Those holding Groupon, Inc. (NASDAQ:GRPN) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. The last month tops off a massive increase of 295% in the last year.

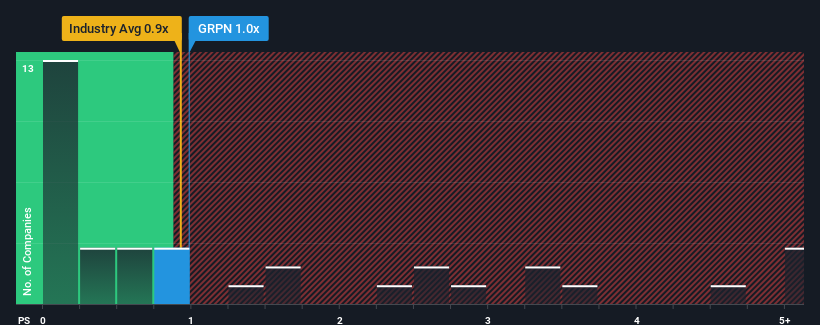

In spite of the firm bounce in price, there still wouldn't be many who think Groupon's price-to-sales (or "P/S") ratio of 1x is worth a mention when the median P/S in the United States' Multiline Retail industry is similar at about 0.9x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

NasdaqGS:GRPN Price to Sales Ratio vs Industry May 12th 2024

What Does Groupon's Recent Performance Look Like?

Groupon could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Groupon's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Some Revenue Growth Forecasted For Groupon?

In order to justify its P/S ratio, Groupon would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 9.0% decrease to the company's top line. As a result, revenue from three years ago have also fallen 60% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 2.0% as estimated by the three analysts watching the company. With the industry predicted to deliver 14% growth, the company is positioned for a weaker revenue result.

With this in mind, we find it intriguing that Groupon's P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Groupon's P/S?

Its shares have lifted substantially and now Groupon's P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Given that Groupon's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

You should always think about risks. Case in point, we've spotted 3 warning signs for Groupon you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.