Lottery becomes a high-yield stock

The outbreak of European shipping at the end of last year ushered in a second wave of climax.

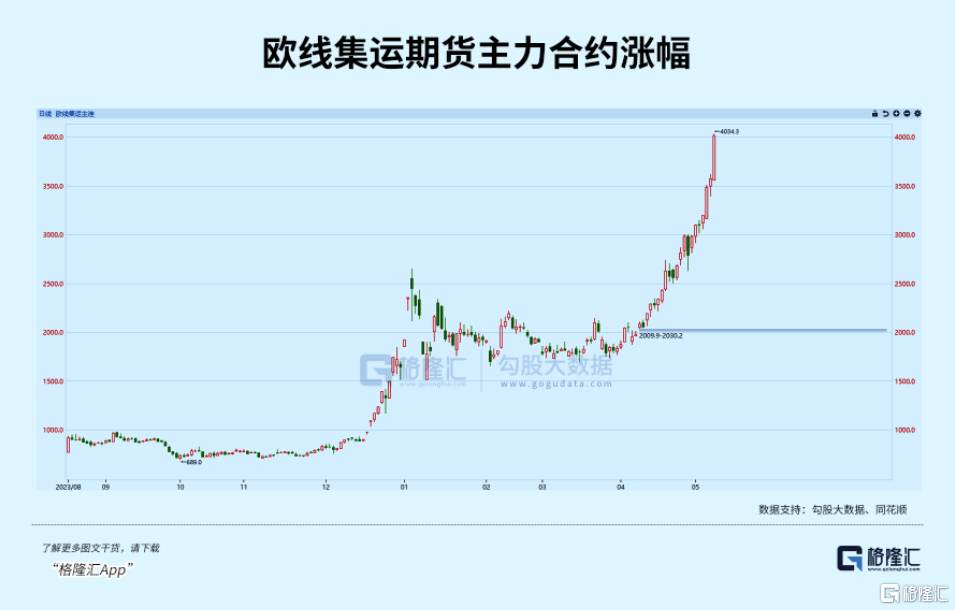

Following the sudden rise of 12% in the intraday period last Thursday, all European contracts have recently broken out again. At one point, the intraday surge surged by more than 14.64%, reaching a high of 4034.3, setting a new record high. By the close, the increase was still as high as 12.11%.

This sharp rise began in late December last year. After four months of silence, the price of the main contract soared from the lowest point of 904.6 to 4008.9 at the close of today's session, with a cumulative increase of 352.47%.

In addition to the intensification of geographical risks in some regions, the recovery in international trade demand this year has also boosted the shipping boom. COSCO Maritime Control surged by more than 9%. This is because the shipping cycle was adjusted starting in 2022, and Maritime Control once again returned to a market value of 200 billion dollars.

Is the “King of Cycles” taking advantage of this time to return?

01

This second wave of European line surges was mainly driven by three factors.

The heating up of the geographical situation is the main reason why the main European futures contracts of the Transportation Index continue to rise. The failure of the peace talks between Palestine and Israel in Cairo temporarily dashed hopes of calming the Red Sea situation, and the disruption caused by the Red Sea turmoil to the container transport industry is spreading.

Recently, Danish shipping giant Maersk said at a performance conference that it is expected to cut capacity between Asia and Europe by up to 20% in the second quarter of this year. Furthermore, the route around the Cape of Good Hope increased fuel usage by 40% per voyage, increasing the operating costs of sailing.

Second, spot prices have been rising, and major liner companies are successively preparing for the second round of rate increases in May.

The first round of freight rates for early May was generally positioned at the level of 4,000 US dollars/FEU (40 foot container unit), up from the price center of 3,000 US dollars/FEU in late April at the level of 1,000 US dollars/FEU. Afterwards, the freight rate price starting in mid-May rose further to the first line level of 5,000 US dollars/FEU.

Moreover, as demand for international trade gradually recovers, current shipping expectations are good, and European line pressure will increase as soon as the peak season begins.

The Eurozone ZEW Economic Sentiment Index for April, which was previously announced, recorded 43.9, a record high of nearly 26 months. Looking at exporting countries, China's manufacturing industry has clearly recovered. The March-April manufacturing PMI and new export order PMI sub-data were above the boom and bust line for two consecutive months.

Since the beginning of the year, export volumes have been strong, along with a recovery in overseas inventory demand. 1Q24's container traffic increased 10.5% year on year. Among them, cargo volume on US lines/European routes/Asian routes showed a year-on-year performance of +9.7%/-9.2%/+14.4%. Since March of this year, the weekly container throughput of Chinese ports has been the highest in nearly 3 years.

So how long has the price increase continued since then?

Currently, the airline plans to gradually start increasing the freight rate in early June. On May 9, Maersk initially priced the price at 5,500 US dollars/FEU, while Dafei set the price at the level of 6,000 US dollars in early June.

Looking back, there is currently no significant marginal increase on the supply side. The detour has caused ships returning to the Far East from Europe to not be in a timely manner and continue to affect supply. If the volume of goods is sufficient during the next peak season, there may also be two or more rounds of mid-month price increases in June-August, and the freight center may rise further.

02

Affected by the drop in container freight rates, the 23-year performance of Maritime Control unexpectedly declined. The annual report for the year 23 was announced at the end of March. Revenue fell 55.14% year on year, and net profit to mother fell 78.25% year on year.

The 23-year supply chain bottleneck has just been eased, yet ships built during the super dividend period are being launched at an accelerated pace. Last year, global container capacity increased by about 8% year on year, double the growth rate in 2022.

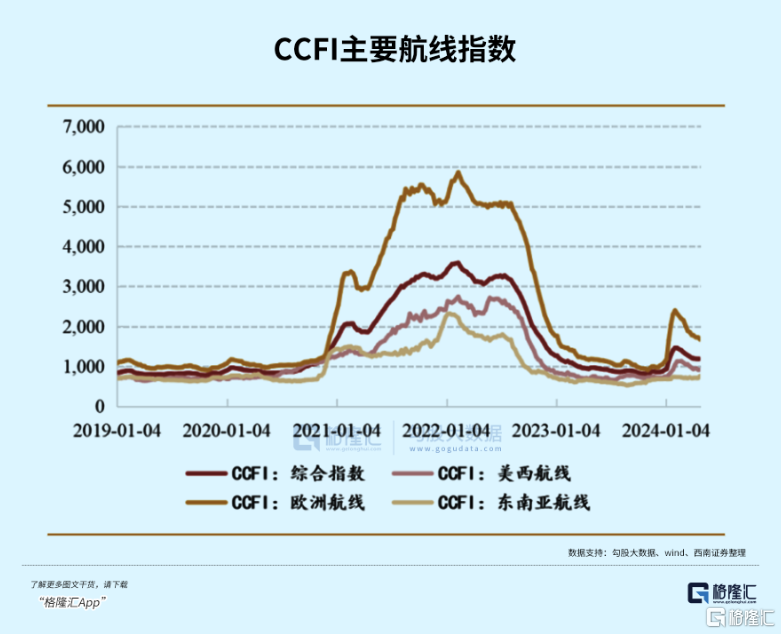

Meanwhile, most developed countries in Europe and the US, which struggle with inflation and have to raise interest rates, have fallen into a situation where demand is falling. The average value of China's Export Container Freight Composite Index (CCFI) fell 66.4% year on year in 2023. Due to the sharp imbalance between supply and demand, COSCO Maritime Control's container shipping business revenue fell 56.22% year on year.

In terms of volume price, the company's consolidated cargo volume was 235.54 million TEU, down 3.5% year on year, of which the cargo volume of foreign trade routes was 19.2.31 million TEU, down 3.5% year on year; estimates suggest that the company's revenue per box of foreign trade routes was 10,55.3 US dollars/TEU, down 60% year on year, basically in sync with export freight rates.

Industry profits also shrunk sharply in 2023. Of the top ten liner companies in the world last year, although 8 companies achieved profits, the average net profit drop was as high as 87.5%, and the remaining 2 lost money. In particular, in the last quarter, the first two giants, Maersk and Dafei Group, both experienced losses and began massive layoffs in order to cut costs.

The industry still faced excessive pressure in 24-25 years. According to Clarkson data, as of March 2024, on-hand orders for container ships were 23% of the current fleet. Even with environmental regulations and the elimination of old ships, the 2024-2025 fleet growth was 8.9% and 4.9%, respectively, while cargo demand increased by only 3.9% and 3.0%, respectively, during the same period.

Trade demand has recovered, but it cannot beat the speed of supply release, so outsiders predict that freight rates will fall easily and will not rise.

Outsiders originally anticipated that the container shipping market would fall into a long-term downturn. However, the Red Sea crisis caused another change in market supply and demand. It is unknown how long this sudden black swan will last and when it will end.

Since December of last year, Maersk and other shipping companies have diverted cargo ships to the Cape of Good Hope in Africa to avoid being attacked by Iranian-backed Houthi militants in the Red Sea. The detour led to a longer flight time, which not only boosted immediate freight rates, but also absorbed more existing capacity in order to ensure timely delivery.

However, the annual supply volume of the shipping industry is actually the load capacity of all ships multiplied by the speed of navigation times the annual effective time, and then summed. The situation in the Red Sea continues to ferment, so whether the diversion operation will cause congestion at ports in other regions will continue to affect supply. It is difficult to clearly assess, so there is a big difference in expectations whether the freight rate adjustment will be sustainable.

The results of several giants in the first quarter of this year showed that although the profit portion still declined sharply, as the Red Sea problem continued to affect freight rates, the decline was better than market expectations. In the first quarter, global container ship capacity increased 9.6% year on year. Among them, European line capacity increased 8.6% year on year, and US line capacity increased 2.4% year on year. In the face of a significant increase in new supply, freight rates still recorded a significant year-on-year increase.

Market performance is as intense as a roller coaster. It mainly catalyzes marginal changes in the Red Sea situation. Looking at the actual growth in trade volume in the medium to long term, and the rate of release of global capacity, it is often easy to underestimate the ability of liner companies themselves to raise prices.

The shipping industry went through three full rounds of clean-up in the first 15 years. Leading companies launched price wars with the advantage of unit transportation costs brought by large ships. Other leading companies increased capital expenditure one after another, leading to a serious imbalance between supply and demand. In the middle, it even led to the merger and restructuring of “five weddings and one funeral”, forming three major shipping alliances, and the overall concentration level increased by one level.

The two rounds of promotion by the three major alliances in May raised the freight center significantly from the March off-season level, which in turn boosted the performance of shipping stocks. In a situation where demand has declined in the past, the three major alliances have tacitly saved freight rates by adjusting capacity investment, but the essence is still a match between supply and demand.

Maritime Control is no exception. Shipping prices from the Far East to the US and Canada rose sharply in April, up to 70% in terms of average freight rates. Maritime Control's revenue in the first quarter (1.9%) stopped declining, and net profit also rebounded sharply from month to month (277.6%).

In addition to the price factor, the overall cost control capability of Ocean Control is also improving. The cost of a single box fell 8.9% year-on-year in the first quarter, and the gross profit of a single box was +312.1% month-on-month. Furthermore, the size of interest-bearing debt continued to decline, and the financial expense ratio fell 2.1% year on year in '23.

Price competition has arisen due to capacity investment. Compared to Maersk, which has recently lost money, the company is still able to achieve relatively stable profits. This is mainly due to 1) Changxie's execution volume is lower than that of Maersk, which also benefits from the increase in immediate freight rates; 2) due to differences in route structure, Maersk's cost of a single box is more affected by the Red Sea situation. The external leasing ratio (42.7%) is higher than that of Haikou Control (25.35%), and the average rental cost has been rising for 4 consecutive months.

Shipping has strong cyclical properties and is closely related to the prosperity of the global manufacturing industry. Most inflection points in shipping demand occur in passive inventory removal. As global macro demand improved marginally, the Red Sea incident was an opportunity for price increases, which is conducive to the reversal of giants' performance expectations.

03

The sector's performance was poor last year, but undervaluation has fully overdrawn the industry's performance. Future improvement trends will become the core logic driving the sector's continued rise. Nothing has received more attention than COSCO Marine Control.

At the end of the 2023 period, Haikong plans to distribute a dividend of 0.23 yuan per share, with a total year-end dividend of 3,670 billion yuan. In addition to an interim dividend of 8.196 billion yuan, the company will total 11.866 billion yuan in 2023, accounting for about 50% of the company's net profit returned to mother in 2023. Meanwhile, in August of last year, the company began repurchasing A+H shares. By the end of February 2024, a total of about 215 million A shares and H shares had been repurchased.

Previously, freight rates dropped significantly, but maritime control operations did not fall into a quagmire. Profits seemed to have declined sharply in '23, but after the special year 21-22, last year was already the best performance since listing. The consistent forecast for net profit to the mother for 24 years reached 24 billion yuan, with 8-10 times PE. The dividend rate range is about 5% to 6.25%. The company's current market value is also within this range.

This is the third year in a row that the company has paid dividends. After an explosion of household income in the previous few years, there are about 140 billion dollars in undistributed profits and about 170 billion in cash assets on the balance sheet.

Previously, in order to ease public anger over scarce dividends, the company raised the dividend payment ratio to 30%-50% in 22-24, with an average of 42.22% in '22 and '23, which means this year is the last year, and how the return plan for the next three years will be adjusted. This will also reflect the company's attitude towards future profit prospects.

Compared to China's Shenhua, which is more than 800 billion dollars, the average ROE and dividend level have gradually increased after supply-side reforms. The average payment rate of the company in the three years 2020-2022 reached 88.44%, the highest or even higher than that year's net profit. The average dividend rate reached 10.19%. Although net profit is also declining, the dividend amount has not been greatly affected.

Of course, as a stock with some growth potential in the cycle, in response to calls from central enterprises to increase the dividend ratio, Haikong's future dividend rate and ROE have room to rise, and the valuation logic changes from strong cyclical stocks to high-interest stocks with low volatility and stable dividends, and whether more valuation premiums can be put in place one step at a time. A steady increase in profits is the most important prerequisite.

edit/new