Key Insights

- Meritage Homes will host its Annual General Meeting on 16th of May

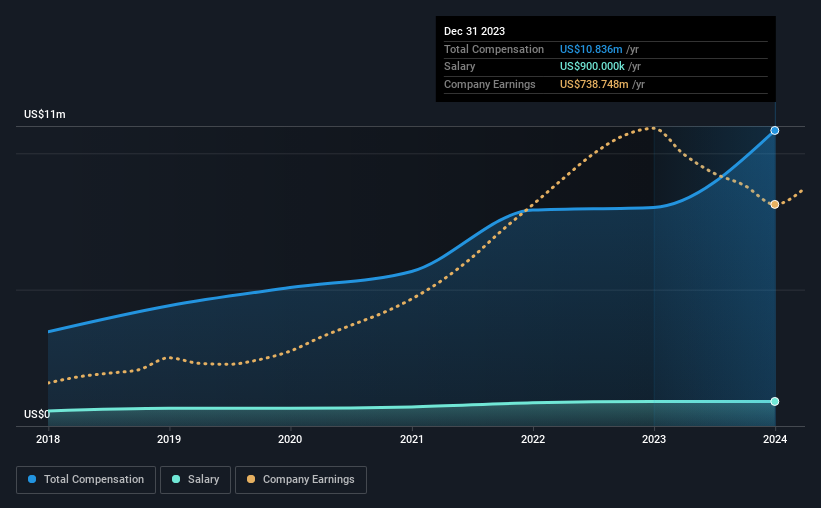

- Total pay for CEO Phillippe Lord includes US$900.0k salary

- Total compensation is similar to the industry average

- Meritage Homes' total shareholder return over the past three years was 65% while its EPS grew by 19% over the past three years

It would be hard to discount the role that CEO Phillippe Lord has played in delivering the impressive results at Meritage Homes Corporation (NYSE:MTH) recently. Coming up to the next AGM on 16th of May, shareholders would be keeping this in mind. It is likely that the focus will be on company strategy going forward as shareholders hear from the board and cast their votes on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

How Does Total Compensation For Phillippe Lord Compare With Other Companies In The Industry?

According to our data, Meritage Homes Corporation has a market capitalization of US$6.6b, and paid its CEO total annual compensation worth US$11m over the year to December 2023. Notably, that's an increase of 35% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at US$900k.

On examining similar-sized companies in the American Consumer Durables industry with market capitalizations between US$4.0b and US$12b, we discovered that the median CEO total compensation of that group was US$11m. This suggests that Meritage Homes remunerates its CEO largely in line with the industry average. What's more, Phillippe Lord holds US$18m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$900k | US$900k | 8% |

| Other | US$9.9m | US$7.1m | 92% |

| Total Compensation | US$11m | US$8.0m | 100% |

On an industry level, around 17% of total compensation represents salary and 83% is other remuneration. In Meritage Homes' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Meritage Homes Corporation's Growth

Meritage Homes Corporation's earnings per share (EPS) grew 19% per year over the last three years. The trailing twelve months of revenue was pretty much the same as the prior period.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Meritage Homes Corporation Been A Good Investment?

Boasting a total shareholder return of 65% over three years, Meritage Homes Corporation has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We did our research and identified 3 warning signs (and 1 which doesn't sit too well with us) in Meritage Homes we think you should know about.

Important note: Meritage Homes is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.