① Bank of Tianjin's customer deposits in the first quarter was RMB 446.678 billion, a decrease of RMB 4.08 billion from the beginning of the year, or 0.89%. ② Bank of Tianjin's average interest rate on customer deposits in the first quarter decreased by 22 basis points compared to 2023, which is a significant acceleration from last year's decline of 7 basis points. ③ Judging from the banks that have already disclosed their quarterly reports, there are different ways for each company to deal with the pressure of interest spreads.

Financial Services Association, April 23 (Reporter Liang Kezhi) Under the pressure of interest spreads, some banks finally said “no” to high-cost deposits, making heavy pressure drop adjustments, and even affecting the total deposit size in stages.

Yesterday evening, the Bank of Tianjin released its first quarter operating results. The data showed that the bank's total assets were RMB 871,117 billion, up 3.61% from the beginning of the year; of these, the amount of customer loans and advances was RMB 432.241 billion, up 9.15% from the beginning of the year. Total liabilities were RMB 804.656 billion, up 3.73% from the beginning of the year.

It is particularly noteworthy that Bank of Tianjin's customer deposits in the first quarter was RMB 446.678 billion, down RMB 4.08 billion from the beginning of the year, or 0.89%. A Financial Services Association reporter noticed that among the A-share and H-share listed banks currently issuing quarterly reports, Bank of Tianjin is the only bank whose deposits at the end of the first quarter declined compared to the beginning of the year.

In response, the Bank of Tianjin said that the main reason is that the bank continues to reduce the pressure on high-cost deposits. The average interest rate on customer deposits fell by 22 basis points compared to 2023, which affected the growth of various deposits to a certain extent.

In fact, before that, Bank of Tianjin had just won a “deposit attack.” According to the Bank of Tianjin's 2023 annual report, current customer deposits were 45.7 billion yuan, up 13.3% from 397.8 billion yuan at the end of 2022. Management said at the time that by adhering to the concept of deposit execution, fighting a good deposit campaign, compacting the entire bank's responsibility to collect and increase savings, and playing a role in performance evaluation, the scale of deposits has increased rapidly.

On April 22, a creditor from the Guangzhou branch of a stock bank told the Financial Association reporter that some banks are quite aggressive at the end of the year, and may reduce the pressure on some inflated deposits in the first quarter. However, under normal circumstances, pressure does not drop to negative growth.

The debt structure began to be adjusted last year, and the decline in interest rates accelerated in the first quarter

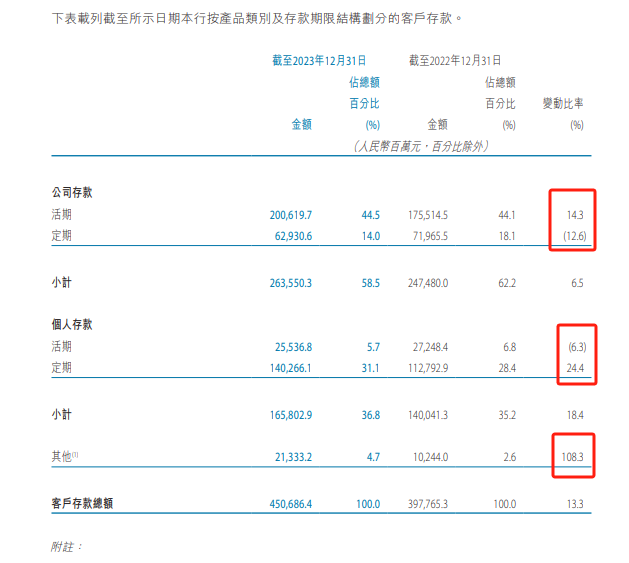

In the 2023 annual report, Yu Jianzhong, chairman of the Bank of Tianjin, said that in 2023, the bank's net interest spread was 1.75%, and the customer deposit interest rate was 2.89%, down 7 basis points from the previous year. Under the premise of effectively reducing high-cost deposits, customer deposits were 45.7 billion yuan, up 13.3% from 397.8 billion at the end of 2022. Public deposits and personal deposits increased 6.5% and 18.4% respectively.

Specifically, the Bank of Tianjin grew the most at the end of last year in corporate demand deposits and personal time deposits, which increased by 14.3% and 24.3% respectively. At the same time, “other deposits”, mainly security deposit, payable remittance and temporary deposit, reached 108.3%. It shows that there is holding pressure on its deposits, and the bank's deposit at the end of last year was characterized by regular savings and a large share of the public interest period.

Regarding the negative growth in deposit deposits in the first quarter, the Bank of Tianjin said that the main reason was that the bank continued to reduce high-cost deposits. The average interest rate on customer deposits fell 22 basis points compared to 2023, which affected the growth of various deposits to a certain extent.

A Financial Services Association reporter noticed that the Bank of Tianjin's quarterly report did not disclose the average interest rate index for customer deposits. However, based on last year's 2.89% level, the average interest rate level for the first quarter fell by 22 basis points to 2.67%. The rate of decline is much faster than last year.

The root cause is still pressure on interest spreads

According to the first quarterly report, Bank of Tianjin's loans increased by 9.15% and assets increased by 3.61%, but the bank's net profit only increased by 1.63%. Like many listed banks, it was pressured by interest spreads, and there was a situation where revenue growth did not increase profits.

The deposit strategies of Ping An Bank and Bank of Hangzhou, which recently released quarterly reports, have changed to varying degrees.

According to Ping An Bank's quarterly report data, the principal amount of deposits absorbed at the end of March was 3.45 trillion yuan, a slight increase of 1.3% from the end of last year. However, corporate deposits fell slightly by 0.1% from the end of last year and recorded 2.20 trillion yuan. Had it not been driven by a 3.9% increase in personal loans, Ping An Bank deposits in the first quarter might also have an overall negative growth.

In a quarterly report, Ping An Bank stated that it mainly boosts the scale of retail deposits by enabling AUM to drive current deposits, expand deposit business scenarios, and enhance dropshipping service capabilities. According to the data, the average daily balance of personal deposits in the first quarter was 1.23 trillion yuan, an increase of 14.2% over the previous year; the dropshipping and batch business brought in deposits of 313.5 billion yuan, an increase of 4.8% over the end of last year.

In terms of cost, Ping An Bank's average deposit cost rate at the end of March was 2.22%, slightly higher than 2.19% at the end of December last year. It is worth noting that the average cost rate of corporate deposits at the end of March was higher than at the end of December last year, at 2.15% and 2.12%, respectively. Contrary to the declining trend in personal deposits, it shows that larger corporate deposits are under greater maintenance pressure.

This is similar to the situation at the Bank of Tianjin. Although the regularization of personal deposits will increase costs, the total volume is growing steadily, and most of the variables are corporate deposits.

Ji Guangheng, Governor of Ping An Bank, once confessed, “In 2024, Ping An Bank's pressure on public business is on deposits, and the pressure on retail business is on loans. We need mutual help for public and retail businesses. We hope that the public business can rise above the top and seek a resuscitation for retail.”

Ping An Bank said that the average cost rate for absorbing deposits in the first quarter increased by 2 basis points year-on-year, mainly due to continued high interest rates in the foreign currency market and the regularization of RMB deposits. The next step will be to strengthen the control of high-cost deposit products, promote the deposit of low-cost settlement deposits, and optimize deposit costs.