Comprehensive brokerage China, Wall Street news, etc.

On the evening of April 25, Beijing time, the market was shocked by two major data reports disclosed by the US. First, according to data released by the US Department of Commerce, US real GDP in the first quarter increased by 1.6% over the initial quarterly period, far less than the 2.5% expected by the market, and a sharp slowdown from 3.4% in the fourth quarter of last year.

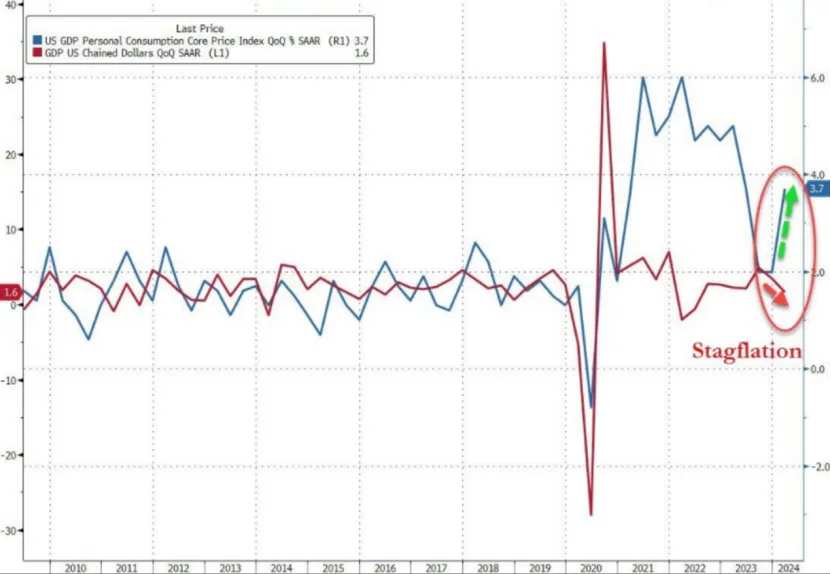

Second, the initial value of the US core PCE price index for the first quarter after seasonal adjustment was 3.7%, estimated at 3.4%, and the previous value was 2.0%. This is the first month-on-month acceleration in a year. After the data was released, the interest rate swap market believes that the Federal Reserve will not start cutting interest rates until December this year, not November.

Faced with unexpected “collapse” in US economic growth and stubborn core inflation, the market is worried, and the risk of US stagflation seems to be increasing. Affected by this, the three major US stock indices opened sharply lower. The NASDAQ plummeted 2.1%, the S&P 500 index fell 1.41%, and the Dow fell 1.39%. The European market also collectively dived. The European Stoxx 600 index fell 1% to the lowest point in the day; indices from Germany, France, Italy and other countries fell more than 1%.

Currently, another risk point in global financial markets may come from a strong dollar. The US dollar index has continued to rise due to the delay in interest rate cuts expected from the Federal Reserve, and has now risen to its highest point since early November last year. According to Invesco Asset Management's regression analysis, for every 1% increase in the US dollar index, the monthly return on the MSCI global (excluding the US) stock index falls by 0.2%.

Black swan raid

On the evening of April 25, Beijing time, data released by the US Department of Commerce showed that US real GDP in the first quarter grew 1.6% from the initial quarterly quarter, far short of the 2.5% expected by the market, and a sharp drop from 3.4% in the fourth quarter of last year.

According to the data, the GDP-weighted price index for the first quarter of this year was 3.1%, higher than the forecast of 3.0%, almost double that of 1.6% in the fourth quarter.

Unlike other countries, the US uses the annualized quarterly rate of real GDP as the most common indicator for measuring economic growth, and believes that it better reflects economic trends.

After the data was released, US President Joe Biden issued a statement saying that the US GDP report showed steady growth, but more work needed to be done.

Analysts believe that growth slowed significantly in the first quarter due to the increase in US inflation and the cooling of consumer and government spending.

Among them, consumer spending increased by 2.5%, lower than the 3.3% increase in the fourth quarter. Fixed investment and government spending at the state and local levels helped keep GDP positive this quarter, while falling private inventory investments and rising imports had a negative impact.

At the same time, the inflation index that the Federal Reserve is most concerned about is also sending a major negative signal.

According to the newly released quarterly inflation data, personal consumption expenditure (PCE) annualized quarterly increased 2.5% from the initial value of 3.3%, and fell short of the expected 3%; the core PCE price index, which does not include food and energy, grew 3.7% quarterly, exceeding expectations by 3.4%, almost double the previous value of 2%, for the first time in a year.

Inflation rebounded sharply in the first quarter. Excluding housing and energy, inflation in the service sector rose 5.1%, almost double the growth rate of the previous quarter.

This means that the risk of core inflation in the US is once again rising.

Currently, the market is nervous about the state of monetary policy and when the Federal Reserve will start cutting interest rates. As inflation remains high, investors have to adjust their views on when the Federal Reserve will begin easing.

After the data was released, the swap market is no longer fully priced and the Federal Reserve will cut interest rates before December this year. Furthermore, traders expect the Federal Reserve's first rate cut to be postponed until December. Interest rate swap traders now expect that the Federal Reserve will only cut interest rates by about 35 basis points for the full year of 2024, far lower than the forecast at the beginning of the year. At that time, it was expected to cut interest rates by 25 basis points more than six times this year.

Affected by this, the three major US stock indices opened sharply lower. The NASDAQ plummeted 2.1%, the S&P 500 index fell 1.41%, and the Dow fell 1.39%. At the beginning of the US stock market, Meta once plummeted by more than 16%, while Microsoft, Google, and Amazon all plummeted by more than 4%.

The European market also collectively dived. The European Stoxx 600 index fell 1% to the lowest point in the day; indices from Germany, France, Italy and other countries fell more than 1%.

The US bond market also experienced a wave of sell-offs. Among them, the yield on 2-year treasury bonds rose to 5.018%, the highest level since November 14 last year; the yield on 10-year treasury bonds rose to 4.70%, the highest level since November 2; and the yield on 30-year US bonds rose to 4.81%, a new high since November 9 last year.

Affected by the data, the US dollar strengthened again, and the US dollar index rose by nearly 20 points in the short term, and is approaching 106.

According to the schedule, the Federal Reserve will hold a meeting next week. The market is expected to keep interest rates high for 20 years. Traders will analyze Federal Reserve Chairman Powell's remarks to find the latest clues about the easing policy.

Risks from the US dollar

Currently, another risk point in global financial markets may come from a strong dollar.

Recently, the US dollar index has continued to rise. It has now risen to its highest point since early November last year, and remains around 106. Since this year, the US dollar index has accumulated a cumulative increase of more than 4%.

According to Invesco Asset Management's regression analysis, for every 1% increase in the US dollar index, the monthly return on the MSCI global (excluding the US) stock index falls by 0.2%.

The currencies of Asian countries, including Japan, South Korea, and Indonesia, are under tremendous depreciation pressure. Among them, the exchange rate of the yen against the US dollar has now fallen below 155, a new low since June 1990.

The market is worried that under tremendous depreciation pressure, the Bank of Japan may “air attack” the market. The Bank of Japan will announce its latest monetary policy decision on Friday (April 26), and the market expects the Bank of Japan to keep interest rates stable.

Currently, yen traders are waiting with bated breath, ready to respond to possible market intervention and changes in central bank policy at any time to prepare for the September 2022 scene to be repeated. At the time, the Bank of Japan's decision to ease monetary policy triggered a sharp reaction in the market.

According to a recent report by Japan's Jiji Press, the Bank of Japan will consider measures to reduce its government bond purchases.

Takeshi Yamaguchi, chief Japanese economist at Morgan Stanley, believes that Bank of Japan Governor Kazuo Ueda may make tougher remarks. The Bank of Japan is expected to raise interest rates by 15 basis points in July 2024, bringing the policy interest rate to 0.25%, and by another 25 basis points in January 2025.

UBS, on the other hand, pointed out in the report that the possibility that the Bank of Japan will raise interest rates in July cannot be ruled out, and with the further depreciation of the yen, this possibility has risen from 40% at the time to more than 45%. The Bank of Japan may also gradually reduce treasury bond purchases in June before raising interest rates.

UBS believes that with the weakening of the yen, the possibility of interest rate hikes in July has risen from 40% in March to over 45%.

What do analysts think?

Jeffrey Roach, chief economist at LPL Financial, stated:

The economy is likely to slow further in the next few quarters as consumer enthusiasm is likely to come to an end. Furthermore, as inflation continues to put more pressure on consumers, the savings rate is falling. We should expect inflation to ease somewhat this year as aggregate demand slows, but the Fed's 2% target is still far away.

Analyst Paul Davidson said:

At the beginning of this year, the economy slowed more than expected as weak corporate inventories and exports offset strong consumer spending and a boom in housing construction. The US Department of Commerce announced a 1.6% GDP growth for the first quarter, lower than the strong 4.1% increase in the second half of last year, and lower than market expectations.

The disappointing economic performance in the first quarter is likely to soften the views of Federal Reserve officials. Earlier, due to the accelerated rise in the consumer price index in the first quarter, Federal Reserve officials said they were not in a hurry to cut interest rates. However, some analysts still believe that the economy will weaken significantly later this year, while inflation will resume a rapid decline, thus enabling the Federal Reserve to cut interest rates several times.

Stuart Cole, chief macroeconomist at Equiti Capital, said:

The market reacted more to the PCE data than to the expected GDP data. Today's data is interesting. If the GDP data is confirmed in subsequent revisions, it will indicate that the US economy has finally begun to slow down under the monetary austerity policy implemented by the Federal Reserve, which in turn may lead to a decline in labor demand and downward pressure on wages. But the Federal Reserve is likely to pay more attention to PCE data, which shows that the process of returning inflation to target is still far from winning. Overall, today's data may further push the Federal Reserve to cut interest rates.

Brian Jacobson, chief economist at Annex Wealth Management, said:

GDP growth is lower than expected, but in terms of consumer spending, services are growing, but commodities are falling. Despite the overall weakness, households' domestic spending situation remains healthy. Unfortunately, spending on things like insurance and health care seems to be starting to crowd out spending on other areas. And the inflation data isn't encouraging. The annual increase in service prices has once again accelerated to 5.4%, which is a bit perplexing for the Federal Reserve. Economic growth has begun to slow, and inflation has rebounded. This is the conflict that central bankers are most concerned about.

Editor/Jeffrey