The US April CPI report to be released next week may be a “downside surprise”. Can the script for interest rate cuts be moved out again?

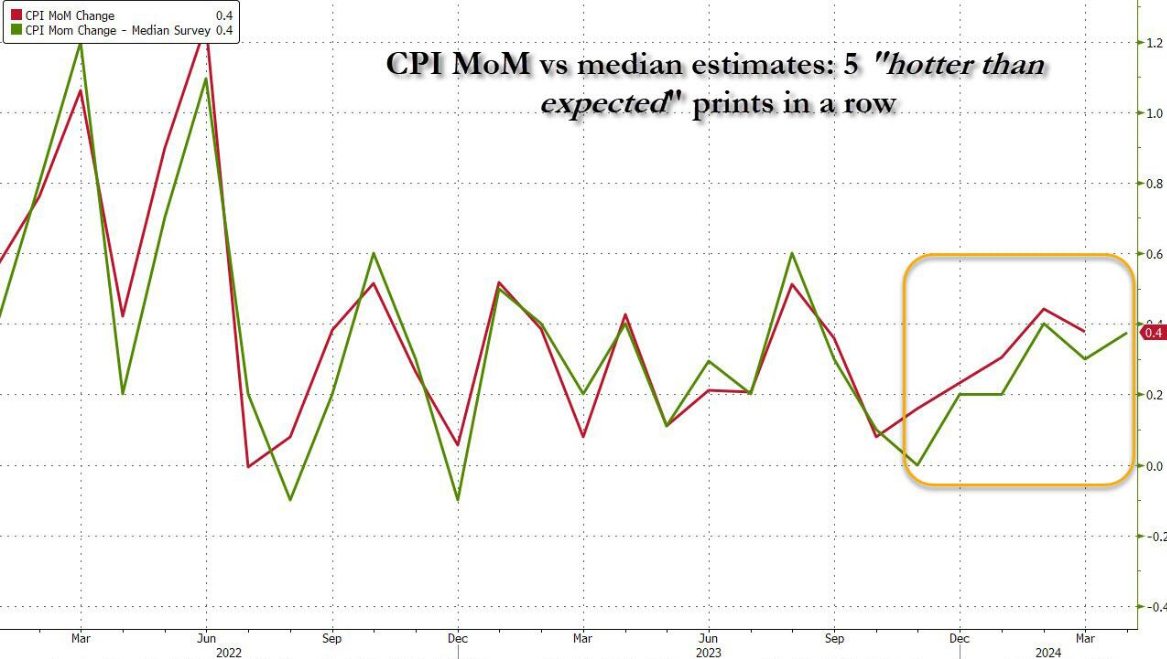

After the US March CPI announced last month was higher than the median forecast for 5 consecutive months, the market more or less gave up hope that the Fed would cut interest rates in the near future and lowered expectations of interest rate cuts before the end of this year to only about one time left. Biden has vowed to predict that the Federal Reserve will cut interest rates “before the end of this year”. Of course, he meant before the election, because any move after November 2024 would only benefit Trump.

The election is imminent, and whether the Federal Reserve is willing to admit it or not, it is more political than ever. Will Biden really allow the Federal Reserve and various propaganda departments to keep interest rates high and suppress consumer sentiment until the critical November election?

According to financial blogger Zero Hedge, the answer is “impossible,” which said that the April CPI report to be released next week would be a “downside surprise” because the lagging OER (Equivalent Rent for Owners' Homeowners) “collapsed.” It has also previously warned that “rent/OER inflation over the next 9-12 months (43% of the CPI basket) will unexpectedly rise, even if rents are actually rising now...”

Now, it is believed that the US Bureau of Statistics will actively falsify OER data in the months before the election, so that the CPI “falls short of expectations” can have more than zero hedging. In the process, interest rate cuts will once again be possible.

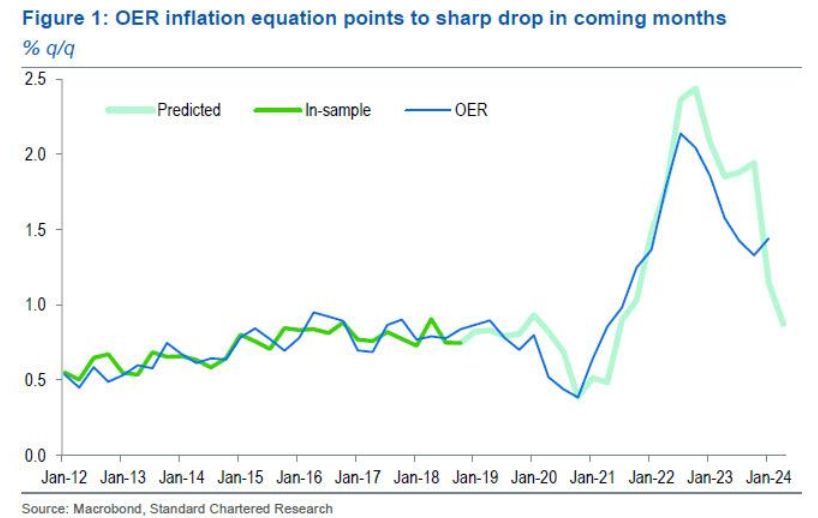

Steven Englander (Steven Englander), chief foreign exchange strategist at Standard Chartered Bank, wrote that Federal Reserve Chairman Powell confidently stated at the FOMC press conference on May 1 that lower housing costs may reduce the core inflation rate over time. England and Germany said they were shocked by Powell's statement.

“As we take a close look at housing costs, particularly the OER portion, we found reason to be optimistic that housing inflation could fall soon and reduce the core inflation rate,” he wrote in a statement on Thursday.

As shown in the chart below, England and Germany carried out a regression analysis of actual and predicted OER and found that “Powell's optimism may be justified” because the analysis indicated that “based on the stable return that has been proven to be stable in recent years, OER will decline sharply in the next few months.”

The analysis is based on an experimental series of new tenant rents and all tenant rents constructed by Federal Reserve and Bureau of Labor Statistics researchers. As can be seen from the chart, the regression results show that the rise in the first quarter is an abnormal phenomenon. The next few months will once again face downward pressure, and “there may be a sharp decline.”

The formula predicts that the average OER month-on-month inflation rate in the second quarter was only 0.29%, which is not far from the prevailing level in 2015-19. In contrast, the OER month-on-month inflation rate for the first quarter of 2024 was 0.48%. This is important because OER accounts for 33% of the core CPI, so this decline will reduce the core CPI by 0.06% month-on-month. This means that if more projects fall short of expectations, then this variable will push the core CPI down from an estimated 0.3% to 0.2%, or even lower.

Since the OER formula tracks lagging private sector market rent data, which has been falling recently (even if rents in many US sectors start to rise again), England believes that OER price inflation will continue to weaken in subsequent quarters. The conclusion, he said, was clear:

“This level of improvement will encourage expectations that anti-inflation will reoccur and fall to a level sufficient to allow the FOMC to lower policy interest rates.”

However, England cautioned that his conclusion had two major risks. The first risk is that the Bureau of Labor Statistics and the Federal Reserve's experimental data on new tenants and rents for all tenants is quarterly data, so his judgment on quarterly changes may be correct, but his judgment on monthly changes may be wrong. The Bureau of Labor Statistics changed the calculation method last year. This means that OER currently estimates based on a small sample of single-family rental housing, which has brought about the possibility of random fluctuations in OER data.

The second risk is that high demand for single-family homes may cause rents to rise disproportionately, and will continue to do so. However, most homeowners have locked in lower mortgage interest rates and won't face this increase in housing costs.

England finally quoted Powell's statement, which he said caught his attention: “Given the rent situation in the market, I still expect housing service inflation to show up over time in measurable housing service inflation.” He pointed out, “Given the high OER inflation rate in the first quarter, I was shocked by his (Powell) confidence, and he seemed to be no longer focusing on so-called supercore inflation (not including food, energy, and housing rent services), but instead looking for lower rental inflation as a sufficient reason to cut interest rates.”

Zero hedging finally added that OER in the CPI will catch up with falling rents now, but by the time the Fed actually cuts interest rates, the 12-18 month lag between OER data and real-time indicators means that the Fed will raise interest rates when the next surge in rents begins. Needless to say, further easing will only exacerbate this trend. Coupled with the fact that the US has accepted tens of millions of illegal immigrants to raise rents over the past three years, this means that by this time in 2025, rents will actually soar, and the “Arthur Burns Fed Ghost” will actually be released. (Arthur Burns, a former chairman of the Federal Reserve, failed to solve the problem of soaring inflation in the late 70s.)

Editor/Jeffrey