Source: Kevin Strategy Research

summary

The differences in the Hong Kong stock market began to widen last week, and the strong upward momentum of the previous two weeks cooled down as scheduled at the beginning of last week. However, news on Friday about the possible adjustment of the Hong Kong Stock Connect dividend tax attracted widespread attention, and investors' risk appetite for the Hong Kong stock market, especially related high-dividend sectors, increased markedly. We are not surprised that the market has taken a break from this position and even pulled back. In the first two weeks, we repeatedly reminded investors that transactional capital and local and regional capital rebalanced due to fluctuations in peripheral markets may be the main driving force. After short-term overpurchases, the market will inevitably face pressure to return profits.

After the recent rapid rebound, the market has basically reached the target point of the first phase of our benchmark situation, which corresponds to around 19,000 points for the Hang Seng Index. The corresponding inflow volume under the EPFR caliber is about 5 billion US dollars, which is equivalent to about 1/4 of the total outflow of the Hong Kong stock market of nearly 20 billion US dollars since 2023.

If the risk premium falls back to the level at the beginning of last year, it is about 20,000 points for the Hang Seng Index; under optimistic circumstances, if follow-up policies continue to work to increase profits by 10%, the market is expected to open up further space, corresponding to 22,000 points for the Hang Seng Index. At this time, long-term value foreign investment is also expected to shift from the current low allocation to China, corresponding to capital inflows of about 42 billion US dollars, which is equivalent to the total outflow since 2021. But the fulfillment of this situation requires larger, faster, and more responsive fiscal spending as a prerequisite.

Admittedly, there are some recent positive changes at the policy level, such as statements from the Real Estate and Politburo meetings to speed up the issuance of ultra-long-term treasury bonds, but the speed and progress of subsequent progress may be even more important. However, recent data is still weak, indicating that further policy support is still necessary. In summary, the market has climbed to our target in the first phase. Until more symptomatic policy measures are implemented, we believe that the overall market may show a volatile trend, so compared to index performance, structural opportunities are more worthy of attention. Overall, it is reflected in a “dumbbell” configuration consisting of three main lines: dividends, technological growth, midstream overseas travel, and service consumption.

body

Market trend review

The differences in the Hong Kong stock market began to widen last week, and the strong upward momentum of the previous two weeks cooled down as scheduled at the beginning of last week. However, news on Friday about the possible adjustment of the Hong Kong Stock Connect dividend tax attracted widespread attention, and investors' risk appetite for the Hong Kong stock market, especially related high-dividend sectors, increased markedly. At the same time, the seesaw effect of dividends and technological growth reappeared. As the high-dividend sector strengthened again, the growth sector pulled back accordingly.

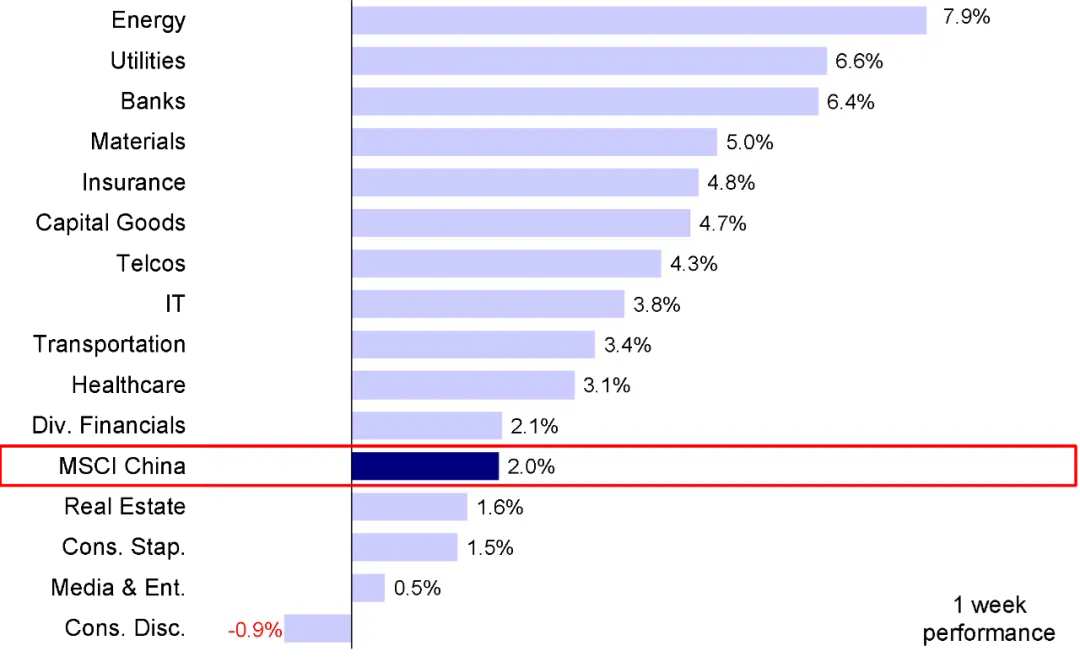

Overall, among the main indices, the Hang Seng and Hang Seng State-owned Enterprises Index rose 2.6%, the MSCI China Index rose 2.0%, and the Hang Seng Technology Index fell slightly by 0.2%. At the sector level, the energy, utilities and banking sectors outperformed, rising 7.9%, 6.6%, and 6.4% respectively, while the optional consumer sector lagged behind, falling 0.9% last week.

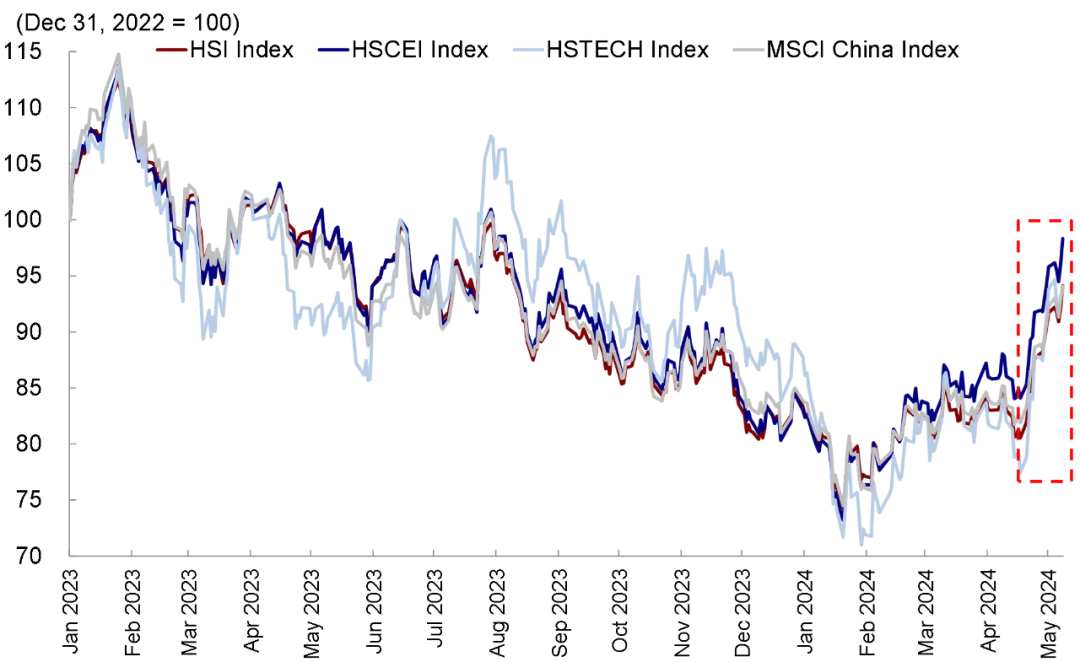

Chart: Following the rise in the previous two weeks, the market fluctuated last week, and the Hang Seng Technology Index even fell slightly

Chart: The traditional high-dividend sector outperforms, while the optional consumer sector lags behind

Market outlook

After the strong and rapid rebound of Hong Kong stocks in the first two weeks outperformed almost all global markets, the upward movement began to slow down at the beginning of last week, and market differences increased. There were some signs of a profit settlement in the first half of the week, especially in the technology growth sector, which had a large increase in the previous period. Had it not been for the sharp rise in the value sector due to dividend tax adjustments on Friday, the increase in the Hong Kong stock market this week may have narrowed markedly.

However, we are not surprised that the market took a break from this position and even pulled back. Our report in the previous two weeks has repeatedly reminded investors that the market has shown clear signs of being overbought in the short term, showing that RSI rose to the highest level since the beginning of 2023 last week, and the share of short sales also dropped sharply by 6% and fell below 15% within two weeks, returning to a low of early January this year).

Judging from historical experience, after being clearly overbought in the short term, the market usually fluctuates or even recovers. According to our previous analysis, the main driving force for this round of growth is capital, macroeconomic fundamentals, corporate profits, and policy changes are not significant (at least not enough to drive a rapid rise in the market within two weeks alone), so liquidity and capital aspects should be the main driving forces for this round of rapid growth.

Specifically, funding sources, transactional capital, and rebalanced local and regional capital due to fluctuations in peripheral markets such as the Japanese stock market may be the main driving force, while the return of long-term capital needs to be supported by more clear and strong fundamentals. Therefore, this source of capital and the rebound driving characteristics behind it can also explain why the market often faces some pressure to take back profits after signs of being overbought in the short term.

Chart: The Hang Seng Index's relative strength index declined somewhat after reaching extreme levels in recent years

Chart: The share of short sales transactions in the Hong Kong market fell rapidly within two weeks, and the decline was close to 6%

After the recent rapid rebound, the market has basically reached our target point in the first phase, which corresponds to around 19,000 points for the Hang Seng Index. How much room is there for foreign capital inflows and market follow-up? We calculate:

1) Under the benchmark situation, assuming that all of the funds from the regional rebalancing mentioned above have returned, it basically corresponds to the outflow of capital from the first quarter of this year (that is, the stage where the market is most enthusiastic about investing in overseas markets such as Japan). Under the EPFR scale, the corresponding inflow volume is about 5 billion US dollars, which is equivalent to about 1/4 of the total outflow of the Hong Kong stock market of nearly 20 billion US dollars since 2023.

Looking at market space, the rebound in the market since this year has basically been entirely contributed by valuation, especially the risk premium. The current risk premium is basically close to the mid-2023 level. Assuming that the risk premium falls further from the current 7.0% to a low of 6.9% in mid-2023, corresponding to the Hang Seng Index level of 19,000 points. If it can return to the high level of sentiment in early 2023 (risk premium of 6.5%), it would correspond to the Hang Seng Index of around 20,000 points.

2) Under an optimistic situation, if subsequent policies further accelerate efforts to promote fundamental restoration (corporate profit growth rate reaches 10%; currently we expect profit growth of 5% in 2024 from a bottom-up strategy perspective), then the market is expected to open up further space, corresponding to the Hang Seng Index of 22,000 points. At this time, long-term value foreign investment is also expected to shift from the current low allocation to China, corresponding to capital inflows of about 42 billion US dollars, which is equivalent to the total outflow since 2021.

However, the fulfillment of the optimistic situation requires larger, faster, and more responsive fiscal spending as a prerequisite. This is also the main means to effectively address current credit contraction and inflationary pressure in the private sector. Until then, this expectation may still seem somewhat optimistic.

Chart: The risk premium for the Hang Seng Index has declined markedly, which is the main driving force behind the recent market rebound

Chart: The Hang Seng Index almost climbed to our first phase target (around 19,000 points)

Admittedly, there have been some recent positive changes at the policy level, such as opening purchase restrictions in more cities, such as Hangzhou and Xi'an; in addition, the April Politburo meeting's overall real estate coordination measures to speed up the issuance of ultra-long-term treasury bonds, absorb stocks, and optimize growth have all raised more expectations in the market, but the pace and progress of subsequent progress may be even more important.

In contrast, some recent data and policies may send signals that confuse the market, and also indicate that further policy support is still necessary. For example,

1) The newly announced April CPI rose to 0.3% year on year, and PPI fell 2.5% year on year. Although there was some recovery from the previous month, it has been negative for 19 consecutive months, indicating that demand is still weak. At the same time, rising prices of some utilities and raw materials may erode the profitability of some midstream and downstream enterprises;

2) The negative shift in social finance in April and the weakening of new RMB loans indicate that demand for private credit is still sluggish, and credit expansion is the key to driving growth recovery. Negative M1 growth also highlights the challenge of weakening the profitability of the corporate sector, how to balance “squeezing moisture” and liquidity support in a situation where finance is “squeezing moisture”;

3) In April 2024, PSL's net monthly repayment of 340 billion yuan was the highest in history, which also made the market worried about the speed and strength of the policy's liquidity investment;

4) The central bank's monetary policy implementation report for the first quarter placed special emphasis on the exchange rate. Considering that the Fed's interest rate cut expectations have been repeatedly postponed, this may suppress the room for short-term domestic monetary policy relaxation. Finally, Sino-US relations are still facing some uncertainty. There are reports that the Biden administration expects to raise import tariffs on Chinese electric vehicles and other products related to the new energy economy in the short term. Investors are advised to keep a close eye on this.

Chart: China's CPI maintained a slight positive increase in April, while PPI continued to decline over the past 19 months

Chart: China's financial data declined in April

In summary, the market has climbed to our target in the first phase. Until more symptomatic policy measures are implemented, we believe that the overall market may show a volatile trend, so compared to index performance, structural opportunities are more worthy of attention.

On the one hand, the high-dividend sector may reap the benefits of short-term market shocks, expectations of potential tax policy adjustments, and market concerns about growth under the latest inflation and social finance data to hedge against declining long-term interest rates. Recent news that individual investors (including public funds) in mainland China are expected to be exempted from the Hong Kong Stock Connect dividend tax triggered a new round of rising prices in the high-dividend sector last Friday.

Under current standards, when individual investors from the Mainland invest in H shares through Hong Kong Stock Connect, they are required to pay 20% dividend tax. For red chip stocks listed in Hong Kong, on the basis of Hong Kong Stock Connect's 20% personal income tax, it will also involve whether the company announced dividends have already been charged 10% corporate income tax, and eventually or in total, they will be deducted from the tax rate of 28% [10% + (1-10%) * 20% = 28%].

We believe that if the Hong Kong Stock Connect dividend tax relief is implemented, the scale of short-term direct relief may be relatively limited, bringing more of an emotional boost. However, in the medium to long term, it will help boost the attractiveness of Hong Kong stocks with high dividends, enhance the liquidity of Hong Kong stocks, and even reduce the AH premium for some companies.

Specifically, in addition to traditional high-dividend sectors (such as telecommunications, energy, raw materials, and utilities), some Internet and some everyday and durable consumer goods that have stable cash flow and are willing to increase shareholder returns through repurchases and dividends are also increasingly attracting investors' attention. In a sense, they are also a “new dividend concept.”

Chart: Hong Kong Stock Connect dividend tax collection standards under the current system

On the other hand, as the other side of the dumbbell strategy, high-quality growth sectors, such as the Internet, consumer electronics, and technological hardware, those in the midstream manufacturing industry, and the consumer services sector, which includes travel, travel, and leisure, are also worth paying attention to. Overall, it is reflected in a “dumbbell” configuration consisting of three main lines: dividends, technological growth, midstream overseas travel, and service consumption.

Specifically, the main logic underpinning our views above and the changes we need to pay attention to last week mainly include:

1) Trade: China's imports and exports both exceeded expectations in April. According to data released on Thursday, China's exports increased 1.5% year on year in April to 292.5 billion US dollars, and fell 7.5% year on year in March. Meanwhile, in April, China's imports unexpectedly increased by 8.4% year on year, which was significantly better than in March (down 1.9% year on year). The trade surplus also grew in April, climbing to US$72.4 billion, significantly higher than US$58.6 billion in March. Specifically, the US is still China's largest trading partner. China's imports from the US increased 9% year over year, while exports fell nearly 3%. Meanwhile, in April, China's exports to ASEAN increased 8% year on year, and imports increased 5%. By product, exports of automobiles, liquid crystal displays, and home appliances have increased, while imports of crude oil and natural gas have increased.

Chart: April import and export data rebounded from March low

2) Inflation: CPI continued to increase slightly and PPI continued to decline for 19 months. According to data released by the National Bureau of Statistics, China's CPI increased 0.3% year on year in April, slightly higher than the 0.1% increase in March. Meanwhile, the 2.5% year-on-year decline in PPI in April was narrower than the 2.8% decline in March, but it has been in a declining range for 19 consecutive months. Specifically, after excluding food and energy prices, the core CPI rose 0.7% year on year in April, slightly up from 0.6% in March, but it is still not that high. In terms of PPI, in the short term, as the issuance of government bonds is expected to accelerate, fiscal capital investment may support demand, but real estate recovery is still slow, and overall industrial product prices may continue to weaken.

3) Social finance credit data: Social finance grew negatively, and M1 also turned negative. M1 fell 1.4% year on year in April, down 2.5 percentage points from the previous month; M2 also fell to 7.2% year on year from 8.3% in March. At the same time, as a broad measure of credit, new social finance was reduced by nearly 200 billion yuan in April. This is the first time in recent years that this data has declined, indicating that domestic demand is still relatively weak, leading to a contraction in financing demand. Specifically, the repayment scale of government bonds in April exceeded the scale of issuance, which was the main factor leading to the decline in new social finance. The amount of new RMB loans added in April was only 730 billion yuan, which is significantly lower than the 3.1 trillion yuan in March, and also lower than the unanimous market forecast of 916 billion yuan.

4) Real estate: Major cities such as Hangzhou and Xi'an have completely abolished housing purchase restrictions. Specifically, the two major cities of Hangzhou and Xi'an have abolished existing housing purchase restrictions. This move is ostensibly an attempt by local governments to inject vitality into the real estate industry. After the Politburo meeting of the Central Committee ended at the end of April, several major cities, including Hangzhou, Xi'an, and Chengdu, abolished all housing purchase restrictions. Judging from current policies, only first-tier cities in the country go north to Guangzhou and Shenzhen, and Tianjin and Sanya still have housing purchase restriction policies. Future policy adjustments and optimizations in these cities deserve continued attention.

Chart: Major cities such as Hangzhou and Xi'an lift housing purchase restrictions

5) Liquidity: Southbound capital inflows continued last week, and more regional foreign capital inflows. Specifically, data from the EPFR shows that overseas active funds left the overseas Chinese stock market last week, totaling 190 million US dollars, but this is significantly narrower than the total outflow of 380 million US dollars in the previous week. Although active overseas capital has been flowing out of overseas Chinese stock markets for 45 consecutive weeks, the scale of outflows has continued to decline over the past three weeks. Southbound capital inflows remained strong last week. Specifically, mainland Chinese investors bought HK$11.4 billion in Hong Kong stocks southward through the Hong Kong Stock Connect last week, clearly exceeding the previous week's purchase scale of HK$6 billion.

Chart: Overseas active funds continue to flow out, while southbound capital inflows continue to be strong

Chart: Although the overall outflow of overseas capital continues, some regional capital shows signs of inflow

Focus on events

US CPI data for May 15, Chinese industrial value added and fixed asset investment data for May 17

[1] https://sc.people.com.cn/n2/2024/0511/c345167-40840049.html

[2] https://finance.eastmoney.com/a/202404303065843528.html

[3] https://www.ft.com/content/9b79b340-50e0-4813-8ed2-42a30e544e58

editor/tolk