Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that China Cyts Tours Holding Co., Ltd. (SHSE:600138) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is China Cyts Tours Holding's Net Debt?

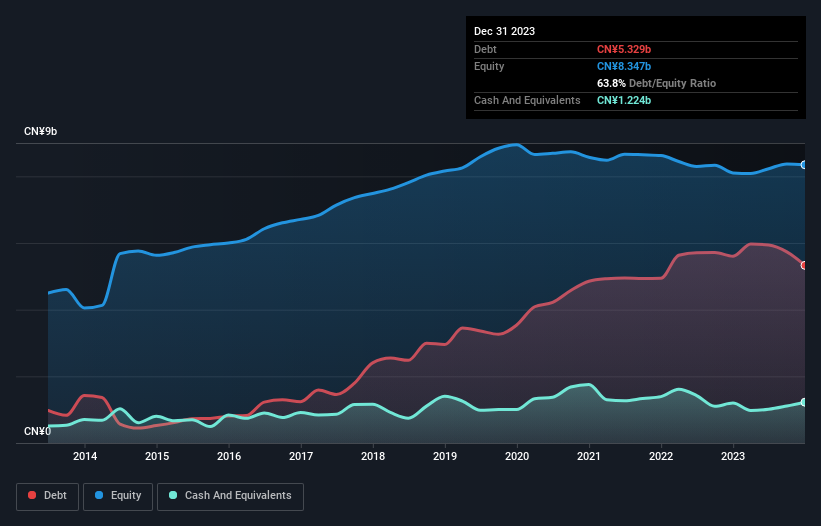

As you can see below, China Cyts Tours Holding had CN¥5.33b of debt at December 2023, down from CN¥5.60b a year prior. However, it also had CN¥1.22b in cash, and so its net debt is CN¥4.11b.

How Healthy Is China Cyts Tours Holding's Balance Sheet?

The latest balance sheet data shows that China Cyts Tours Holding had liabilities of CN¥6.84b due within a year, and liabilities of CN¥2.10b falling due after that. Offsetting these obligations, it had cash of CN¥1.22b as well as receivables valued at CN¥2.65b due within 12 months. So its liabilities total CN¥5.06b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of CN¥7.87b, so it does suggest shareholders should keep an eye on China Cyts Tours Holding's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

China Cyts Tours Holding's debt is 4.8 times its EBITDA, and its EBIT cover its interest expense 4.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Notably, China Cyts Tours Holding made a loss at the EBIT level, last year, but improved that to positive EBIT of CN¥580m in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if China Cyts Tours Holding can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, China Cyts Tours Holding actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

On our analysis China Cyts Tours Holding's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. In particular, net debt to EBITDA gives us cold feet. Looking at all this data makes us feel a little cautious about China Cyts Tours Holding's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example China Cyts Tours Holding has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.