As of the evening of April 22, the 2024 quarterly reports for partial equity funds (partial share hybrid, balanced hybrid, and flexible allocation types in ordinary equity funds+hybrid open funds) have basically been disclosed.

China Merchants Fund's first-quarter position analysis showed that: the main board ratio rebounded, and the double share ratio declined; concentrated increases in stable dividends, offshore chains, and resource products sectors; in terms of industry allocation, increased inventory, new energy, consumer services, utilities, and reduced positions in pharmaceuticals and TMT; the tracks that increased positions mainly include CXO, aviation industry chain, lithium battery, liquor, photovoltaics, green electricity, etc. The tracks that reduced positions mainly included CXO, aviation industry chain, medical devices and services, industrial internet, domestic semiconductor substitution, AI, etc.; there is a big difference between fundraising and North China Capital in terms of industry preferences.

Let's take a look specifically:

In terms of sector configuration, the motherboard ratio rebounded, and the double innovation ratio declined. The allocation ratio of active equity public funds to the main board rebounded in the first quarter of 2024, and the ratio of the Double Innovation sector dropped sharply. Of the 2024Q1 active partial equity public fund holdings, the main board accounted for 72%, up 3.31% from the previous period; GEM accounted for 17.74%, down 1.39% from the previous period; and heavy stocks on the Science and Technology Innovation Board accounted for 9.84%, down 1.91% from the previous period.

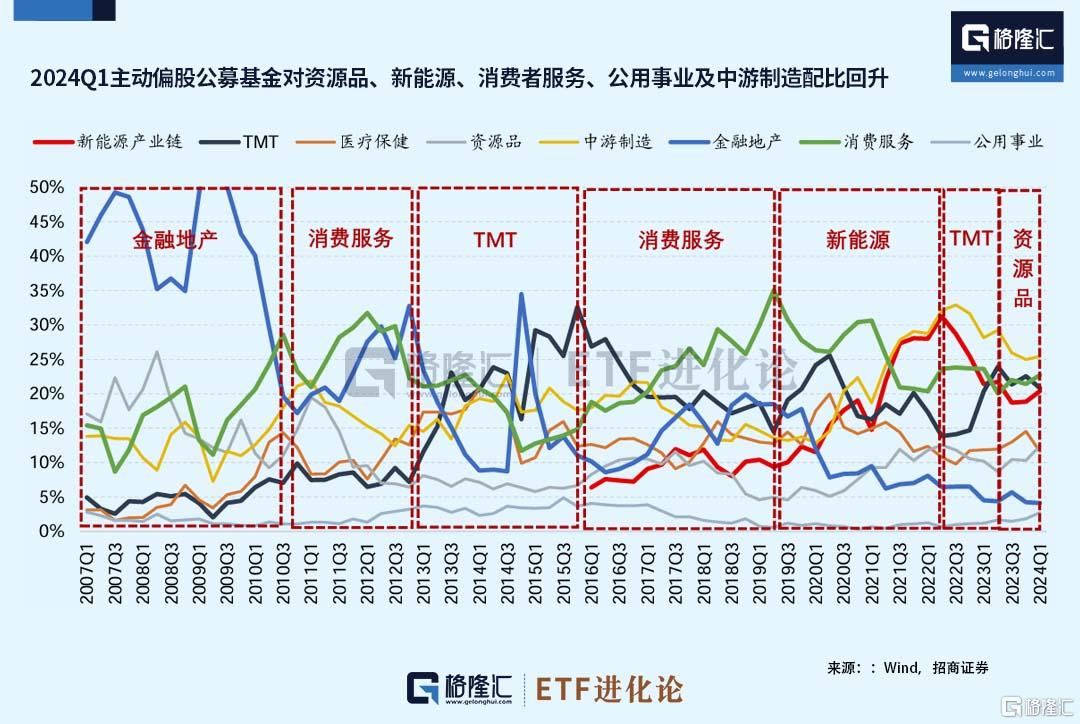

In major industries, the ratio of active partial equity public funds to resources, new energy, consumer services, and utilities rebounded in the first quarter of 2024, while the ratio of pharmaceuticals, TMT, and financial real estate declined.

The ratio rebounded in the sector. The ratio of resource products was 12.4%, up 2.11% from the previous period, and was 97.7% in the past ten years. The ratio of new energy sources was 20.4%, up 1.53% from the previous period, and 71.9% in the past ten years. The consumer service ratio was 22.7%, up 1.31% from the previous period, and 50% in the past ten years. The utility ratio was 2.7%, up 0.88% from the previous period, to 63.6% in the past ten years. The midstream manufacturing ratio was 25.4%, up 0.45% from the previous period, or 79.5% in the past ten years.

In the sector where the ratio declined, the pharmaceutical ratio fell 11.6%, down 2.92% from the previous period, to 18.2% in the past ten years; the TMT ratio was 20.8%, down 1.74% from the previous period, to 61.4% in the past ten years; and the financial real estate ratio was 4.1%, down 0.12% from the previous period.

The track in Kakura mainly includes mid-range specials, energy storage, lithium batteries, liquor, photovoltaics, green electricity, etc. The main tracks for reducing positions include CXO, the aviation industry chain, medical devices and services, the industrial Internet, domestic semiconductor substitution, AI, etc.

Judging from the first quarter fund position adjustment ideas, there are roughly three ideas:

The first is to lay out a stable dividend section.Increase coal mining, electricity, major state-owned banks, railways and highways, etc. Sectors such as coal, electricity, railways and highways have high dividends and low fluctuations, have abundant free cash flow, and have strong defensive properties. The fundamentals of large state-owned banks are relatively stable, static PB valuations are relatively low, and large banks have an advantage in debt costs and high average dividend rates.

The second is to lay out the offshore chain sector. With the gradual recovery of overseas demand, the export chain is relatively prosperous, and some overseas sectors such as white goods, light industry, and construction machinery have benefited. The export value increased 1.5% year-on-year in the first quarter, significantly higher than -4.65% at the end of 2023. Although the growth rate of orders placed in March turned negative due to the influence of the high base figure, there is still an improving trend when looking at the manufacturing PMI New Export Orders Index. Against the backdrop of a recovery in global manufacturing and recovery of overseas inventories, exports are expected to remain an important direction for improving the economy.

The third is to lay out the resource products section. Supply is expected to shrink, and prices for industrial metals such as copper and aluminum, which have low inventory levels, have increased. The intrinsic value of the US dollar continues to depreciate due to overspending of US debt. Demand for gold purchases by central banks is strong. Combined with geographical conflicts, the safe-haven value of precious metals is highlighted, and prices of precious metals such as gold have risen sharply. Global pricing and commodity prices have strengthened, and the A-share upstream resources sector is also favored by public funds.

In the first quarter of 2024, public funds and North China Capital had major differences in industry preferences. The industries that agreed to make net purchases include banking, non-ferrous metals, household appliances, utilities, communications, transportation, etc.; they also sold pharmaceuticals, computers, machinery and equipment, social services, steel, construction materials, etc. NorthThe differences between capital and public funds mainly focus on food and beverage, electronics, national defense and military industry, non-bank finance, light industry manufacturing, media, etc.

Most fund managers expressed optimism about the upcoming market.

Director Xing Quan said that various signs indicate that the steady upward trend in the domestic economy has been consolidated; although the index continued to rise after the Spring Festival, judging from the horizontal and vertical comparison of valuations, the current valuation of the A-share market still has a strong price/performance ratio, and we are optimistic about the performance of the A-share market.

Looking forward to the future market, Huatai Berry Dong Chen is still worth looking forward to. Although some traditional sectors are still facing the pain of economic transformation, the rapid development of emerging sectors cannot be ignored as a driving force for the overall economy, and the overall economic data is performing well. The momentum of subsequent policies in the direction of “new quality productivity” is expected to drive economic transformation and further deepening development, thus creating more opportunities for the stock market.

Harvest Zhang Jintao and Hu Yufei believe that the market performance for the whole of 2024 should be better than the past two years. In terms of investment direction, commodity companies with stable demand, tight supply, and global pricing are still important allocation directions.

E-Fangda Zhang Kun pointed out that judging from the stock asset performance of long-term treasury bonds and bond-like bonds, the market's risk appetite has been reduced to a very low level.