整体来看,本次变化针对港股市场近年来所面临的新变化和新形势,尤其是市场流动性不足,融资吸引力下降以及内地投资者可投资范围有限等问题,有的放矢的提供应对措施。

整体来看,本次变化针对港股市场近年来所面临的新变化和新形势,尤其是市场流动性不足,融资吸引力下降以及内地投资者可投资范围有限等问题,有的放矢的提供应对措施。Source: Zhongjin Dim Sum

CICC Research

On the evening of April 19, Beijing time, the China Securities Regulatory Commission's website published the “5 Capital Market Cooperation Measures with Hong Kong” [1] (hereinafter referred to as the “Cooperation Measures”) to further expand the Shanghai-Shenzhen-Hong Kong Stock Connect mechanism, consolidate Hong Kong's position as an international financial center, and jointly promote the collaborative development of capital markets between the two places. The cooperation measures specifically include 5 items, namely 1) easing the scope of eligible products for stock ETFs under the Shanghai Shenzhen Hong Kong Stock Connect; 2) incorporating REITs into the Shanghai, Shenzhen, and Hong Kong Stock Connect; 3) supporting the integration of RMB stock trading counters into Hong Kong Stock Connect; 4) optimizing mutual fund recognition arrangements; and 5) supporting leading enterprises in the mainland industry to go public in Hong Kong. This article will be interpreted from the three perspectives of market strategy, the financial industry, and the REITs market.

Strategy: Optimizing connectivity mechanisms to consolidate and enhance Hong Kong's position as a financial center

Overall, this change provides targeted countermeasures in response to the new changes and situations faced by the Hong Kong stock market in recent years, particularly problems such as insufficient market liquidity, declining financing attractiveness, and limited scope for mainland investors to invest. In the medium to long term, it will not only help diversify the variety of trading products and provide more convenience and choices for foreign and mainland investors, but also help promote further integration of the capital markets of the two places, help internationalize the RMB, and strengthen Hong Kong's position as a financial center. Based on the latest developments, we have sorted out the specific content mentioned in this “Cooperation Measures” and interpreted the possible impact.

Overall, this change provides targeted countermeasures in response to the new changes and situations faced by the Hong Kong stock market in recent years, particularly problems such as insufficient market liquidity, declining financing attractiveness, and limited scope for mainland investors to invest. In the medium to long term, it will not only help diversify the variety of trading products and provide more convenience and choices for foreign and mainland investors, but also help promote further integration of the capital markets of the two places, help internationalize the RMB, and strengthen Hong Kong's position as a financial center. Based on the latest developments, we have sorted out the specific content mentioned in this “Cooperation Measures” and interpreted the possible impact.

Measure 1: Relaxate the scope of eligible products for stock ETFs under the Shanghai-Shenzhen-Hong Kong Stock Connect to further facilitate the allocation of Chinese assets by foreign investors

On July 4, 2022, connectivity was officially included in ETF trading, becoming another landmark event under the continuous optimization of the interconnection mechanism. Under current regulations, the screening for inclusion in interconnected products is mainly based on fund size and tracking indices, mainly stocks subject to connectivity, etc. The details include: 1) ETFs must be listed for 6 months and 1 year after tracking the underlying index; 2) Mainland ETFs must be denominated in RMB, and the average daily asset size for the past 6 months is not less than 1.5 billion yuan; 3) stocks listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange account for no less than 90% of the underlying index, and Land Stock Connect shares account for no less than 80% of the weight. The Hong Kong Stock Connect ETF inclusion requirements are similar. In terms of market capitalization requirements, the average daily asset size for the last 6 months is not less than HK$1.7 billion. The constituent securities are mainly Hong Kong Stock Exchange's, while synthetic ETFs, leveraged and inverse products are not included.

This measure relaxes the scale threshold for inclusion and withdrawal and weight requirements for tracking indices. On the Shanghai Stock Connect side: 1) The inclusion scale threshold was adjusted from the average daily asset size of not less than 1.5 billion yuan to no less than 500 million yuan in the previous 6 months; 2) the weight of stocks listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange in the components of the tracked index was reduced from no less than 90% to no less than 60%; 3) The weight of China Stock Exchange in the tracked index components dropped from no less than 80% to no less than 60%; 4) The average daily asset size for the past 6 months was adjusted to no less than 400 billion yuan; 4) The average daily asset size of the Shanghai Stock Exchange was adjusted to no less than 4 billion yuan in the previous 6 months; The weights of Land Stock Connect and Land Stock Connect have been lower than before, respectively 85% and 70%, both down to 55%. On the Hong Kong Stock Connect side: 1) The inclusion scale threshold was adjusted from no less than HK$1.7 billion to no less than HK$550 million; 2) the share weight of stocks listed on the Stock Exchange in the tracked index components was reduced from no less than 90% before to no less than 60%; 3) In terms of the share weight share of Hong Kong Stock Connect, the indices that were previously tracked were Hang Seng Index, Hang Seng China Enterprise Index, Hang Seng Technology Index, or Hang Seng Hong Kong Listed Biotech Index, whose constituent securities account for at least 70%; The share weight of Hong Kong Stock Connect shall not be less than 80%; After the adjustment, the weight ratio was uniformly adjusted to no less than 60%. 4) Exclusion aspect: The transfer scale threshold was adjusted from less than HK$1.2 billion to less than HK$450 million; the transfer scale ratio was uniformly adjusted to not less than 55%.

According to the above conditions, based on the current interconnected ETFs (141 A shares and 8 Hong Kong stocks), we will screen about 78 A shares and 8 Hong Kong stock ETF products or meet the inclusion criteria. The corresponding fund sizes are RMB 85.2 billion and HK$25.5 billion respectively. The average daily turnover for the past three months was RMB 5.56 billion and HK$20.5 million, respectively.

Overall, the further expansion of connected ETFs will help facilitate international investors, especially allocative capital, to allocate China through passive indices. Furthermore, according to our estimates, most of the new A-share ETFs that are expected to be included this time are industry-themed funds, which are in line with China's long-term development themes (chips, cloud computing, photovoltaics, state-owned enterprises, dividends, etc.), and are also conducive to attracting overseas investors to lay out the A-share industry segments and popular tracks in detail. Compared to A-shares, there are only 8 new eligible Hong Kong stock ETFs, so the overall impact on Hong Kong stocks is relatively limited in the short term, but from a long-term perspective, the expansion of connected ETFs marks the continued deepening of financial connectivity between Hong Kong and the mainland, and helps support the construction of the Hong Kong International Asset Management Center (“Further Expansion of Connectivity into ETFs”).

Measure 2: Integrate REITs into the Shanghai-Shenzhen-Hong Kong Stock Connect to further enrich investment categories

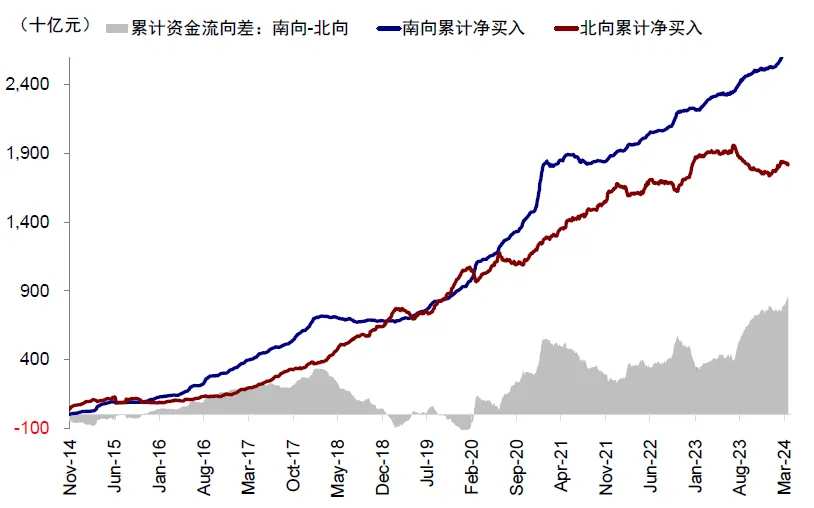

Since the opening of the Shanghai-Hong Kong Stock Connect and the Shenzhen-Hong Kong Stock Connect at the end of 2014 and the end of 2015, the cumulative inflow volume to the north and south has reached 1.8 trillion yuan and 2.7 trillion yuan. The overall operation is smooth and smooth, and the two-way scale and transaction activity have continued to increase (Chart 2 to Chart 3). Since its launch, the Shanghai-Shenzhen-Hong Kong Stock Connect mechanism has continued to be improved and optimized, and the scope of transactions has continued to expand: 1) the total amount limit was lifted in 2016; 2) the daily quota for the northbound and southbound daily quota was increased by 3 times in 2018; 3) Hong Kong listed companies with the same shares and different rights were included in the Hong Kong Stock Connect scope in February 2021; 5) Interconnect was officially included in the ETF in July 2022; and 6) Foreign companies were included for the first time in March 2023 (Chart 1).

Chart 1: Since its launch in 2014, the interconnection mechanism has continued to be optimized. This plan includes REITs and RMB trading counters

Chart 2: Since the launch of connectivity in 2014, the cumulative inflows to the north and south have reached 1.8 trillion yuan and 2.7 trillion yuan

Chart 3: Continued increase in terms of position share and trading activity

The inclusion of REITs this time is a further expansion of the scope of connectivity investments, further enriching the investment categories. In terms of the number of optional products, as of April 19, there were 36 REITs products on the Shanghai and Shenzhen Exchange and 11 REITs products on the Hong Kong Stock Exchange; in terms of overall scale, the total closing market value of REITs products on the Shanghai and Shenzhen Exchange as of April 19 was about RMB 102 billion, and the total closing market value of REITs products listed on the Hong Kong Stock Exchange was about HK$110 billion (Chart 4 to Chart 5).

Chart 4: Currently 36 REITs are listed on the Shanghai and Shenzhen Exchange

Note: The data is as of the close of April 19

Chart 5: Currently 11 REITs are listed on the Hong Kong Stock Exchange

Note: The data is as of the close of April 19

In the current macro environment, REITs, as a typical example of stable dividend assets, also help increase their appeal to dividend investors. According to CICC Real Estate Group estimates, the pricing of mainland REITs is anchored in RMB capital costs. The long-term return on investment may be 6-7% (between stocks and bonds), and the cash return represented by dividends accounts for the main part. At the same time, the recent demand for allocating high dividends to Hong Kong stocks is clearly reflected in the context of market fluctuations and the overall decline in return on investment. For REITs currently listed on the Hong Kong Stock Exchange, most TTM dividend rates can reach 10% or more, so we believe that after being included in connectivity this time, it is expected that more mainland capital will be allocated from the perspective of dividend attractiveness (”The value of high-dividend investment under the new macro situation”).

Based on the allocation requirements of inland investors for high dividends, we believe that Hong Kong REITs will show higher investment value after RMB capital gains more pricing power.

Measure 3: Support the integration of RMB stock trading counters into Hong Kong Stock Connect, help long-term capital allocate high-dividend assets for Hong Kong stocks, and help internationalize RMB

The Hong Kong Stock Exchange's “HKD-RMB Dual Counter Model” was officially launched on June 19, 2023. Under the dual counter model, eligible securities have both HKD and RMB trading counters. Investors can trade and settle in both HKD and RMB currencies respectively, and can trade across counters between HKD counters and RMB counters (Chart 7). Hong Kong stock companies that meet market value and liquidity requirements can set up additional RMB counters. Up to now, the Hong Kong Stock Exchange has approved 24 listed companies to set up RMB counters (Chart 6), mostly for blue-chip stocks and Hong Kong Stock Exchange (“”What you need to know about the “double counter” of Hong Kong stocks”). The Hong Kong stock dual counter model is currently mainly used by local or overseas investors in Hong Kong, so trading activity is low. Currently, the average daily turnover of RMB counters accounts for less than 0.5% of HKD counter turnover, and the current average price difference between RMB counters and HKD counters under the dual-counter bookmaker system is less than 0.5%. In addition, the double counter bookmaker mechanism provides continuous quotes for double counter stock buyers and sellers to inject liquidity into the market. At the same time, bookmakers trade across counters when there is a price difference between the two counters, reducing the price difference between the two counters.

Chart 6: List of Eligible Dual Counter Securities

Chart 7: HKD-RMB Dual Counter Model

Previously, the RMB counter was mainly intended to provide investment targets directly denominated in RMB for RMB deposits overseas. After this adjustment, southbound capital can also directly purchase RMB over-the-counter Hong Kong Stock Exchange through the Shanghai-Hong Kong Stock Connect channel. For mainland southbound investors, the significance of this change is: 1) saving exchange transaction costs during the transaction; 2) However, they will still bear the loss of exchange rate fluctuations during the investment process, mainly because the daily price difference between the RMB counter and the Hong Kong dollar counter will be quickly smoothed out due to exchange rate fluctuations under the dual-counter bookmaker system, so changes in exchange rates will be reflected in stock price changes; 3) However, dividends during the holding period are directly paid in RMB, which can avoid this part of the exchange cost. Investors do not need to exchange HKD for RMB when receiving dividends. Therefore, in the short term, due to the small scope of initial RMB counters (24 companies), light transactions (accounting for less than 0.5% of the HKD counter), and the inability to hedge against exchange rate fluctuations during the holding period, this will not cause much change at all in the early stages. However, for long-term value investors who prefer high dividends, such as funds such as social security insurance banks, etc., it will increase the attractiveness of this part of the investment and reduce the loss of dividends. In the long run, the continuous increase in the number of RMB counter targets and participants will help increase its transaction activity. This may attract more international investors to use RMB transactions, help consolidate Hong Kong's position as an offshore RMB center, and promote the internationalization of the RMB.

Measure 4: Optimize mutual fund recognition arrangements to enrich the diversified investment needs of mainland investors

Since July 1, 2015, the China Securities Regulatory Commission and the Hong Kong Securities Regulatory Commission have jointly launched mutual recognition of funds between the two places. Eligible funds can be sold in each other's markets. Currently, it is stipulated that the sales scale of mutual recognition funds in the counterparty market must not exceed 50% of the total assets, and when the sales share of mutual recognition funds in the other party market is close to the upper limit of 50%, necessary measures must be taken to control them. If mutual recognition funds passively exceed the bid due to large redemptions in the local market, the fund also needs to suspend sales in the other party's market. Furthermore, Hong Kong Mutual Recognition Fund Managers cannot delegate investment management functions to investment institutions operating outside Hong Kong.

As of April 19, 48 Mainland Mutual Recognition Funds have been registered and 6 are being approved; 117 Hong Kong Mutual Recognition Funds have been registered. Although the current average annualized return of Mainland Mutual Recognition Funds is 2.8%, which is higher than -1.4% of Hong Kong Mutual Recognition Funds, the sales volume of Mainland Mutual Recognition Funds is less than 5% of Hong Kong Mutual Recognition Funds. As of the end of February 2024, the cumulative net subscription amount of the Hong Kong Mutual Recognition Fund was RMB 21.44 billion, far higher than the Mainland Mutual Recognition Fund's RMB 980 million (Chart 8). Hong Kong mutual recognition funds have a high level of activity. On the one hand, due to the diversification of their product types, the number of bonds, equities, and hybrid funds account for 59.0%, 36.7%, and 4.3% respectively. On the other hand, since Hong Kong mutual recognition funds do not only invest in the Hong Kong market, the main investment areas of more than 40% of Hong Kong mutual recognition funds are the United States, Indonesia, Japan, South Korea, India, etc. (Chart 9). Compared to connected Hong Kong stock ETF products, which are mainly based on the Hong Kong Stock Exchange Standard and are not actively traded, the Hong Kong Mutual Recognition Fund has a wider variety of products and strategies. In particular, overseas assets are attractive to mainland investors, which has led to an overall increase in sales of the Hong Kong Mutual Recognition Fund since its opening.

Chart 8: Cumulative net subscription amount for mutual recognition funds between the two places

Chart 9: Mutual Fund Types and Investment Regions in Hong Kong

The measure aims to promote a moderate relaxation of restrictions on the sales ratio of mutual recognition funds in each other's market. Of the 47 Mainland mutual recognition funds registered as of April 19, 21 were suspended or suspended for large purchases, partly due to a sales share close to or above 50% in Hong Kong. If this ratio is later relaxed, these funds may resume normal subscription; secondly, to allow the transfer of investment management functions of Hong Kong Mutual Recognition Fund to overseas asset management agencies in the same group as the manager, which previously did not allow investment institutions operating outside Hong Kong to obtain investment management functions. Under this influence, we believe that the asset allocation channels for investors from the two regions are expected to continue to expand and explore new investment directions; at the same time, mainland investors will enter overseas markets through the Hong Kong Mutual Recognition Fund, improving the accessibility of cross-border investment channels and enriching the diversified investment needs of mainland investors.

Measure 5: Support leading mainland enterprises to go public in Hong Kong, which will help strengthen Hong Kong's position as a financial center

Since 2018, a series of listing system reforms in Hong Kong have significantly improved the Hong Kong stock ecosystem: 1) In April 2018, the Hong Kong Stock Exchange reformed the listing system to attract new economy companies to go public in Hong Kong with three major measures, including allowing unprofitable biotech companies to go public in Hong Kong, opening a new chapter for the Hong Kong market. 2) The Hong Kong Stock Exchange then proposed easing the secondary listing threshold again in 2021, and officially implemented it in January 2022, welcoming the return of China Securities with a more open and inclusive mindset. 3) In October 2022, the Hong Kong Stock Exchange published the “Consultation Document on New Listing Rules for Special Technology Companies” and officially added Chapter 18C of the “Listing Rules” in March 2023 to set up new channels to attract more specialty technology companies to go public in Hong Kong (Chart 10).

Chart 10: Listing System Reform: Biotechnology, WVR, Secondary Listing → Optimizing Secondary Listing → Specialized Technology Listing

Meanwhile, on March 31, 2023, the new overseas issuance and listing filing regulations issued by the China Securities Regulatory Commission were officially implemented, and previous rules were systematically optimized, including unifying supervision to fill gaps, setting up negative lists to increase inclusiveness, and optimizing filing management processes (“Interpreting the New Overseas Listing Regulations for Domestic Companies”).

Affected by macroeconomic and market sluggish performance, the Hong Kong stock IPO market has also performed poorly in recent years. According to statistics from the Hong Kong Stock Exchange, only 73 IPOs were listed on the Hong Kong Stock Exchange in 2023, and the initial public offering was HK$46.29 billion, a decrease of 17 companies compared to 2022, a decrease of 55.8%. The number of listed companies in 2023 was about one-third of the 218 IPOs listed on the Hong Kong Stock Exchange in 2018 (Chart 11).

Chart 11: The Hong Kong Stock Exchange's IPOs have not performed well in recent years

This measure further supports leading enterprises in the mainland industry to go public in Hong Kong, and also shows support for Hong Kong to consolidate and enhance its status as an international financial center. We believe, on the one hand, that mainland enterprises use two markets and two resources to standardize their development, that overseas financing channels for domestic enterprises are further unblocked, that the capital market continues to be open at a high level, and that global investors will have more opportunities to share the dividends of China's economic development. As of April 18, out of 99 companies applying for overseas issuance of securities and listing filings (initial public offering and full circulation) with the China Securities Regulatory Commission, 72 have applied for listing on Hong Kong stocks, accounting for more than 70%. On the other hand, listing more mainland companies in Hong Kong will help optimize the structure of the Hong Kong stock market, attract more capital accumulation, form positive feedback from high-quality companies and capital, and further strengthen Hong Kong's position as a global financial center and RMB bridgehead. In the long run, Hong Kong is still one of the preferred destinations for mainland Chinese-funded enterprises, especially in the new economy sector, for listing and financing, and is also a link between international capital and Chinese assets (Chart 12).

Chart 12: The overall share of the “new economy” sector in Hong Kong stock market capitalization continues to rise

Finance: Five measures to strengthen Hong Kong's position as an international financial center

In line with the implementation of the new “National Nine Rules” on “adhering to a high level of institutional openness and security in the capital market and expanding and optimizing the cross-border interconnection mechanism of the capital market, etc.,” the Securities Regulatory Commission issued 5 capital market cooperation measures with Hong Kong on April 19 to help Hong Kong consolidate and enhance its status as an international financial center and promote the collaborative development of the two markets.

① Relieve the scope of eligible products for stock ETFs under the Shanghai-Shenzhen-Hong Kong Stock Connect and support the construction of the Hong Kong International Asset Management Center. This expansion of the target includes reducing the ETF size requirement and lowering the share weight requirement for tracking the underlying index, that is, the Shanghai Stock Connect ETF inclusion threshold was lowered from no less than 1.5 billion yuan to no less than 500 million yuan, the share weight of Shanghai and Shenzhen Stock Connect shares was not less than 60% of the underlying index constituent stocks, and the Hong Kong Stock Connect ETF inclusion threshold was reduced from HK$1.7 billion to no less than HK$550 million. The target index constituent stocks were reduced by no less than 60%, and the detailed requirements were lowered simultaneously ((See Chart 13); The relevant preparations for the two exchanges are expected to take about three months . ETF Connect was launched in July '22. As of April 20, the number of products included in Northbound and Southbound was 141 units/8 respectively, with a total market capitalization of 1,552.1 billion HKD/191.5 billion, respectively; the 1Q24 Southbound ETF ADT reached HK$1.68 billion, accounting for 5.4% of the total Southbound ADT /6.2% of the Hong Kong Stock Market ETF, and 1.08 billion yuan, accounting for 0.8% of the total Northbound ADT and 0.9% of the A-share market equity ETF. We estimate that this relaxation of standards is expected to add 78 northbound ETFs/corresponding fund size of 85.2 billion yuan, and 8 southbound ETFs/corresponding size of HK$25.5 billion. If we refer to the 1Q ETF penetration rate, the corresponding increase in northbound and southbound ADT is 140 million yuan/HK$3.3 million.

② Integrate REITs into the Shanghai-Shenzhen-Hong Kong Stock Connect and enrich the variety of Shanghai-Shenzhen-Hong Kong Stock Connect transactions. The first batch of A-share REITs was listed in June 2021. The asset composition is mainly infrastructure, with a total market value of $101.9 billion and a 2024 YTD ADT of $470 million; the first REITs on the Hong Kong Stock Exchange were listed in November 2005. The asset composition was mainly office/retail/hotels. As of April 20, the total number of listings was 11, with a total market value of HK$113.9 billion and HKD 2024YTD of 370 million. In the short term, due to the small overall turnover of REITs in the two regions, it is expected that the increase in market trading volume will be limited; in the medium to long term, the domestic REITs market has just progressed and there is still a lot of room for development in the future. Furthermore, following the ETF connection, the Shanghai Shenzhen Hong Kong Stock Exchange once again ushered in product category expansion, helping investors in the two places achieve diversified allocations.

③ Support the integration of RMB stock trading counters into Hong Kong Stock Connect and help internationalize RMB. The Hong Kong Stock Exchange officially launched the HKD-RMB dual counter model in June 23. Currently, 24 companies have set up RMB counters, which are limited to offshore RMB transactions; the total ADT of 24YTD RMB counters was RMB 53 million, accounting for only 0.2% of the HKD counter ADT during the same period (see Figure 15 for details). At present, the two exchanges and clearing houses have reached a preliminary agreement on the plan to include the RMB counter in Hong Kong Stock Connect. For investors going south, the RMB counter helps mitigate exchange risks and enhance the convenience of southbound transactions; since this year, southbound turnover has accounted for 15% of the Hong Kong market/ 7% of the position size. If launched in an orderly manner in the future, it may help increase RMB counter turnover.

④ Optimize mutual fund recognition arrangements to meet the diverse needs of investors in the two regions. In 2015, the two local securities regulatory councils jointly introduced mutual fund recognition. Eligible funds can be sold in each other's markets, and the maximum sales ratio is 50%. As of April 20, 2024, the number of registered Mainland Mutual Recognition Funds (issued by Mainland fund companies and sold in Hong Kong) was 54 and 117 Hong Kong Mutual Recognition Funds (issued by Hong Kong fund companies and sold in the Mainland); the cumulative sales of Mainland and Hong Kong Mutual Recognition Funds were 4.2 billion yuan and 102.3 billion yuan respectively, with net subscription amounts of 1 billion yuan and 21.4 billion yuan respectively. The development of Hong Kong Mutual Recognition Funds is relatively active. This time, the Securities Regulatory Commission “intends to promote a moderate relaxation of mutual recognition fund customer sales ratio restrictions and allow Hong Kong mutual recognition fund investment management functions to be transferred to overseas asset management agencies with managers”. We believe that the relevant measures will help improve the scale limit of SME and SME fund sales, and help Hong Kong Mutual Recognition Fund to give full play to the Group's comprehensive investment and research capabilities, and further enhance the appeal of mutual recognition funds.

⑤ Support leading enterprises in the mainland industry to go public in Hong Kong. Since the rules of the overseas listing filing management system were implemented in March last year, according to the Securities Regulatory Commission, 72 companies have now completed the filing of IPOs in Hong Kong (as of April 20, 2024), with unobstructed channels and sufficient projects. Meanwhile, based on Wind, as of April 20, the Hong Kong Stock Exchange had 89 projects lined up, 82 of which were mainland enterprises [2]. Supporting leading mainland enterprises to go public in Hong Kong not only helps enterprises make full use of the two markets and resources to achieve development, but also helps the Hong Kong Stock Exchange attract high-quality enterprises, improve market size and structure, and elevate the long-term growth center.

risks

The capital market fluctuates greatly.

Chart 13: Comparison between the “Shanghai Stock Exchange Shanghai-Hong Kong Stock Exchange Business Implementation Measures (Draft for Comments)” Stock ETF Interconnection Standards and the Original Standards

Chart 14: ETF Pass Monthly Trading Status

Chart 15: Current List of RMB Counter Companies and Transaction Status

Note: The data is as of April 20, 2024. The average daily turnover of RMB counters has been converted to HKD according to the 24-year average exchange rate

Figure 16: Current Mainland Mutual Recognition Fund Mechanism

Chart 17: Current customer sales of mutual recognition funds between the two places

REITs: Collaboration for Win-Win - A Brief Review of REITs Incorporating Connectivity for the First Time

On April 19, the China Securities Regulatory Commission announced 5 capital market cooperation measures with Hong Kong (hereinafter referred to as “cooperation measures”), officially incorporating REITs into the Shanghai-Shenzhen-Hong Kong Stock Connect.

Connectivity is beneficial to the development of both REITs markets. The mainland REITs market is still in the early stages of development, and the momentum of expansion is good, but there is still room for further enrichment and optimization of the investor structure. Among them, overseas investors are currently a relatively empty field. We believe that connectivity is expected to attract some overseas capital to invest in China's infrastructure assets. The Hong Kong REITs market has a history of development for nearly 20 years, but its overall size (total market value of about HK$110 billion as of April 19) and position falls short of mainstream Asia-Pacific REITs markets such as Singapore, Japan, and Australia. We believe that connectivity will help the Hong Kong market share the development dividends of the mainland market. In the future, it may attract some assets to be listed in Hong Kong, China, and if it can effectively expand the investor base, it will also have positive significance in promoting the development of asset securitization in Hong Kong, China. Overall, the current market capitalization of the two markets is relatively equal, and connectivity will enable them to take advantage of their own needs in future development and work together for a win-win situation. With the implementation of specific mechanisms in the future and the gradual deepening of investor awareness, we believe that both markets are expected to reap longer-term development benefits and push REITs as a major asset class to a level more suited to the size of the economy.

The asset structure and investment logic of the two places are different. The asset structure of the mainland market is mainly infrastructure. There are a large number of single securities (currently 35 projects listed), but the asset types are more diverse, so investors can be more flexible in portfolio allocation. What needs to be improved in the mainland market is that currently the size of single vouchers is still small, and it may need to be increased through normalized expansion in the future. The asset structure of the Hong Kong market is still dominated by traditional office, retail, and hotel businesses. The number of targets is limited (currently there are 11 listed REITs) and the concentration is high. For example, the Lingzhan Real Estate Fund single voucher accounts for about 70% of the total market value of REITs in Hong Kong, China. From an investment perspective, we believe that the pricing of mainland REITs is anchored in RMB capital costs. The long-term return on investment may be 6-7% (between stocks and bonds), of which the cash return represented by dividends accounts for the main part. In terms of valuation, we believe that mainland REITs as a whole are currently at a reasonable level. In the future, in the context where the equity market's high-dividend strategy may be further deepened, REITs, as an integral part of the high-dividend allocation, are expected to maintain the resilience of the valuation level. The operation of REITs in Hong Kong, China is greatly affected by the Chinese economy on the molecular side (level of return on assets), and is greatly affected by US dollar interest rates on the denominator side (at what dividend rate). Therefore, there is an endogenous molecular denominator cycle mismatch, and it may be necessary to pay more attention to the timing of investment. Currently, the overall REITs market in Hong Kong, China is still in a downward channel, but we believe that valuation already has a certain margin of safety. The long-term dimension, such as if the pricing power were to switch more to RMB, then it may currently be a reasonable window to focus on long-term allocation of high-quality assets.

risks

Exchange progress fell short of expectations; project fundamentals deteriorated; overseas interest rates remained high.

Figure 18: Summary of the basic situation of REITs in Hong Kong

Note: Figures are as of April 19, 2024

Chart 19: Trends in the REITs Market in Hong Kong, China

Note: 1) Based on January 2010 data, benchmark = 100; 2) Data frequency is monthly; 3) Data as of March 28, 2024

Chart 20: Stock and ETF Shanghai-Shenzhen-Hong Kong Stock Connect Rules Summary

[1] http://www.csrc.gov.cn/csrc/c100028/c7474875/content.shtml

[2] Statistics of companies with headquarters and office addresses based on iFind data

Editor/jayden