① Analysts expect Nvidia's net profit for the 2025 fiscal year of Q1 to be US$12.87 billion, an increase of more than 530% over the previous year. ② In addition to the performance figures themselves, demand prospects and supply chain issues are still the focus of attention. ③ Well-known investors recently revealed that they had reduced their Nvidia stock holdings at the end of March; Goldman Sachs recently raised Nvidia's target price.

“Science and Technology Innovation Board Daily”, May 18 — Nvidia will disclose the results for the first quarter of fiscal year 2025 (as of April 28, 2024) after the US stock market closes on May 22, and will hold a conference call at 14:00 Pacific Time on May 22 (5:00 Beijing time on May 23).

According to consensus forecasts compiled by Visible Alpha, analysts expect Nvidia's revenue for the first quarter of fiscal year 2025 to reach 24.65 billion US dollars, an increase of 11.54% over the previous year, an increase of more than double the previous year. Previously, the company's revenue guidance was 24 billion US dollars, fluctuating 2% up and down; net profit for the same period is expected to be 12.87 billion US dollars, a slight increase from month to month, an increase of more than 530% year on year.

In the midst of this AI boom that has continued for a long time, demand for AI chips continues to soar, and Nvidia's data center business has also grown rapidly. In the fourth quarter of fiscal year 2024, its data center business revenue reached US$18.4 billion, more than five times the same period of the previous year, and set a new record high set in the previous quarter. At the time, Nvidia estimated that about 40% of this $18.4 billion came from AI inference.

As earnings for the first quarter are about to be revealed, Nvidia's data center business revenue may reach a new high — according to estimates compiled by Visible Alpha, its data center division's revenue for the first quarter of fiscal year 2025 may reach US$21.17 billion, an increase of 15% over the previous quarter.

▌What issues need attention?

As the “king” of the AI chip field at this stage, every trend of Nvidia still affects the nerves of the market.

As the giant's new earnings report is about to be revealed, in addition to the performance figures themselves, demand prospects and supply chain issues are still the focus of investors' attention. Morningstar believes there are a few more issues worth paying attention to:

The first is the data center business. Focus on whether (or how fast) Nvidia's suppliers can expand to meet their AI GPU needs;

Second is customer demand. What is the pace of data center capital expenditure in 2024 and beyond? Indeed, cloud service providers will still invest heavily in AI, and “most of the spending is expected to go into Nvidia's pocket.” But beyond that, what about capital expenses for software vendors, financial services companies, healthcare companies, etc.?

Then there are GPU market expectations. AMD previously raised its forecast for the industry's overall potential market in 2027 from 150 billion US dollars to 400 billion US dollars. This figure includes not only GPUs, but also various other types of chips.

Finally, how does Nvidia view those tech giants starting to develop their own chips, and how can the company deal with this competition? When will the recent supply restrictions be resolved?

▌Can Nvidia continue to rise?

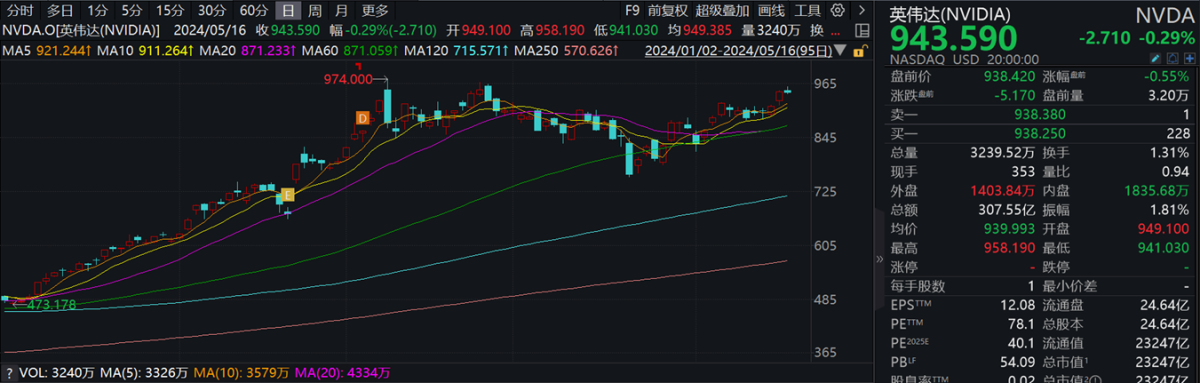

Judging from the stock price trend, since this year, Nvidia's range increase has reached about 90%, and set a new record high in stock price in March of this year, reaching 974 US dollars — this impressive increase is still a result achieved against the backdrop of a cumulative increase of nearly 240% last year.

Chart | Nvidia's US stock trend from January 2 to May 16 local time

As Nvidia's stock price and market capitalization soared, it was a question on the minds of many investors: “Is Nvidia too expensive? Can it still go up?”

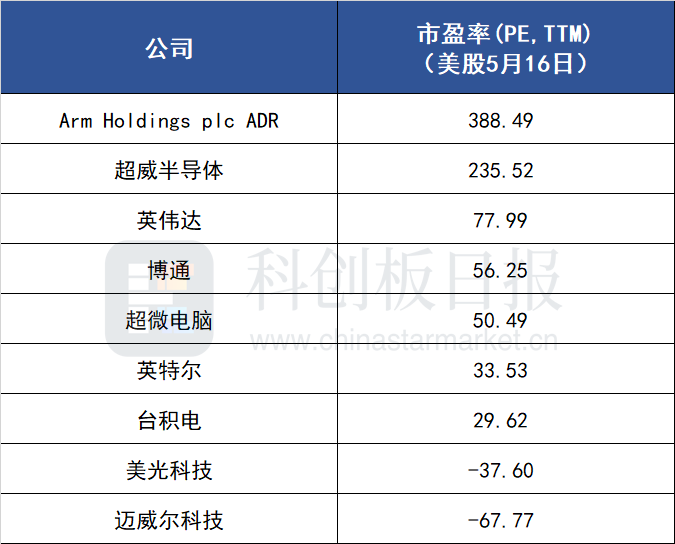

Judging from the price-earnings ratio, among popular AI concept stocks in the US, Nvidia's price-earnings ratio (TTM) is currently around 78 times; while AMD and Arm have reached 236 times and 388 times, respectively.

Goldman Sachs said in a report released last week that Nvidia shares still have a lot of room to rise in the future and raised Nvidia's target share price from $1,000 to $1,100. Goldman Sachs said that considering Nvidia's rapid growth rate and the persistence of this growth trend in the next few years, its stock valuation is still relatively attractive compared to its peers.

According to the report, AI remains Nvidia's main growth driver, and it is expected that data center performance in the second and third quarters of this year will benefit from strong demand for artificial intelligence-related computing and networks. Furthermore, Microsoft, Google, Amazon AWS, and META's capital investment in cloud computing continued to grow this year, and analysts believe this will also drive Nvidia's continued revenue and profit growth.

However, there were also those who raised cautious opinions.

Well-known Wall Street investor Stanley Druckenmiller revealed in an interview with the media in early May that he had reduced his Nvidia stock holdings at the end of March this year. Druckenmiller said that although 20 years ago no one would have thought the internet would become so huge, the NASDAQ index still fell 80% in 1999. At the same time, he stressed that artificial intelligence may be a bit overhyped now, but it is still underrated in the long run.

Looking back at the last time Nvidia released results (fourth quarter of fiscal year 2024), the “perfect” financial report sparked market enthusiasm — Wall Street firms raised Nvidia's target price one after another; Nvidia's market capitalization soared $277 billion in just one day.

So this time, this stock, hailed by Goldman Sachs as “the most important on Earth,” will it hand over what results, and can it still regain its former glory? Let's wait and see.