Zheshang Securities recently released a research report, which believes that the combination of the three major factors of the protracted Red Sea conflict, marginal improvement in demand from Europe and the US, and the entry of the US line into the Changshang Agreement signing period is the reason for the recent sharp rise in shipping prices.

Recently, there has been a counterintuitive rise in freight rates. Following a sudden increase of 12% in the intraday session last Thursday, all European contracts have broken out again recently. Yesterday, the intraday price surged by more than 14.64% to a high of 4034.3, setting a new record high. By the close, the increase was still as high as 12.11%. Zheshang Securities recently released a research report. It believes that the prolonged Red Sea conflict, marginal improvement in demand from Europe and the US, and the entry of the US line into the Changshang Agreement signing period are the three major factors that have led to the sharp rise in shipping prices.

The increase in freight rates exceeded expectations

Recently, freight rates have risen more than expected. On May 9, shipowners announced the June freight rate increase one after another. Dafei announced the online FAK rate between Shanghai and Ouji Port in early June. The price for large containers was 6,000 US dollars, and the Maersk large cabinet price was raised to 5,500 US dollars.

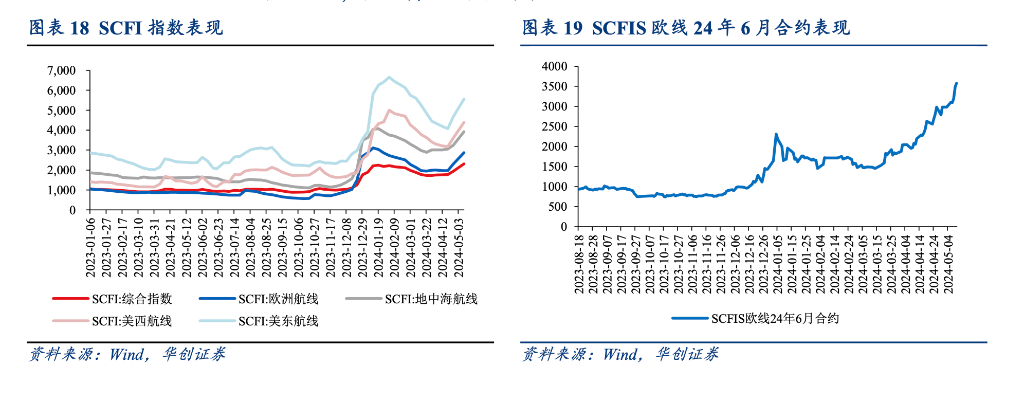

SCFI's recent strong performance. As of May 10, SCFI closed at 2306 points, +18.8% week over week; among them, the US West, East America, Europe, and the Mediterranean were +22.0%, +19.3%, +24.7%, and +21.0%; SCFI 2024Q2 averaged 1904 points, +93.6% year over year.

Currently, the SCFI European route freight rate is about November 2020, while the average value of SCFI's European route from 2017 to 2019 is only 820 US dollars/TEU. Currently, it has risen 249.9% year on year from this average level; the SCFI US East Asia route has risen to the level of 11/20, which is 111.8% higher than SCFI's average value of 2,626 US dollars/TEU from 2017 to 2019.

Recently, on May 10, the SCFIS (Shanghai Export Container Settlement Freight Index) European line contract in June '24 EC2406 was +20% month-on-month, up about +297.3% from December 1.

Prolonged Red Sea conflict has strained supply chains

According to the Zheshang Securities Research Report, there is an intrinsic logic behind the recent sharp rise in shipping prices. The prolonged Red Sea conflict, marginal improvement in demand between Europe and the US, and the entry of the US line into the CCA signing period are the three major factors that have led to the counterintuitive rise in freight prices.

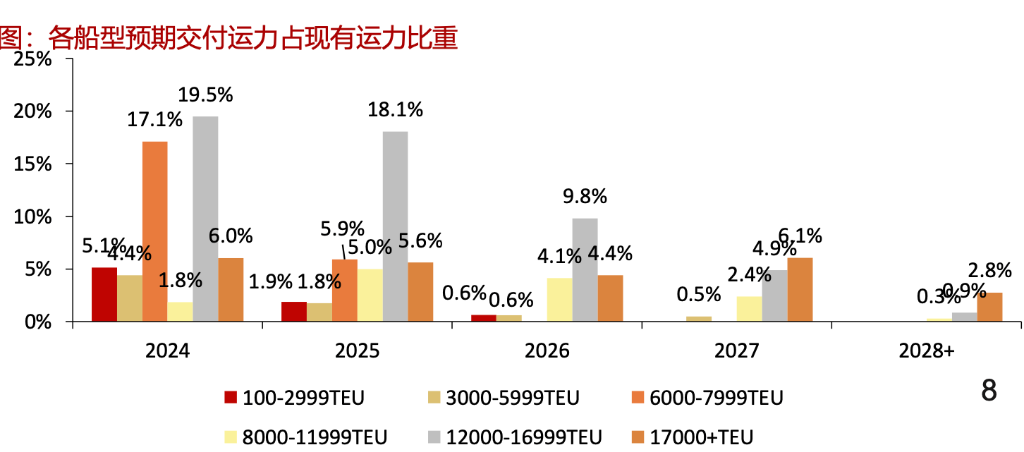

From the supply side, container ships have entered the centralized delivery period. As of April 2024, the world has about 6,239 container ships in stock, with a total capacity of about 285.49 million TEU, and about 749 ships on hand. The total capacity is about 6.347 million TEU, accounting for about 22% of the order capacity.

According to Clarksons data, delivery capacity from 2024 to 2027 is expected to account for 8.3%, 6.8%, 3.9%, and 2.6% of the current capacity, respectively. 2024-2025 is the centralized delivery period for order capacity. By ship type, the 17000+ TEU ship on the main route will account for about 6.0% of the delivery capacity in 2024, and delivery capacity is relatively limited.

The research report points out that ships detour after the Red Sea conflict, and there is a marked trend of protracted detours. Since January, container ships have begun to bypass the Cape of Good Hope on a large scale. As of May 8, an average of about 6 container ships arrived in the Gulf of Aden on the 7th, -67%, and the number of containers was 16,700 TEU, or -92%; about 20 container ships arrived at Cape of Good Hope, +262% compared to the same period, and the number of containers was 224,300 TEU, +446% year over year.

According to Clarksons data, if you avoid the Red Sea and choose a detour, the route distance and number of sailing days will be greatly increased. Take the Far East to Europe as an example. The number of days to sail around the Cape of Good Hope is about 36 days, which is an increase of about 8 days compared to the route through the Suez Canal, and the flight distance will increase by about 29%. According to research estimates, detours on routes from the Far East to Europe will drive a 5.27% increase in global demand for box-nautical mile transportation.

According to the research report, the Red Sea conflict has effectively increased the demand for container ships' capacity in nautical miles and absorbed the existing capacity. According to Clarksons data, capacity is expected to increase by about 9.0% in 2024, demand tons and nautical miles will increase by about 9.2%, and the relationship between supply and demand in the industry will improve. However, due to the relatively limited delivery capacity of the 17,000+ TEU ship type on the main route mentioned earlier in 2024, it is expected that the trade box nautical mile growth rate between Europe and the Far East will be 16% in 2024, and the supply of European capacity is relatively scarce.

As a result, the Red Sea crisis has, on the one hand, led to an increase in ship detour distances, effectively increasing the demand for box-nautical-mile capacity and absorbing existing capacity; on the other hand, the decline in ship turnover efficiency has led to tight container turnover in ports, further exacerbating supply chain tension.

High concentration and industry alliances form a driving force to raise prices

At the same time, the research report believes that the highly concentrated pattern of the shipping industry and industry alliances have formed a driving force for price promotion.

Foreign trade container liner companies have a high level of concentration. As of May 10, 2024, the top ten container liner companies accounted for 84.2% of capacity. Coupled with the formation of industry alliances and cooperation between companies, on the one hand, it helps to slow down vicious price competition by suspending flights and controlling capacity in the context of the deteriorating supply and demand environment. On the other hand, in the context of improving supply and demand relationships, it is expected that higher freight rates can be achieved through joint pricing.

Shipping prices rose sharply in 2024. Year-to-date, the CCFI index averaged +20% year-on-year, and the SCFI index averaged +100% year-on-year.

Since May, a number of shipping companies have disclosed price increases. At the beginning of the month, Dafei and Hapag-Lloyd targeted freight transfers on routes such as Asia - Northern Europe, Asia - Mediterranean and North Africa. Taking DaFei as an example, the new FAK standards for the Asian-Nordic route are 2,700 US dollars/TEU and 5,000 US dollars/FEU. The new standard increases were 500 US dollars/TEU and 1,000 US dollars/FEU; recently, a number of liner companies have successively adjusted peak season surcharges for Asian-African routes.

Demand margins are improving

According to the research report, a positive demand-side margin has also contributed to price increases. On the one hand, macroeconomic data in Europe and the US improved marginally; on the other hand, due to longer transit times due to detours, compounded expectations of rising freight rates during the peak season, shippers prepared goods ahead of schedule.

Finally, the US line has entered a critical period of signing the Changxie contract, and shipping companies are motivated to increase prices.

Editor/Somer