BeautyHealth (NASDAQ:SKIN) Beats Q1 Sales Targets But Quarterly Guidance Underwhelms

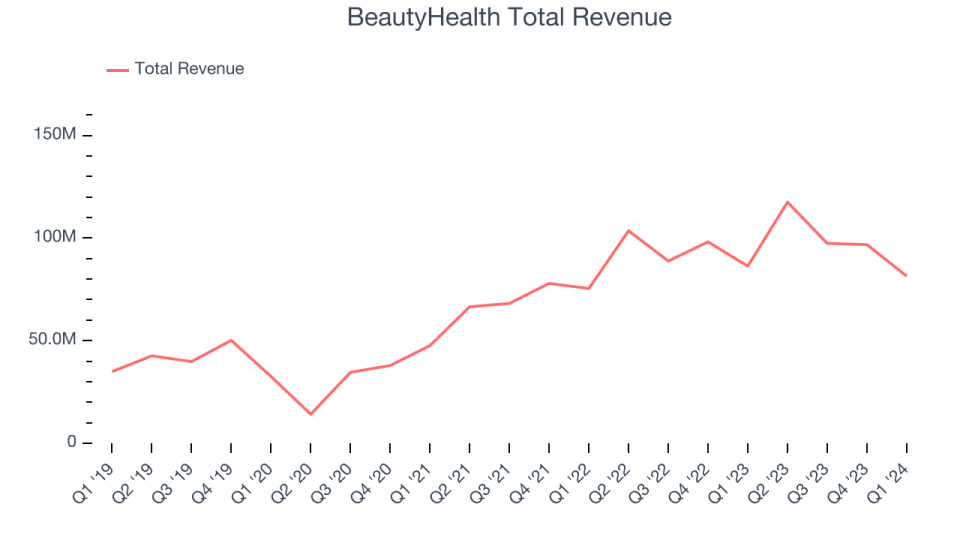

Skincare company BeautyHealth (NASDAQ:SKIN) announced better-than-expected results in Q1 CY2024, with revenue down 5.7% year on year to $81.4 million. On the other hand, next quarter's revenue guidance of $99 million was less impressive, coming in 8.4% below analysts' estimates. It made a GAAP loss of $0.10 per share, improving from its loss of $0.15 per share in the same quarter last year.

Is now the time to buy BeautyHealth? Find out in our full research report.

BeautyHealth (SKIN) Q1 CY2024 Highlights:

Revenue: $81.4 million vs analyst estimates of $80.65 million (small beat)

EPS: -$0.10 vs analyst estimates of -$0.14 (26.7% beat)

Revenue Guidance for Q2 CY2024 is $99 million at the midpoint, below analyst estimates of $108.1 million

Full year adjusted EBITDA guidance of at least $4 million was ahead

Gross Margin (GAAP): 59.5%, down from 62.7% in the same quarter last year

Market Capitalization: $423.5 million

"Our first quarter results demonstrate the progress we are making on our near-term strategic priorities, including sales excellence, operational excellence, and financial discipline,” said BeautyHealth Chief Executive Officer Marla Beck.

Operating in the emerging beauty health category, the appropriately named BeautyHealth (NASDAQ:SKIN) is a skincare company best known for its Hydrafacial product that cleanses and hydrates skin.

Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Sales Growth

BeautyHealth is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 43.1% over the last three years was incredible for a consumer staples business.

This quarter, BeautyHealth reported a rather uninspiring 5.7% year-on-year revenue decline to $81.4 million in revenue, in line with Wall Street's estimates. The company is guiding for a 15.7% year-on-year revenue decline next quarter to $99 million, a reversal from the 13.5% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 4.8% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

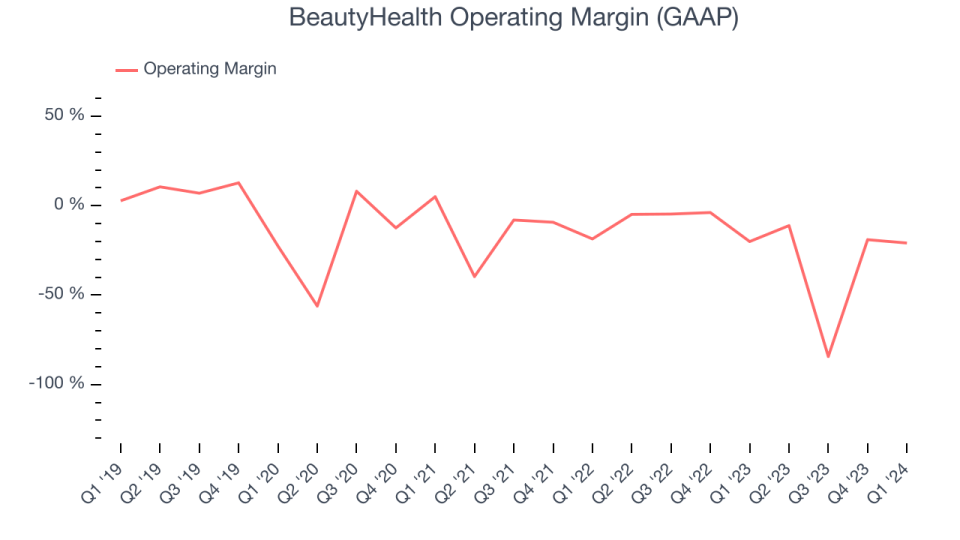

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

In Q1, BeautyHealth generated an operating profit margin of negative 20.9%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

There are few unprofitable publicly traded consumer staples companies, and over the last two years, BeautyHealth has been one of them. Its high expenses have contributed to an average operating margin of negative 20.9%. On top of that, BeautyHealth's margin has declined by 25.2 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.

Key Takeaways from BeautyHealth's Q1 Results

We enjoyed seeing BeautyHealth exceed analysts' EPS expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. For the full year, the company's adjusted EBITDA guidance of at least $40 million is ahead of expectations. On the other hand, its revenue guidance for next quarter missed analysts' expectations and its gross margin missed Wall Street's estimates. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $3.59 per share.

So should you invest in BeautyHealth right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.