If EPS Growth Is Important To You, Jabil (NYSE:JBL) Presents An Opportunity

If EPS Growth Is Important To You, Jabil (NYSE:JBL) Presents An Opportunity

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

对于初学者来说,收购一家向投资者讲述好故事的公司似乎是个好主意(也是一个令人兴奋的前景),即使该公司目前缺乏收入和利润记录。但是正如彼得·林奇所说 One Up On Wall 街,“远射几乎永远不会得到回报。”亏损的公司可以像海绵一样争夺资本,因此投资者应谨慎行事,不要一笔又一笔地投入好钱。

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Jabil (NYSE:JBL). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

如果这种公司不是你的风格,你喜欢创收甚至赚取利润的公司,那么你很可能会对捷普公司(纽约证券交易所代码:JBL)感兴趣。尽管利润不是投资时应考虑的唯一指标,但值得表彰能够持续生产利润的企业。

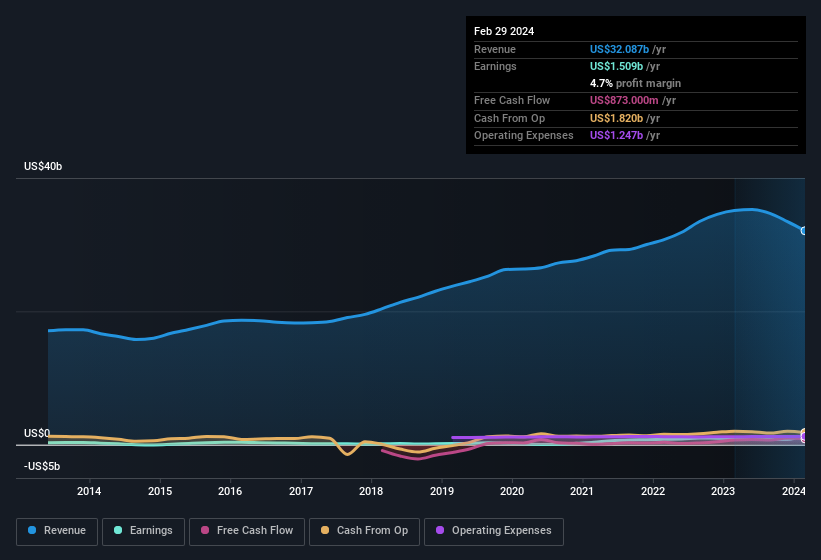

Jabil's Improving Profits

捷普提高利润

In the last three years Jabil's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. So it would be better to isolate the growth rate over the last year for our analysis. Outstandingly, Jabil's EPS shot from US$7.06 to US$12.51, over the last year. Year on year growth of 77% is certainly a sight to behold.

在过去的三年中,捷普的每股收益腾飞;如此之多,以至于用这些数字来推断长期估计有点不诚实。因此,最好将去年的增长率分开来进行分析。出人意料的是,捷普的每股收益在去年从7.06美元飙升至12.51美元。77%的同比增长无疑是一个值得一看的景象。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While Jabil may have maintained EBIT margins over the last year, revenue has fallen. This does not bode too well for short term growth prospects and so understanding the reasons for these results is of great importance.

仔细检查公司增长的一种方法是查看其收入以及利息和税前收益(EBIT)利润率如何变化。尽管捷普在去年可能保持了息税前利润率,但收入却下降了。对于短期增长前景而言,这并不是一个好兆头,因此了解这些结果的原因非常重要。

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

在下图中,您可以看到公司如何随着时间的推移实现收益和收入的增长。点击图表查看确切的数字。

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Jabil's forecast profits?

在投资中,就像在生活中一样,未来比过去更重要。那么,为什么不看看这个免费的Jabil的交互式可视化效果呢? 预测 利润?

Are Jabil Insiders Aligned With All Shareholders?

捷普内部人士是否与所有股东保持一致?

Owing to the size of Jabil, we wouldn't expect insiders to hold a significant proportion of the company. But we are reassured by the fact they have invested in the company. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$488m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

由于捷普的规模,我们预计内部人士不会持有该公司的很大一部分股份。但是他们投资了该公司,这让我们感到放心。事实上,他们有大量财富投资于此,目前价值4.88亿美元。这表明领导层在做出决策时会非常注意股东的利益!

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. A brief analysis of the CEO compensation suggests they are. The median total compensation for CEOs of companies similar in size to Jabil, with market caps over US$8.0b, is around US$14m.

尽管通过大量投资看到内部人士对公司抱有坚定的信心总是件好事,但股东询问管理层薪酬政策是否合理也很重要。对首席执行官薪酬的简要分析表明确实如此。市值超过80亿美元的规模与捷普公司首席执行官的总薪酬中位数约为1400万美元。

The CEO of Jabil only received US$4.8m in total compensation for the year ending August 2023. That looks like a modest pay packet, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

截至2023年8月的财年,捷普首席执行官仅获得了480万美元的总薪酬。这看起来像是微不足道的工资待遇,可能暗示着对股东利益的某种尊重。尽管首席执行官的薪酬水平不应成为公司看法的最大因素,但适度的薪酬是积极的,因为这表明董事会将股东利益放在心上。更笼统地说,它也可以是善治的标志。

Is Jabil Worth Keeping An Eye On?

捷普值得关注吗?

Jabil's earnings have taken off in quite an impressive fashion. The cherry on top is that insiders own a bucket-load of shares, and the CEO pay seems really quite reasonable. The strong EPS improvement suggests the businesses is humming along. Big growth can make big winners, so the writing on the wall tells us that Jabil is worth considering carefully. Still, you should learn about the 3 warning signs we've spotted with Jabil (including 1 which is significant).

Jabil的收入以令人印象深刻的方式实现了增长。最重要的是,内部人士拥有大量股票,首席执行官的薪酬似乎非常合理。每股收益的强劲改善表明企业正在蓬勃发展。大幅增长可以造就大赢家,因此墙上的文字告诉我们,捷普值得仔细考虑。不过,你应该了解我们在Jabil身上发现的3个警告信号(包括一个重要的警告信号)。

Although Jabil certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with insider buying, then check out this handpicked selection of companies that not only boast of strong growth but have also seen recent insider buying..

尽管捷普肯定看起来不错,但如果内部人士买入股票,它可能会吸引更多的投资者。如果你想看看有内幕买入的公司,那就看看这些精心挑选的公司,这些公司不仅增长强劲,而且最近也出现了内幕买盘。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文中讨论的内幕交易是指相关司法管辖区内应报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。