Some EMCORE Corporation (NASDAQ:EMKR) Analysts Just Made A Major Cut To Next Year's Estimates

Some EMCORE Corporation (NASDAQ:EMKR) Analysts Just Made A Major Cut To Next Year's Estimates

The analysts covering EMCORE Corporation (NASDAQ:EMKR) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

报道EMCORE Corporation(纳斯达克股票代码:EMKR)的分析师今天对今年的法定预测进行了重大修订,从而给股东带来了一定负面影响。收入和每股收益(EPS)的预测均向下修正,分析师认为灰云即将出现。

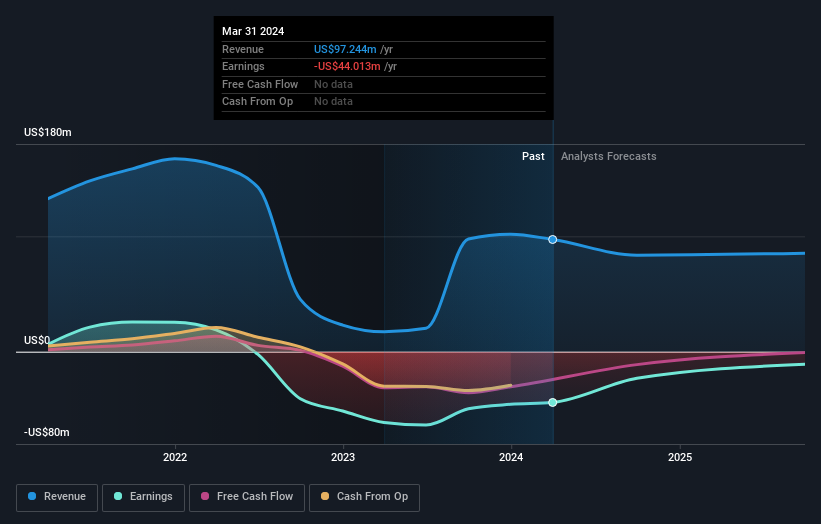

Following the latest downgrade, the current consensus, from the three analysts covering EMCORE, is for revenues of US$84m in 2024, which would reflect a chunky 14% reduction in EMCORE's sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 68% to US$1.84. Yet before this consensus update, the analysts had been forecasting revenues of US$102m and losses of US$1.65 per share in 2024. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

继最近的降级之后,报道EMCORE的三位分析师目前的共识是,2024年的收入为8400万美元,这将反映出EMCORE在过去12个月中销售额大幅下降14%。预计每股亏损将在不久的将来大幅减少,缩小68%至1.84美元。然而,在这次共识更新之前,分析师一直预测2024年的收入为1.02亿美元,每股亏损1.65美元。因此,在最近的共识更新之后,观点发生了很大变化,分析师大幅下调了收入预期,同时也预计每股亏损将增加。

The consensus price target fell 83% to US$2.00, implicitly signalling that lower earnings per share are a leading indicator for EMCORE's valuation.

共识目标股价下跌83%,至2.00美元,暗示每股收益下降是EMCORE估值的主要指标。

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. Over the past five years, revenues have declined around 5.9% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 26% decline in revenue until the end of 2024. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 5.2% per year. So while a broad number of companies are forecast to grow, unfortunately EMCORE is expected to see its sales affected worse than other companies in the industry.

我们可以从大局的角度看待这些估计值的另一种方式,例如预测如何与过去的表现相提并论,以及预测相对于业内其他公司是否或多或少看涨。在过去的五年中,收入每年下降约5.9%。更糟糕的是,预测本质上是预测下降将加速,预计到2024年底,收入的年化下降26%。相比之下,我们的数据表明,预计类似行业的其他公司(有分析师报道)的收入每年将增长5.2%。因此,尽管预计将有许多公司增长,但不幸的是,预计EMCORE的销售影响将比业内其他公司更严重。

The Bottom Line

底线

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at EMCORE. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that EMCORE's revenues are expected to grow slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

从此次降级中需要注意的最重要一点是,市场共识增加了今年的预期亏损,这表明EMCORE可能并非一切顺利。不幸的是,分析师也下调了收入预期,行业数据表明,预计EMCORE的收入增长将慢于整个市场。考虑到下调评级的范围,看到市场对该业务变得更加警惕也就不足为奇了。

That said, the analysts might have good reason to be negative on EMCORE, given dilutive stock issuance over the past year. For more information, you can click here to discover this and the 4 other concerns we've identified.

尽管如此,鉴于过去一年的股票发行量呈稀释态度,分析师可能有充分的理由对EMCORE持负面看法。欲了解更多信息,您可以点击此处了解这个问题以及我们已经确定的其他 4 个问题。

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

当然,看到公司管理层将大量资金投资于股票与了解分析师是否在下调预期一样有用。因此,您可能还希望搜索这份内部人士正在购买的免费股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。