing has been initially established and clarified.

► Revitalize existing soil storage. For the first time, it was proposed to support local governments to take back land at reasonable prices, give full play to the role of a secondary land market, and promote circulation and transfer mechanisms. We believe that this policy is also an important puzzle to remove from inventory.

► Mortgage policy. The minimum down payment ratio limits for the first and second apartments were lowered to 15% and 25%, respectively (previously 20% and 30%, respectively), abolished the lower limits of the national personal housing loan interest rate policy, and each city independently determined the level within its jurisdiction based on the city's policies. In addition, interest rates on various types of housing provident fund loans with various terms will also be lowered by 0.25 percentage points. Overall, the adjustment of the mortgage policy may exceed market expectations.

The highlight of the policy? We believe that the overall strength of the current real estate policy is similar to that of 2015, and market expectations may usher in improvements. Similar to 2015 is the restrictive demand policy and the vigorous optimization of credit policies. In particular, we expect a further decline in mortgage interest rates to support residents' ability to buy homes. The part of differentiation is mainly the method of fiscal effort, from demand-side currency investment during the shed reform period to the current round to a supply-side mechanism with collection, storage, and inventory revitalization as new grippers. We believe that innovation is that it may provide housing enterprises with a more direct and powerful cash flow support mechanism. We believe that the establishment of this system can effectively strengthen the ability to prevent and mitigate financial risks in the real estate sector, and also consolidate the security of China's overall financial system. This is a critical background for our view of future market trends. As for the potential intensity of capital investment, we believe that, firstly, investment under the current framework is becoming more accurate and rational. Second, the necessity of investment may also change dynamically as the market environment improves, and we tend to observe the final investment intensity dynamically. Overall, this round revolves around the supply side, and a series of measures to remove inventory and optimize increments reflect policy planning and innovation capabilities, and may lead to a market repair path differentiated from previous cycles. We believe that differences may be reflected in several aspects. First, in the past, demand was mainly added, and in this round, supply was more oriented. These are two different balance methods. The latter supports asset prices more strongly or more moderately; second, the main body of leveraging is shifting to government departments, and the recovery of production capacity by enterprises during the deleveraging process is more gradual, so the driving capacity of development and investment activities to drive the economy may be weaker than before; third, this round takes more into account total restoration and structural reforms. For example, the housing supply structure and real estate business management model may experience new changes.

Where does the cycle run? We believe that the overall adjustment of housing prices will continue for some time in the context of higher inventories (especially second-hand housing inventories), but the downward slope has narrowed marginally (“How to understand current real estate price trends?” Through further examination of the rent-to-sale ratio of housing in China, we believe that there may be room for further adjustment of housing prices in China within this round (“How do you view the rent-sale ratio of housing in China?”). Overall, even without considering new policies, we believe that the real estate cycle itself in the next 6-12 month dimension is expected to take a turn and transition to a smoother phase. We believe that the recent introduction of new real estate policies may have a more profound impact on how the market operates in the next 3 years. We believe that the core of the New Deal is to optimize two aspects. One is that it is possible to relieve the pressure of inventory accumulation (especially second-hand housing inventory) by guiding improvements in market expectations to transition to a state of inventory removal; the second is the further management of potential financial risks for housing enterprises described above, which can provide a more stable environment for the market to operate. Overall, consideration of various aspects of the current real estate policy is gradually improving, and the pressure to adjust housing prices during this cycle has also been fully released. We have stronger confidence in the steady recovery of the market in the next 3 years, and the main gripper in judging housing price trends may also fall back to the economic situation itself.

What other policy areas are worth paying attention to in the future? We think there are four main aspects.

► Long-term supply structure adjustments. We believe that housing supply will show three basic trends in the next few years: one is a decrease in supply growth, the second is an improvement in supply quality, and the third is supply structure adjustment. Among them, supply structure adjustment includes the dual meaning of balance between rental and purchase, as well as balance between products and security, all of which may be achieved using guaranteed housing as the main carrier. Although the mention of the three major projects has recently been diluted, we do not recommend that the market view guaranteed housing as an expedient measure or as an exit channel for fiscal collection and savings. In fact, we think this is an important part of the next phase of China's real estate infrastructure reform, and it is also a reasonable strategy for supply-side adjustment in the post-cycle, so the new supply structure may be long-term.

► Deleveraging strategies of Chinese housing enterprises. For example, if we compare the general bailout process of financial institutions (although this analogy is not necessarily accurate), the current collection, savings and inventory revitalization mechanism is similar to the “lender of last resort” mechanism. We believe that it is effective for enterprises experiencing phased difficulties in terms of cash flow, but for companies that may actually already need to undergo asset restructuring, we think further plan research and refinement can be carried out. Overall, Chinese housing enterprises are still in the early stages of deleveraging, which mainly relies on cutting expenses and disposing of assets, and the progress and results of their deleveraging in the future deserve close attention.

► Optimization of the revitalization mechanism for the secondary market of land and assets. In addition to the personal housing market, local governments are already implementing a series of measures conducive to promoting the circulation of transactions, the revitalization of assets on the enterprise side may be the next priority. For example, during the State Council press conference on May 17, a spokesperson for the Ministry of Natural Resources mentioned that in the future, transaction mechanisms will be simplified and optimized for the recovery and acquisition of undeveloped land, or that will help the government and enterprises to revitalize existing assets between enterprises and enterprises. Another example is the public REITs market, which is also promoting further optimization of the normalized issuance mechanism, or optimizing processes in terms of asset review and asset recommendation. Overall, we believe that improving the efficiency of revitalizing the stock will help in risk management in the Chinese real estate market, and is also one of the important measures for deleveraging.

► Optimization of credit policies. The central bank's abolition of lower mortgage interest rates is expected to promote the formation of market-based interest rates in this field. We estimate that the average interest rate for the first home loan in March 2024 was about 3.59%, and there may still be marginal downside in the future. Furthermore, the current reduction in mortgage interest rates mainly revolves around newly approved loans, and it is worth paying attention to whether interest rates on stock loans will be adjusted simultaneously in the future.

A brief summary of future prospects: We believe that recent policy adjustments will lead to improvements in social expectations and the creation of a more favorable market operating environment. Looking ahead, we believe that the market adjustment may still have some inertia in the short term, but the slope may tend to converge, and it is expected that the adjustment phase since 2021 will end in the near future and enter the next relatively smooth operating cycle. In the next 3 years, we believe that the basic state of China's real estate industry will still be “inventory removal and deleveraging,” and that the industry's production capacity and development investment may gradually return to a potentially reasonable level (for discussions on reasonable demand, see “Looking at Potential Demand for New Urban Housing Under the New Situation in the Real Estate Industry”).

Investment prospects in the real estate sector

Overall, we believe that the strength or weakness of policy enforcement may not affect the fact that China's real estate stocks will usher in a round of valuation repair at a turning point in the cycle, but the recent centralized introduction of policies may present a certain degree of anticipation for confirmation and trading opportunities at the bottom of the stock price. Looking at the 6-12 month dimension, we think real estate stocks may still have room to rise from their current position. In the short term, if the stock price pulls back and consolidates, we think further investment arrangements can still be made.

Where are Chinese real estate stocks in the long term? We believe that China real estate stocks may have confirmed the bottom of the long cycle. In addition to observing traditional valuation indicators such as net market ratio (see Chart 3), we provide three more perspectives. First, the recent bottom price index is similar to 2008 and 2014. Second, we estimate that the compound annualized return of Chinese real estate stocks (mainly selecting large and medium-sized stocks still on the market) over the past 20 years was 9.4% (10.1% in US dollars), which is slightly higher than the annualized increase in housing prices during the period (about 8%). Our long-term estimates for overseas markets for nearly 40 years show that the average annual return on stock prices for real estate stocks in major markets is around 9%, while the annualized increase in nominal housing prices may be around 3%. This shows that real estate stocks that can cross the cycle can record returns similar (or slightly higher) to the equity market as a whole in the long term, and that this rate of return is higher than the increase in housing prices. Looking back at the relationship between China's real estate stocks and the rise in housing prices, it's hard to think that China's real estate stocks are substantially overvalued. Third, we estimate that Chinese real estate stocks account for about 1% of the market value of the A-share market, which has reached a record low, and is similar to the historical bottom level of overseas markets (see “Time changes, real estate investment should take a different face”). Overall, we believe that China's real estate stocks are expected to get out of the most difficult stage in history and open up a recovery channel.

What kind of market conditions are we likely to face, and how does it compare to 2015-2017? We currently believe that a potential shift in the 6-12 month real estate cycle is expected to bring about a round of valuation repair, but it is unlikely that it will evolve into a bull market similar to 2015-2017. Some of the bases for arriving at this point include:

► What are the main factors influencing real estate stock valuations? Our historical examination of domestic and foreign markets shows that the housing price cycle has the most direct explanation for net market rate fluctuations.

► Do Chinese real estate stocks have the conditions for a subsequent bull market? Simply put, the resonance of demand, housing prices, and leverage are the three necessary conditions for real estate stocks to rise to a high level. Typical examples include mainland China 2015-2017, the US 2003-2006 and 2021-2024, Hong Kong, China 1994-1997, etc. These periods also saw significant financial expansion. Looking at the comparison, we believe that in the next three years, China may still be in the consolidation stage in terms of demand for home purchases, housing prices, and the ability of enterprises to expand their tables. The upward space and resonance probability of the three elements are all relatively limited, so it is currently difficult to think that the conditions for a new three-year bull market are in place.

► Can you provide some references to the history of overseas markets? Overseas real estate stocks also showed a valuation repair market at a similar stage. Using some large and medium-sized enterprises as a statistical sample, we found that US real estate stocks achieved overall share price earnings of about 40% during the period from the first quarter of 2009 to the first quarter of 2010 (the inflection point of the first housing price cycle), while Japanese real estate stocks achieved an overall return of about 50% from mid-1995 to mid-1996 (housing prices can be confirmed to stabilize month-on-month in the second quarter of 1995). The overall profit of Hong Kong real estate stocks from the third quarter of 1998 to the second quarter of 1999 (the third quarter of 1998 was the inflection point of the first housing price cycle), achieved an overall return of more than 1 times. These markets usually run for no more than 1 year from bottom to top, so they can be thought of as a phased upward trend. The main driving factor is the restoration of valuation multiples, and the restoration of industry fundamentals after the incident actually took longer.

Short-term strategy? The recent recovery in real estate stocks is based on expected improvements, and we do not rule out that there will still be some upward momentum in the short term. However, as the cumulative increase expands, the market may experience pullback pressure, and then enter a period of observation of the effects of the policy. However, leaving aside short-term game-like and eventful transactions, we believe that the real estate market itself is already running in a direction where the downward slope is slowing down. The introduction of policies may help the current cycle to take a faster turn in the 6-12 month dimension to end the first adjustment phase since 2021 and transition to the next smoother cycle. At this turning point in the cycle, we believe that the sector is expected to experience a significant round of revaluation. There is some progress in recent trading, but the increase in the past three weeks (about 37% cumulative for A-shares and 46% for Hong Kong stocks) has not yet been overdrawn to the potential height of this round. If there is a subsequent correction and consolidation in stock prices, we recommend further layout.

The investment tone for the next 3 years? As mentioned earlier, a sustained market based on significant total recovery is not what we currently think is the benchmark situation, and the cycle trend thereafter still needs to be assessed dynamically. The current round of real estate stock recovery may represent the beginning of a longer dimensional investment cycle, but we believe that investment within this stage may need to balance total volume and structure. For example, we believe that the fundamentals of asset-light companies may have bottomed out and are on the recovery path; the long-term investment base of asset-heavy enterprises may still need to be consolidated, but there may also be some changes and iterations in business models within the enterprise, and the ability to expand the table over a long period of time will also be more clearly differentiated. Finally, the public REITs, an emerging market, may enter a new 3-year expansion cycle, and their investment value is also worthy of industry attention.

Chart 1: Highlights of the May 17 State Council Policy Routine Briefing Meeting

Chart 2: Fundamental Trends and Policy Adjustments in Past Cycles

Chart 3: Historical trend of China's sample A-share real estate stocks

Chart 4: Historical trend of US domestic production stocks

Chart 5: Historical trends in Japan-like domestic production stocks

Chart 6: Historical trends in Hong Kong, China's local production stocks

Chart 7: Long-term returns on real estate stocks in major global markets

Chart 8: Forward price-earnings ratio and net price-earnings ratio of A-share real estate companies

Chart 9: Forward price-earnings ratio and net price-earnings ratio of H-share real estate companies

Editor/jayden