The Bank of Japan ended its negative interest rate policy in March of this year, keeping interest rates at 0%-0.1%. This is the first rate hike since 2007, as shown in the chart below.

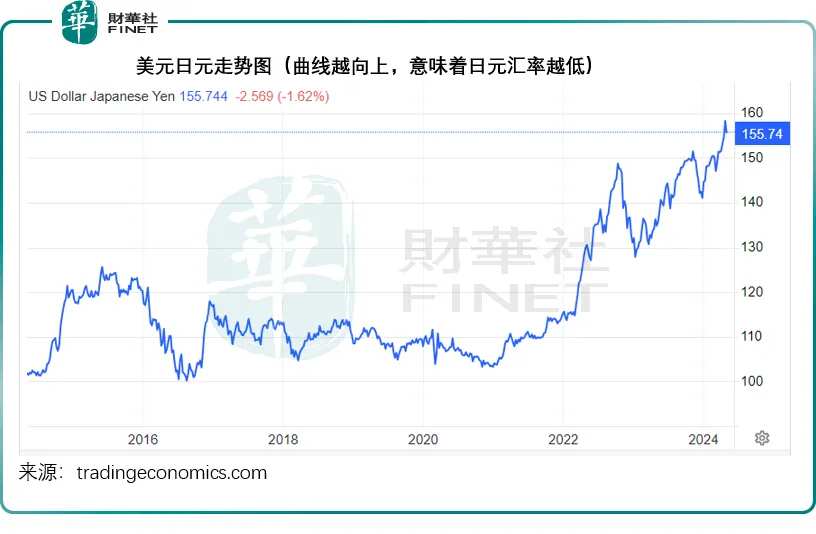

However, the exchange rate of the yen against the US dollar was not boosted by this. Instead, it fell again and again. It fell to the 160 level in the early part of April 29, 2024. Although it soon fell below 160 due to intervention by the Bank of Japan, it was still weak and failed to break through 155. See chart below.

The yen began to have negative interest rates in February 2016. As can be seen from the chart above, the exchange rate of the yen against the US dollar continued to decline in February 2022 (the higher the value, the lower the exchange rate of yen against the US dollar). It can be seen that the two are highly correlated.

What is the root cause of the depreciation of the yen?

The widening spread is the most intuitive explanation for this trend.

The Federal Reserve began the interest rate hike cycle in March 2022. According to general expectations, it is now at a high level in the current US dollar interest rate cycle, because the market expects the Fed to cut interest rates starting in the second half of this year.

However, judging from recent US employment data and the somewhat stubborn consumer price index, the market seems to be aware that expectations for the Federal Reserve to begin a cycle of interest rate cuts are a bit too optimistic.

In other words, the US dollar interest rate is likely to remain at a high level for a long period of time. At the same time, in order to stabilize exchange rate expectations, the Bank of Japan stated that it will still maintain an easy monetary policy, which means it may not raise interest rates further.

This means that the interest rate spread between the US dollar and the yen will be at a high level for a period of time. For speculative capital, this is undoubtedly an advantageous time to short the yen — selling the yen, buying high-interest currency, and then closing the Japanese yen position, you can not only earn an interest difference, but also earn another exchange rate difference when the yen depreciates further. It's a profitable business.

As shown in the chart below, the interest rate spread between the US 10-year Treasury interest rate and the yen 10-year Treasury interest rate rose sharply after 2022, and has remained at a high level of more than 300 basis points since the end of 2022. Furthermore, in October 2023, when the Fed's interest rate hike cycle may peak and is at its peak, breaking through 400 basis points.

However, as can be seen from the chart above, interest spreads actually declined at the end of 2023. Although they have recently rebounded slightly due to speculations that the Federal Reserve may delay the interest rate cut cycle, they have not returned to the level of the end of 2023. Why did the yen continue to decline?

According to Caihua News, speculative activity should be the main reason — betting that the Bank of Japan will not unexpectedly interfere with the foreign exchange market on a large scale. On the other hand, Japan's economic fundamentals seem to have not improved significantly, prompting capital to quickly escape from Japanese assets and move to gold (safe haven), US dollars (higher interest), and emerging markets (such as China).

According to economic data just released by Japan, in the fourth quarter of 2023 (September to December 2023), its real GDP (based on total social expenditure) was 142.64 trillion yen, up 1.20% year on year, the lowest increase in the four quarters of 2023, as shown in the chart below.

Looking at sector segments, Caihua News noticed that in the fourth quarter of 2023, household consumption expenditure, which is the largest component of Japan's GDP, actually fell by 0.52% year on year, while government spending only increased by 0.1%. Exports should have contributed the most to its actual GDP growth, with a year-on-year increase of 3.52%.

As shown in the chart below, as an export-oriented economy, changes in Japan's export trade had a huge impact on its actual GDP. At the height of the epidemic in 2020, due to the decline in export trade, despite continued growth in government spending, its overall GDP growth rate of 1.92% increased by 1.92% compared to the previous year due to the growth effect of exports, despite a slowdown in household consumption expenditure and government spending growth.

Consumption expenditure growth in Japanese households is weak, but the depreciation of the yen has encouraged a large number of tourists to travel and shop in Japan, which will help boost domestic demand. At the same time, the depreciation of the yen will also benefit Japanese companies' exports. This is a benefit of the yen exchange rate being pressured.

According to data from Japan's Ministry of Finance, Caika reported that Japan's export value increased 7.32% year-on-year to 9.47 trillion yen in March of this year (the latest decline in yen began in early March); the value of imports fell 5.13% year over year to 9.08 trillion yen; and generated a trade surplus of 387.01 billion yen.

However, the continued depreciation of the yen exchange rate also has its drawbacks. Japan is a country that is relatively resource-poor, and many resources, minerals, and consumer goods need to be imported.

Taking 2023 as an example, Japan's trading partner with the highest net import value is Australia and the Middle East (especially the Arab Emirates), because it needs to import minerals from Australia to be processed into finished products, such as importing large amounts of iron ore, processed into steel to support the development of its automobile manufacturing and export industries — automobiles are the industry with the highest export value from Japan, and they also need to import fuel from the Middle East to support domestic consumption.

Therefore, the depreciation of the yen will cause domestic production prices and consumer prices to rise — the price of imported products will rise due to the depreciation of the yen. For example, due to the depreciation of the yen, steel mills in Japan need to pay a higher price in yen for imported mineral products, leading to an increase in production costs — if the price cannot be transferred to export prices, manufacturers will absorb losses; similarly, consumers need to pay higher yen prices for imported gasoline, which will suppress their desire to consume.

Furthermore, according to IMF data, the ratio of Japan's treasury debt to GDP continued to rise, reaching 261.3% in 2022, while according to commodity.com data, the ratio was still as high as 241.64% by April 16, 2024. In other words, the government's debt far exceeds its annual revenue, which will increase the cost of government borrowing and fiscal pressure.

This was the main reason for the Bank of Japan's quick market entry intervention when the yen fell to 160.

Everyone may be concerned, how will the depreciation of the yen affect Buffett, the “stock god” who has vigorously entered the Japanese capital market?

Response to the depreciation of the yen and Buffett's deal

Buffett already bought five Japanese conglomerates as early as August 2020, namely$Mitsubishi (8058.JP)$,$Mitsui (8031.JP)$,$ITOCHU (8001.JP)$,$Marubeni (8002.JP)$und$Sumitomo (8053.JP)$, and it continues to increase its holdings.

These five companies are no ordinary people; they have a long historical background and a global scope of business. What is particularly noteworthy is that these companies all have one characteristic in common: mineral resources constitute their main source of revenue. In addition to this, the business reach of these companies extends to all aspects of consumer life in Japan and abroad, showing the characteristics of diversification of their business.

As mentioned earlier, Japan has obvious deficiencies in mineral resources. Despite this, as an important industrial force in the world, Japan's industrial production is highly dependent on mineral resources, such as iron ore, copper, lead, and nickel. To meet this challenge, Japan's Ministry of Economy, Trade and Industry actively guided large domestic enterprises to invest in mineral resources abroad as early as the last century. It is worth mentioning that the five major groups Buffett invests in are huge in the field of mineral investment, so they can make full use of Japan's market demand and economic development opportunities. Furthermore, since the mineral resources of these companies are mainly concentrated overseas, they are relatively less affected by the depreciation of the yen in the operation and management of mineral resources.

As shown in the chart below, the five major groups have accumulated a cumulative increase of more than 70% since Japanese stocks surged in 2022. Among them, the stock prices of MITSUBISHI CORP and Mitsui & Co., Ltd. have more than doubled. Since this year, the five major groups have maintained strong double-digit increases, showing strong momentum for capital appreciation.

Since the Japanese stock market surged in 2022, the five major groups have accumulated gains of more than 70%. In particular, it is worth mentioning that the stock prices of Mitsubishi Corporation and Mitsui & Co., Ltd. have more than doubled. And this year, the five major groups have maintained strong double-digit growth, showing their strong potential for capital appreciation.

What is even more interesting is the recent Japanese yen bond issuance and financing strategy adopted by Buffett, whose capital is used to cover general business operation needs. This transaction is essentially an act of arbitrage. The specific procedure is to borrow yen at a lower cost, then convert these funds to other high-interest currencies, and invest in high-interest assets. When the bond matures, the funds are then exchanged back to Japanese yen to complete the debt repayment operation.

from$Berkshire Hathaway-B (BRK.B.US)$As can be seen from the documents submitted by the US Securities Regulatory Commission, the total principal amount of this batch of bonds is 283.3 billion yen, or about 1,819 million US dollars. The largest principal amount is the three-year 169 billion yen senior notes with an annual interest rate of 0.974%. Based on data from this batch of bonds, Caihua estimates that the total annual interest rate is about 3.471 billion yen, or about 22.29 million US dollars, with an average annual interest rate of only 1.225%.$Berkshire Hathaway-A (BRK.A.US)$In terms of cash holdings of hundreds of billions of dollars, such interest expenses are not a problem at all. The key point is that Berkshire can use this borrowed capital to earn much higher returns than this cost. The yield on risk-free US Treasury bonds alone is far higher than this rate. Ycharts data shows that the current US 1-year treasury note interest rate is 5.21%, which means Berkshire can earn at least 399 basis points of interest spread from it, not counting the benefits of a further decline in the yen exchange rate.

This is exactly the investment logic of the “stock god.”

Therefore, the smartest investment strategy is not to maximize risk and return when the wind is high; rather, when the wind is calm and quiet, it is to gain early insight into future macroeconomic trends to ensure stable returns without risk. This concept hopes to help investors who are at the crossroads of capital markets and are confused.

Editor/Somer