这次FOMC会议没有提供新的点阵图和预测表,市场的关注点集中在鲍威尔的发言上。去年12月份鲍威尔转向降息指引,市场现在想知道美联储是继续持有降息的观点,还是正在放弃这种想法。此外,由于年初以来的通胀数据持续超预期,市场也想了解是否存在重启加息的可能性。

这次FOMC会议没有提供新的点阵图和预测表,市场的关注点集中在鲍威尔的发言上。去年12月份鲍威尔转向降息指引,市场现在想知道美联储是继续持有降息的观点,还是正在放弃这种想法。此外,由于年初以来的通胀数据持续超预期,市场也想了解是否存在重启加息的可能性。Source: CICC Macro

Authors: Xiao Jiewen, Zhang Wenlang

The May meeting of the Federal Reserve kept interest rates unchanged, in line with expectations. The monetary policy statement acknowledged the stickiness of inflation, and Powell said there was insufficient confidence in interest rate cuts, indicating that the Federal Reserve's interest rate cut threshold has been raised significantly. Powell also denied the option to raise interest rates and announced that the downsizing was about to slow down, which gave the market a sigh of relief.

Overall, we think Powell's guidelines this time are quite reasonable. He is no longer leading interest rate cuts like before. This is the right approach, and it is also a good thing for the market. We maintain our previous judgment that the Federal Reserve may cut interest rates only once this year, in the fourth quarter.

The FOMC meeting did not provide a new bitmap or forecast table, and the market's focus was on Powell's statement. Powell switched to interest rate cuts in December of last year. The market now wants to know if the Federal Reserve continues to hold the view of cutting interest rates or is abandoning this idea. Furthermore, since the inflation data since the beginning of the year continued to exceed expectations, the market also wanted to know if there is a possibility of restarting interest rate hikes.

The FOMC meeting did not provide a new bitmap or forecast table, and the market's focus was on Powell's statement. Powell switched to interest rate cuts in December of last year. The market now wants to know if the Federal Reserve continues to hold the view of cutting interest rates or is abandoning this idea. Furthermore, since the inflation data since the beginning of the year continued to exceed expectations, the market also wanted to know if there is a possibility of restarting interest rate hikes.

Judging from Powell's statement, we think the Federal Reserve's threshold for cutting interest rates has been raised significantly.

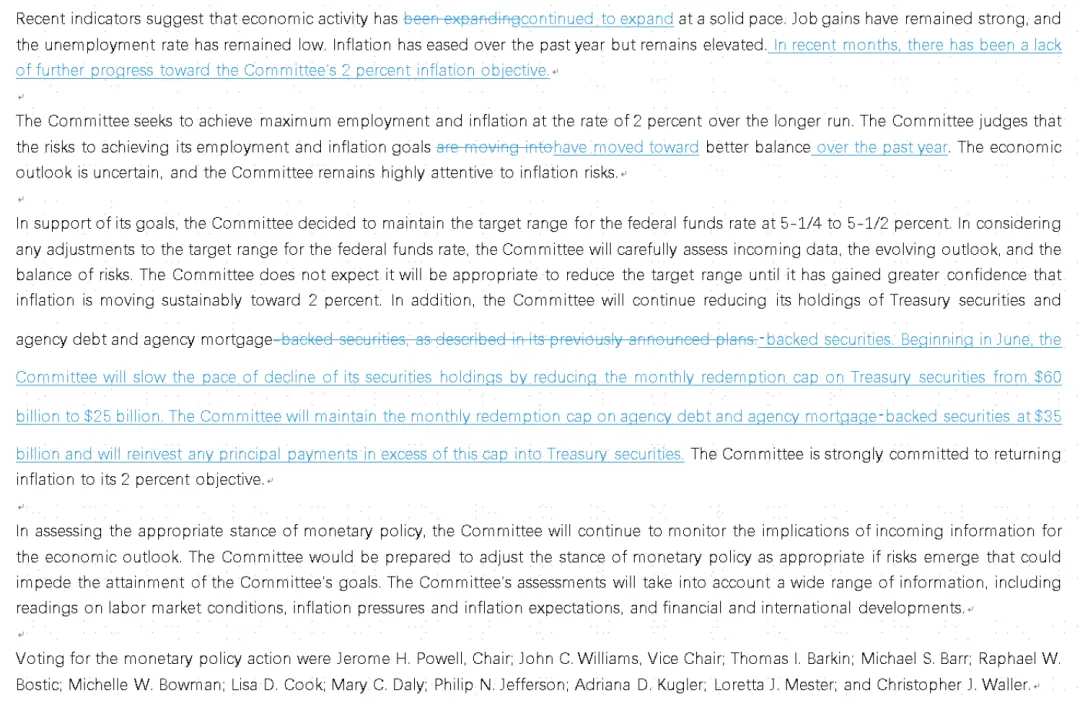

First, the Federal Reserve acknowledged in its monetary policy statement that in recent months, there has been a lack of further progress in achieving the 2% inflation target (in recent months, there has been a lack of further progress made the Committee's 2 percent inflation objective). This shows that officials have clearly understood the resilience of inflation.

Second, Powell said that these inflation data did not give the Federal Reserve enough confidence to cut interest rates, and officials needed more time to observe the trend of inflation.

Powell's statement was in line with our expectations. We pointed out earlier that based on the current economic and inflation situation, it is already difficult for the Federal Reserve to follow the guideline of cutting interest rates three times during the year. Our benchmark situation is to cut interest rates only once this year, and the timing is in the fourth quarter.

We think there are two possible situations where the Federal Reserve will cut interest rates during the year:

The first is a further slowdown in core PCE inflation, which the Federal Reserve is most concerned about. In particular, rent-excluded service inflation (supercore), which is closely related to the labor market, has cooled down. Under such circumstances, the timing of interest rate cuts will depend on the extent to which inflation slows down.

The second type is a marked deterioration in the labor market. For example, the unemployment rate rose above 4.3% (that is, an increase of 0.5 percentage points from the current level), and the Federal Reserve cut interest rates when inflation falls short of the standard in order to maximize employment in the “double goal” of monetary policy. This situation also means that the risk of economic recession is rising, and interest rate cuts will also be viewed by the market as a negative signal.

As for restarting interest rate hikes, we think it's unlikely.

One reason is that the Federal Reserve believes that the current monetary policy is restrictive and has had some effect in cooling economic activity. For example, the number of job vacancies has declined since this year and the credit card loan default rate has risen, all of which have helped curb inflation.

Another reason is that this is an election year, and it takes a lot of courage to raise interest rates. Judging from the performance since the end of last year, the current Federal Reserve has a clear dovish bias (dovish bias), so there will be no further increase in interest rates unless inflation rises sharply (such as “secondary inflation”).

Excluding interest rate hikes is particularly important for the market, because the current market can accept that the Fed will not cut interest rates this year, but it cannot bear the “weight of interest rate hikes.” Interest rate hikes mean that inflation continues to exceed expectations, the risk of “stagflation” in the economy is rising, and the “double death of equity and debt” is making a comeback. This is an outcome that most people don't want to see. This also explains why today Powell denied the option to raise interest rates, and the stock and bond markets were relieved.

Another change in this meeting is that the downsizing is about to slow down. The Federal Reserve announced that starting in June, it will lower the upper limit of the monthly reduction of US Treasury bonds from 60 billion US dollars to 25 billion US dollars, and keep the upper limit of reducing MBS at 35 billion US dollars per month. This means that the overall downsizing will drop from $95 billion to $60 billion.

The Federal Reserve's slowdown is in line with our expectations, but the reduction in the scale of US Treasury debt reduction is higher than we anticipated. It can also be seen from this that the Federal Reserve does not want to experience liquidity risks due to downsizing similar to those in October 2019. This is a favorable factor for reserves and interbank liquidity in the second half of the year.

Overall, we think Powell's guidelines this time are quite reasonable. He is no longer leading interest rate cuts like before. This is the right approach, and it is also a good thing for the market.

We pointed out in a series of previous reports that there is great uncertainty about US inflation, and there is a high risk that the Federal Reserve prematurely prepares to cut interest rates; this is true now. The interest rate cut guidelines given by the Federal Reserve in December last year led to easier financial conditions and increased economic and inflationary flexibility. Looking back now, this may be out of place. The good news is that now the Federal Reserve has adjusted its attitude and is no longer in a hurry to cut interest rates. This is actually more beneficial to fighting inflation and stabilizing financial markets.

Looking ahead, we believe that under the premise that the risk of inflation is manageable, the Federal Reserve's current monetary policy will not have too negative impact on the economy. US companies and residents will gradually adapt to keeping interest rates high for longer (high for longer), and the economic growth rate is expected to remain above the 2% trend during the year.

Editor/Jeffy