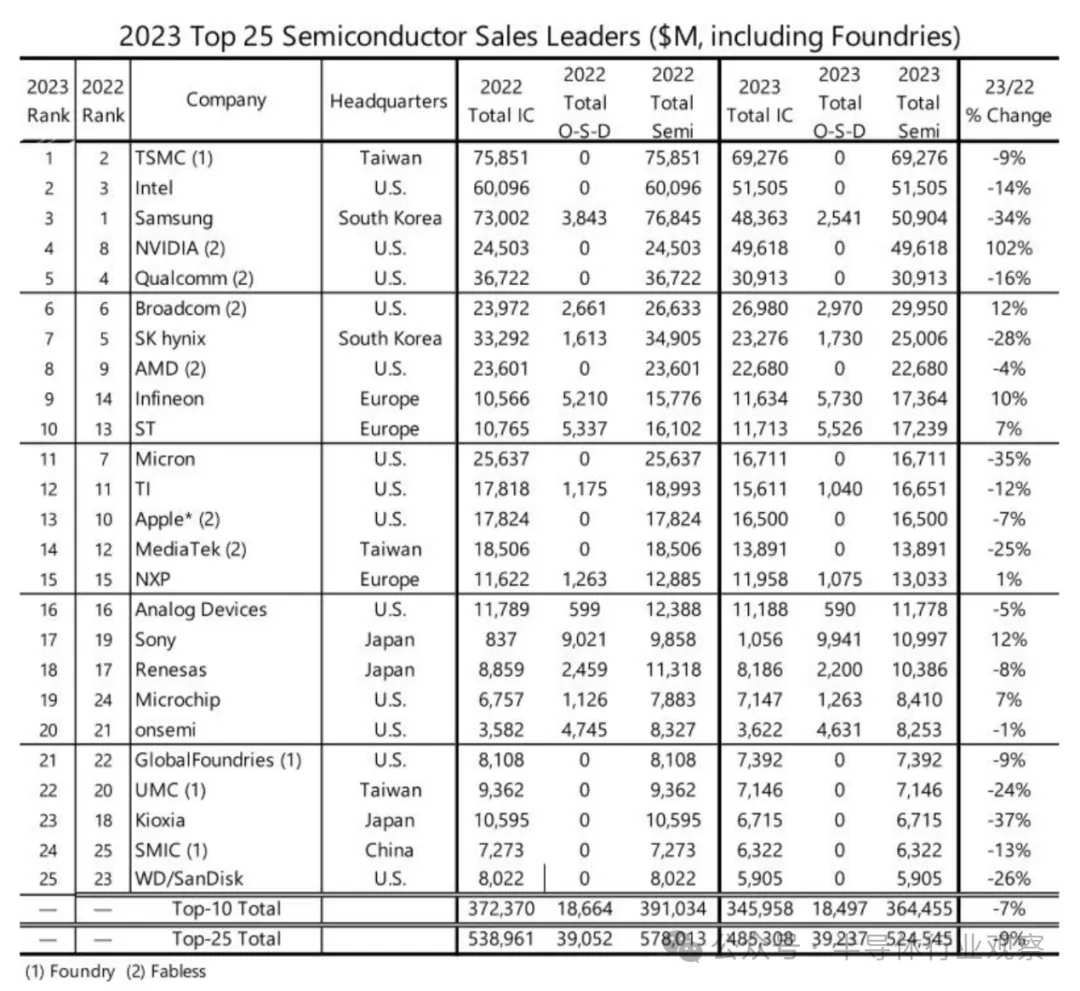

首先从总体营收上来看,与2022年相比,前25名公司的总营收有所下降,从2022年的5790亿美元减少到2023年的5245亿美元,减少约9%。前25名中营收最高额为692亿美元,第25名为590亿美元,前后约相差100亿美元。这也意味着前25名的最低销售额门槛。

首先从总体营收上来看,与2022年相比,前25名公司的总营收有所下降,从2022年的5790亿美元减少到2023年的5245亿美元,减少约9%。前25名中营收最高额为692亿美元,第25名为590亿美元,前后约相差100亿美元。这也意味着前25名的最低销售额门槛。Source: Semiconductor Industry Watch

The top 25 global semiconductors in 2023: Nvidia bucked the trend, storage manufacturers collectively declined, and automotive chips became a bummer! Although many semiconductor providers went through a difficult downward cycle in 2023, the overall performance of the industry remained resilient, showing strong resistance to falling.

Recently, TechInsights announced the final ranking of the top 25 semiconductor suppliers in 2023. In 2023, no new suppliers entered the top 25 list, but the company rankings changed significantly. Among the top semiconductor suppliers in 2023, 11 rose in rank, 11 declined, and 3 companies ranked the same as in 2023. Notably, foundry companies have also been added to the top 25 list, but mainly to compare annual sales, not as a market share ranking.

Revenue performance

First, in terms of overall revenue, compared with 2022, the total revenue of the top 25 companies declined, from US$579 billion in 2022 to US$524.5 billion in 2023, a decrease of about 9%. The top 25 had the highest revenue of 69.2 billion US dollars, while the 25th had 59 billion US dollars, a difference of about 10 billion US dollars before and after. This also means the minimum sales threshold for the top 25.

First, in terms of overall revenue, compared with 2022, the total revenue of the top 25 companies declined, from US$579 billion in 2022 to US$524.5 billion in 2023, a decrease of about 9%. The top 25 had the highest revenue of 69.2 billion US dollars, while the 25th had 59 billion US dollars, a difference of about 10 billion US dollars before and after. This also means the minimum sales threshold for the top 25.

Judging from the performance of individual companies,$Taiwan Semiconductor (TSM.US)$As an industry leader, although revenue declined, it topped the list with revenue of 69.2 billion US dollars. Thanks to the huge growth of its GPU processors for artificial intelligence (AI) workloads in data center servers, Nvidia “stood out” in the top 25, achieving a 102% three-digit increase, jumping from 8th place in 2022 to fourth place with 49.6 billion US dollars in revenue. With $17.3 billion in revenue, Infineon advanced 5 places to the top 10.

Despite the difficult macroeconomic environment, 7 of the top 25 global vendors have achieved growth, as mentioned above$NVIDIA (NVDA.US)$(102%),$Broadcom (AVGO.US)$(12%),$INFINEON TECHNOLOG (IFNNY.US)$(10%),$STMicroelectronics (STM.US)$(7%),$NXP Semiconductors (NXPI.US)$(1%),$Sony Group (6758.JP)$(12%),$Microchip Technology (MCHP.US)$(7%) These manufacturers have largely benefited from high demand for automotive applications. According to TechInsights research, the global automotive semiconductor market grew 16.5% in 2023 to reach a record $69.2 billion.

The remaining 18 manufacturers all experienced varying degrees of decline. Among them, storage vendors in particular experienced the most severe decline. Traditional memory chip makers Samsung (-34%), Micron (-35%), SK hynix (-28%), Kioxia (-37%), and Western Digital/SanDisk (-26%) have all declined in sales rankings as a result.$Samsung Electronics Co., Ltd. (SSNLF.US)$Semiconductor revenue fell 34% to $50.9 billion, the lowest value of its annual semiconductor sales output since 2016. Despite the poor sales performance of memory vendors last year, DRAM and NAND flash memory prices are showing a strong upward trend, which will enable memory IC vendors to achieve the strongest revenue growth in 2024.

regions

From a regional perspective, the US is an important center for global technological innovation and semiconductor industry. It has more than half of the top 25 semiconductor suppliers, and 13 of the top 25 suppliers are headquartered in the US.

Although the US dominates the list, companies from Asian countries such as China, South Korea, and Japan still play a key role in the global semiconductor supply chain. In particular, TSMC is number one on the list and is also the world's largest foundry. Of the top 25, there are 4 companies in China, namely TSMC (1st), MediaTek (14th),$United Microelectronics (UMC.US)$(section 22) and$SMIC (00981.HK)$(No. 24). The three are located in Taiwan, China. There are 3 companies in Japan: Sony (17th), Renesas (18th), and Kioxia (23rd). Korea mainly has two companies, Samsung (3rd) and SK Hynix (7th). They have strong capabilities in the storage field.

Infineon (9th), ST (10th), and NXP (15th) are the European troika. Europe was the only region that achieved growth last year. Sales increased 4%, and European semiconductor manufacturers mostly concentrated their efforts in the automotive and industrial sectors. China and the Asia-Pacific region saw the biggest decline. China is the semiconductor industry's largest sales market, and its revenue fell 14% in 2023. The American market shrank by 5.2%.

Product categories

In terms of product categories, in addition to the four pure wafer foundries, the products sold by other companies include integrated circuits and PSD devices (optoelectronics, sensors, and discrete devices).

Among the top 25 manufacturers, in addition to TSMC, the other three pure wafer foundries are$GlobalFoundries (GFS.US)$, UMC, and$Semiconductor Manufacturing International Corporation (688981.SH)$. These companies specialize in manufacturing semiconductor products for other companies. They don't design their own chips, but are produced according to designs provided by customers. Demand for wafer processing services declined in 2023 due to slow growth and inventory backlogs in smart phones, PCs, data center servers, and other end markets. GlobalFoundries, ranked 21st, saw sales fall 9% to $7.4 billion in 2023; UCC's revenue, which ranked 22nd, fell 24% to $7.1 billion; and SMIC, ranked 24th, saw sales drop 13% to $6.3 billion, falling to 24th place in the 2023 ranking.

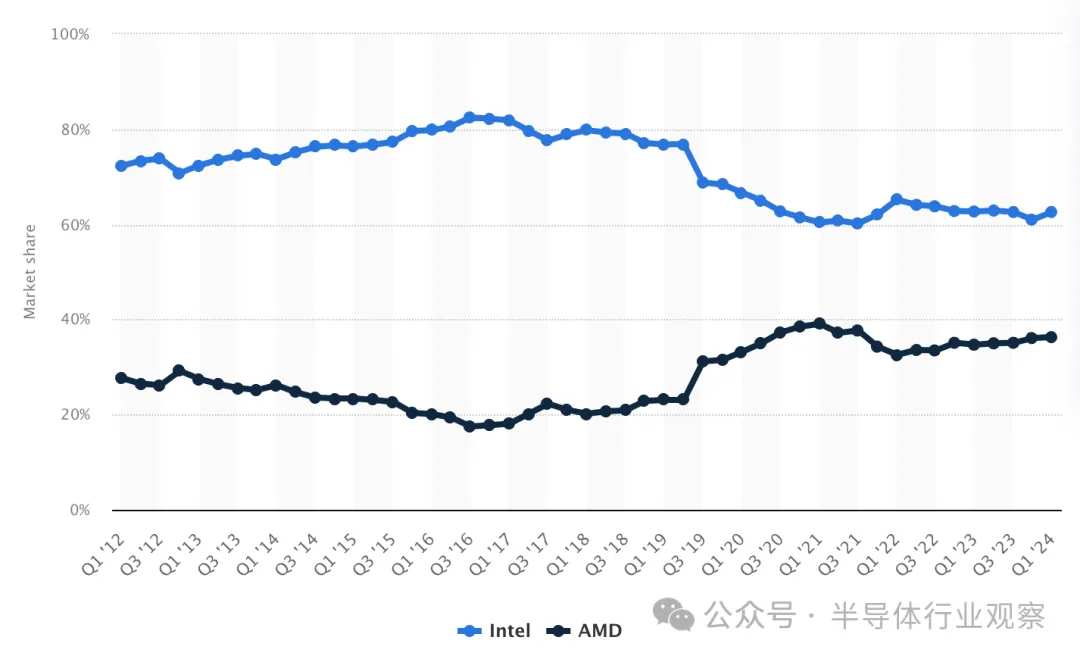

Processor manufacturers: Intel, Nvidia, and AMD are all hampering each other. Intel and AMD compete in the CPU field, while Nvidia and AMD compete in the GPU field. Intel is the world's largest manufacturer of PC and server processors. At its peak, it occupied more than 80% of the market share, but in recent years AMD has continued to encroach on Intel's CPU market share. According to data from CPU tracking company Mercury Research, AMD's overall CPU share reached a record high of 31.1% last year, while Intel fell to 68.9%.

In the current AI era, competition between the three companies in the field of AI chips is also fierce. In the field of generative AI in the cloud, Nvidia's GPU chip H 100, AMD's Instinct MI300X, and Intel's Gaudi predict a fierce competition in 2024. In the AI PC field, it is also a field strongly advocated by Intel and AMD. In this regard, Intel's Core Ultra is gaining momentum and has already explored six major scenarios in the PC field. If you are interested, check out “Commercial AI PCs, Open a New Blue Ocean!”

Cell phone SoC:$Qualcomm (QCOM.US)$, Apple, MediaTek. Qualcomm, ranked 5th, and MediaTek, are both mobile phone processor providers. Apple, ranked 13th, designs and uses its own SoCs, such as A-series and M-series chips, for iPhone, iPad, and Mac products. I have to say that the mobile phone market is indeed a bit tepid. The phone updates aren't attractive enough, and the phone processor doesn't have any highlights. Even though Apple released the 3nm A17 Pro chip last year, it still hasn't surprised me much. After ten years of brilliant phones, it's hard to hide the frenzy of cars. These mobile phone processor providers are gradually igniting the flames of war in the rapidly growing automotive market.

Although most of Qualcomm's revenue comes from the mobile phone and IoT business, it is its automotive business that has experienced significant growth. Qualcomm's automotive business grew 25% in 2023. In recent years, Qualcomm has rapidly entered the field of automotive cockpit and autonomous driving chips, and is now the best choice for smart cockpit chip suppliers. By the end of 2023, more than 350 million cars had been equipped with Snapdragon digital chassis solutions. MediaTek also released a new Dimensity Auto smart cockpit SoC with generative AI in March of this year. It is foreseeable that it will once again compete with Qualcomm in the field of automotive cockpit chips.

Memory chip vendors: Samsung (3rd), SK Hynix (7th), Micron (11th), Kioxia (23rd), Western Digital/SanDisk (25th) are established players of memory chips. Speaking of these storage vendors, as the sector most affected by the semiconductor cycle, no one is doing well. Samsung's profit plummeted 97%, SK recorded the biggest loss in history, inventory from Micron and Western Digital climbed, and memory chips almost hit rock bottom. Despite this, SK Hynix can be described as having unlimited success throughout 2023. Since it is ahead of other memory vendors in high-bandwidth memory (HBM), it is not popular with Nvidia's GPUs in the AI wave.

By 2024, the storage market had suddenly improved. HBM is still being taken over by the market. Overall production capacity supply is far less than demand, and manufacturers such as SK Hynix, Samsung, and Micron are all struggling. I believe that with the improvement of the storage market, the 2024 semiconductor supplier list may be another new sight, and storage manufacturers will raise their eyebrows.

Telecom and networking chips: Broadcom's 6th place covers a wide range of businesses, including wired and wireless communication chips, enterprise and data center networking solutions, storage devices and system software, and various other applications and services. Last year, Broadcom was also a beneficiary of the AI boom. Broadcom's network chips helped transmit large amounts of data needed for artificial intelligence calculations, and they all helped customers design customized artificial intelligence chips. In 2023, Broadcom's revenue for fiscal year 2023 increased 8% year-on-year, to a record high of US$35.8 billion, driven by hyperscale companies' investment in artificial intelligence accelerators and networking connections.

Broadcom is more than just a chip provider; it's also a software company. Recently, it acquired the software company VMvare for 610 US dollars, which attracted the attention of the industry. The CEO of Broadcom said that the acquisition of VMware is transformative. In the 2024 fiscal year, Broadcom expects annual revenue to reach 500 US dollars, and VMware will make a great contribution. Among them, revenue from artificial intelligence-related chips is expected to reach 10 billion US dollars this year. Broadcom CEO Hock Tan said at the earnings conference that about $7 billion of the company's 2024 AI chip revenue will come from helping two major customers design customized AI chips. Tan did not reveal the names of the clients, but analysts generally believe they are Google and META.

Automotive chips: Infineon (9th), ST (10th), NXP (15th), Renesas (18th), Microchip (19th), and Ansemi (20th) are important suppliers of automotive chips, involving power semiconductors IGBT/SiC/GaN, MCU, power management, sensors, etc. As far as the automotive market segment is concerned, Infineon is the No. 1 automotive semiconductor supplier in 2023. The main driving force behind this is sales of MCU products. The company first occupied the first position in MCU last year. In the overall ranking, Infineon jumped from 14th to 9th, and ST from 13th to 10th.

Analog chips: TI (12th) and ADI (16th) are established analog chip suppliers. These manufacturers generally sell a wide variety of chips, covering many important fields such as power semiconductors, signal processing, sensors, and MCUs, and have some competition in different market segments.

Image sensors: Although the 17th Sony is better known as an electronics manufacturer, it is also involved in semiconductor manufacturing, particularly in the field of CMOS image sensors (CIS). In the CIS market, Sony has the highest market share of about 42%, followed by Samsung, and the domestic Howell Technology ranked third. The AI wave has also brought demand for CIS updates. Various terminal applications are using lenses developed specifically for AI applications, which is expected to drive a new wave of demand to replace old lenses with new lenses. In order to seize the AI business opportunity, Sony launched a digital signal processor (DSP) equipped with artificial intelligence algorithms, which is expected to enhance applications such as human motion analysis, enhanced image processing, or human tracking. Furthermore, in addition to TSMC, Sony is the largest shareholder of JASM, the joint venture of TSMC's Japanese plant, which greatly guarantees its subsequent localized production.

Write it at the end

Although many semiconductor providers went through a difficult downward cycle in 2023, the long-term prospects for the semiconductor market are extremely strong as chips play a larger and more important role in the myriad products the world depends on for survival. According to the American Semiconductor Industry Association, the global chip industry is expected to rebound sharply this year, and sales are expected to jump to record levels. SIA also said that judging from the growing demand for electronic components in various industries, sales will increase 13% this year, reaching nearly 600 billion US dollars.

As the global semiconductor industry is gaining momentum in 2024, China's semiconductor industry will also usher in new development opportunities. In the future, we look forward to seeing more Chinese companies active in the top 25 global semiconductor lists, showing the hard-core strength of China Chip on the world stage.

edit/lambor