Prediction: These 2 AI Stocks Will Be Worth More Than Nvidia by 2030

Nvidia (NASDAQ: NVDA) is the now third-largest company in the world, valued at around $2 trillion. Hot on its heels is Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), while Meta Platforms (NASDAQ: META) is about $750 billion smaller.

Although Nvidia is larger right now, I think by 2030, Alphabet and Meta will have taken significant leads over it -- for a fairly simple reason.

Nvidia's GPUs are being dethroned by company-specific hardware

Nvidia's rise has been nothing short of remarkable, although many may consider it unsustainable. Nvidia sells graphics processing units (GPUs) capable of handling intense computational workloads. This makes them a great choice for tasks like artificial intelligence (AI) model training or data collection. However, GPUs aren't necessarily the best hardware for processing AI models.

If a company knows what kind of data structure it wants its AI models in, it can make custom chips optimized for these workloads. That's exactly what Alphabet did with its tensor processing unit (TPU), and what Meta accomplished with its Meta Training and Inference Accelerator (MTIA). As these types of use-specific hardware become more popular, demand should decrease for Nvidia's GPUs.

Make no mistake: GPUs will still be needed because of their versatility in running models that aren't optimized for a particular system. And the rising use of custom chips alone likely won't be enough to lift the market caps of Alphabet and Meta past Nvidia's by 2030.

Nvidia's products aren't subscription-based

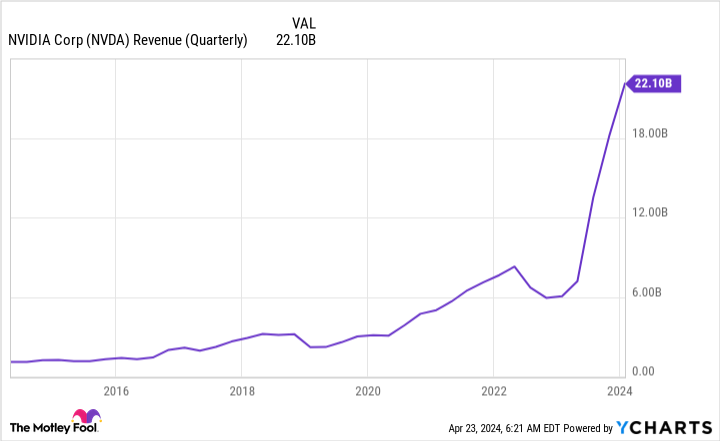

The biggest problem facing Nvidia over the next few years will be how to sustain its incredible revenue figures. Since the demand for GPUs spiked early last year, Nvidia's sales reached unprecedented levels.

Nvidia's products aren't quite subscription purchases -- they're one-time buys. Once a company outfits a data center with hundreds or thousands of GPUs, it's ready to work and will stay online until it's upgraded or replaced. But, refresh cycles typically occur anywhere between two and five years. That means many companies buying today will be purchasing GPUs a few years from now. However, it's unknown if they'll be purchasing at the frequency we're seeing now, as many AI models may have been developed and new ones aren't necesasry. Predicting the future isn't easy, but with Nvidia's stock it requires a bit of foresight.

Because many companies right now are racing to set up systems capable of supporting the newest AI software, Nvidia is seeing a massive demand spike. Eventually, though, demand will level off. But what investors don't know is if the spike will continue rising for a while, or if we're nearing the peak.

If we're nearing the peak, Nvidia might not be able to hold onto its current market cap for long.

By contrast, Alphabet and Meta have been experiencing more of a steady rise, and could maintain those trends. Although both companies are making heavy investments in AI and innovative technologies, each primarily uses AI for one purpose -- to improve the effectiveness of the advertising on their platforms. Advertising sales are at the core of what each business does. And with Meta's social media platforms and Alphabet's family of Google products used daily by billions of people, it's safe to say that each has a recurring-revenue model.

Although this model is far more sustainable than Nvidia's, it has its own weaknesses.

The advertising market is cyclical, just like the chip business, so Alphabet and Meta will have down years as well as growth years. However, they should see less aggressive revenue drops than Nvidia.

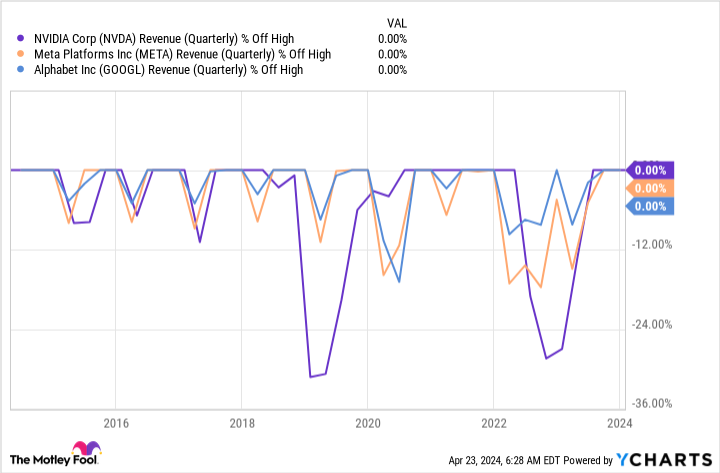

The chart below illustrates how far each company's revenue fell from its all-time highs during one of the cyclical downturns. Because all three recently reported new records on their top lines, the chart shows that they're 0% off their highs. But if you look back a few years, you'll see that Nvidia's revenue dropped by more than 30% from its prior all-time high in 2019, while the worst revenue slumps of Meta and Alphabet were only around 10% to 15%.

This is a key factor, as a sales drop for all companies is coming, but Nvidia's will be more severe than the one suffered by the other two.

With Nvidia's products slated to have weaker demand soon due to the completion of some infrastructure build-out, I'm confident that Alphabet and Meta will surpass Nvidia in size by 2030.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $537,692!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 30, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Keithen Drury has positions in Alphabet and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Meta Platforms, and Nvidia. The Motley Fool has a disclosure policy.

Prediction: These 2 AI Stocks Will Be Worth More Than Nvidia by 2030 was originally published by The Motley Fool