The S&P Index recorded the longest continuous decline in a year and a half. The NASDAQ fell more than 2%, fell more than 5% throughout the week, and fell more than 3% in a week, the biggest weekly decline since the Bank of Silicon Valley went out of business; the Dow rose two times in a row, the constituent stocks of American Express rose more than 6% after the earnings report, and UnitedHealth's earnings rose 14% over the week. The chip stock index closed down more than 4%, with Nvidia recording the biggest decline in four years; the AI “monster stock” Ultra Micro (SMCI) fell 23%; Netflix recorded its biggest decline in more than two years after reporting earnings; and Tesla fell 14% in a week. After the earnings report, L'Oréal rose 5%, and Asmack's earnings week fell 9.5%. China's stock index fell 1%, Ideal Auto fell 9.6%, and NIO fell 5%.

Risk aversion subsided. The 10-year US Treasury yield dived more than 10 basis points to smooth out most of the declines; the US dollar fell, and the yen took back all gains; gold fell several times after rising more than 1% in the intraday period; Bitcoin, which once fell below 60,000 US dollars in the intraday period, rebounded by nearly 6,000 US dollars. The offshore RMB Asian market rebounded nearly 200 points to recover 7.25, then turned down.

After rising more than 4% in the intraday period, crude oil fell by more than 1% at one point and narrowly closed higher. It still fell at least 3% throughout the week. Futures are still at a record high, rising for three weeks. Renxi rose nearly 5% to a new high in the past two years. It rose nearly 10% in a week, and Luntong rose to a two-year high three times in a row.

Federal Reserve officials have repeatedly dampened expectations of interest rate cuts. Even Chicago Federal Reserve Chairman Goulsby, who is seen as a dovish, said on Friday that progress in declining inflation has stalled so far. Technology stocks have once again taken the lead in suppressing the market. For the first time in a year and a half, the NASDAQ index fell more than 2% in one day for the first time since Federal Reserve Chairman Powell hit the March interest rate cut expectations at the end of January. S&P recorded its worst weekly performance since the risk shock of the Silicon Valley Bank collapse in March last year.

After announcing poor revenue guidelines for the second quarter and will stop reporting the number of quarterly subscribers, streaming media giant Netflix fell more than 9% in the market, the worst daily decline in more than two years; the AI benchmark Nvidia fell sharply by 10%, losing more than 200 billion US dollars in one day, the second-largest single-day decline in US stock market value in history, leading to the decline of tech giant “Seven Sisters”; the AI “monster stock” ultra-microcomputer, which had doubled since the beginning of this year, was sold off after confirming that it released earnings reports at the end of this month.

Corporate financial reports are beginning to take over the heavy responsibility of supporting the general market. Driven by the increase in spending by wealthy customers, credit card giant American Express surged 31% in the first quarter. Together with healthcare giant UnitedHealth, which announced excellent financial results on Tuesday, they supported the Dow to rise more than 200 points in the intraday period. Meanwhile, orders from European lithography giant ASML (ASML), which were announced earlier this week, fell sharply in excess of expectations, and TSMC lowered growth expectations for the semiconductor industry other than memory chips, and repeatedly hit chip stocks. Tesla's prospects for low-cost cars and autonomous taxis were questioned by Wall Street. Under pressure from blue chip technology stocks, major stock indexes almost continued to collectively decline, and the Dow used a surprise rebound over the past week.

Risks in the Middle East eased somewhat intraday on Friday. After an Israeli missile hit an Iranian target in the Asian market, Iran expressed restraint, saying that its nuclear facilities had not been damaged, and the US Secretary of State said that the US side had not participated in the Israeli attack. Reports from various sources indicate that Israel's attack was limited in scope and caused very little damage. Some commentators say that both Iran and the West are downplaying the impact of Israel's attacks, and Iran hinted to the media that it has no plans to retaliate against Israel. Other commentators believe that an open conflict between Iran and Israel is expected to be avoided, but the market may still be tense. Considering that Iran launched an attack against Israel last Saturday, nothing is taken for granted.

The risk aversion sentiment set off by the risk of the Middle East conflict “faded away”, and safe-haven assets surged back: gold, which jumped more than 1% in the Asian market, fell several times since then, and failed to approach or even break the historical intraday high set last Friday; the US dollar, which had been close to a five-month high, also fell several times in the intraday market. The yen fell below 154 against the US dollar. At one point, it began to approach the low point since 1990; the decline in US treasury bond prices narrowed, and the benchmark 10-year US bond yield dived more than 10 basis points in the Asian intraday market. It broke 4.50% for the first time, then rose to 4.60%, smoothing out most of the decline. Yields continued to rise cumulatively this week, when expectations of interest rate cuts were hurt.

Bitcoin, which plummeted after the Israeli attack, rebounded. After falling below 60,000 US dollars in the Asian market to its low level since the end of February, Bitcoin once hit 65,000 US dollars in the US stock market and rebounded to nearly 6,000 US dollars. Bitcoin's fourth halving in history is expected to arrive this weekend. Historical data shows that the currency price has generally risen after the halving. However, Deutsche Bank believes that the correlation between currency prices and stock indexes has declined recently, and the market has already partially set prices. It is expected that the price of the currency will not rise sharply this time, but it will remain high in the future.

Among commodities, Middle Eastern risks contributed. International crude oil rose more than 4% in the Asian intraday market on Friday, then turned down a few times, falling 5% from the daily low, and finally narrowed down by at least 3% this week. The US EIA crude oil inventory announced this week increased more than expected, and gasoline demand was once again disappointing, hitting oil prices. Some commentators say that after the Federal Reserve repeatedly suppresses expectations of interest rate cuts, the prospect that high interest rates will continue for longer makes investors worry about the sustainability of economic growth, and it is becoming bad for crude oil. The threat of direct conflict between Israel and Iran will continue to prevent further falls in oil prices, and the focus for the rest of the year will be on concerns about rising demand. Other commentators say that the risk of major Middle Eastern oil producers such as Saudi Arabia and the United Arab Emirates has not increased; in fact, only Iran is at risk, and it will only affect Iran's oil production if the scope of hostilities expands.

This week, when the British and American governments imposed sanctions on some Russian metals, industrial metals became big winners. Luntong and Renxi hit new highs in 2022 for three days. Lunxi surged by nearly double digits in a week. Luntong benefited from continued tight supply. Due to the drastic reduction in LME inventory on the London Stock Exchange and the emergence of long positions in the futures market, investors are wary of the risk of a contraction in Renxi's supply. Despite many intraday declines on Friday, precious metal gold and silver futures both closed higher. Futures closed at record highs on the 3rd day of this week, and continued to rise this week, driven by geopolitical risks.

The NASDAQ fell more than 2% for four weeks, and the Dow rose two times in a row, Nvidia recorded the biggest decline in four years, and American Express surged, and Netflix's biggest decline in two years.

The three major US stock indexes opened with mixed ups and downs. The S&P 500 index, which opened low, turned higher at the beginning of the session. After turning down in early trading, it maintained a downward trend. It fell more than 1.1% in midday trading. The Nasdaq Composite Index opened low and fell more than 2.4% in midday trading. For the first time since January 31, the day Powell hinted after the Federal Reserve meeting that interest rates would not be cut in the short term, it fell more than 2% in the intraday period. The high-opening Dow Jones Industrial Average continued to rise throughout the day. It rose more than 100 points at the beginning of the session, over 200 points in early trading, mostly over 200 points in midday trading, and nearly 330 points at a fresh daily high.

In the end, the S&P and NASDAQ fell for six consecutive trading days, both of which recorded the longest continuous decline since October 2022. S&P closed down 0.88% to 4967.23 points, breaking the closing low since February 13. The NASDAQ closed down 2.05% to 15282.01 points, the biggest closing drop since January 31, and set a new closing low since January 31. The Dow closed up 211.02 points, or 0.56%. It closed higher for two consecutive days and the third day of this week, at 37986.40 points, further breaking away from the closing low since January 18, which was refreshed on Monday.

The small-cap stock index Russell 2000, which is mainly value stocks, closed up 0.24%, breaking out of the low since February 5, which was refreshed after five consecutive days of decline. The Nasdaq 100 Index, which focuses on technology stocks, closed down 2.05%, falling three consecutive days to its lowest level since January 18. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the Nasdaq 100 Index, closed down 3.26%, falling three times to a low level since February 21, and has declined by about 7% this week.

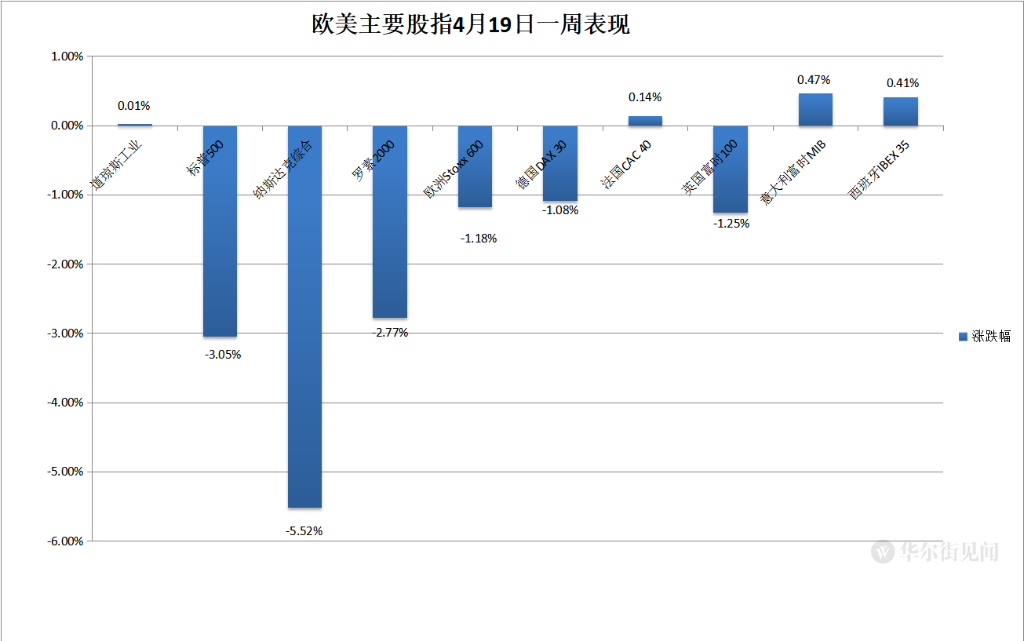

Most of the major US stock indexes fell sharply this week. S&P fell 3.05%, the biggest weekly decline since March 2023. Russell 2000 fell 2.77%, all for three consecutive weeks. The Nasdaq index fell 5.52%, the biggest weekly decline since November 4, 2022. It has fallen 6.98% in the last four weeks. It was the first four-week decline since December 30, 2022, and the biggest four-week decline during the same period. The NASDAQ 100 fell 5.36%, and also fell for four weeks in a row. Meanwhile, the Dow rose slightly by 0.01%, stopping two weeks of continuous decline.

Among the Dow's constituent stocks, American Express (AXP), which had good financial reports, led the rise, closing up 6.2%, Coca Cola, J.P. Morgan, and Amgen all rose more than 2%, and Chevron, the only energy stock, rose 1.6%. The healthcare giant UnitedHealth (UNH), which had continued to rise for the previous three days, rose 1.6%, and climbed 14.1% this week when it released excellent performance reports, while Amazon and Intel, which dropped more than 2%, had the biggest decline.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the tech giants “Seven Sisters” all closed down. Tesla turned up several times in early trading, falling more than 2% at the end of the session and closing down 1.9%. It fell six days and two days in a row, breaking its closing low since January 25, 2023. After rebounding last week and rising nearly 4%, it has fallen by about 14% this week.

Among the six major FAANMG technology stocks, Netflix opened down about 7%, closing down about 9.1%, the biggest closing decline since January 21, 2022, falling 3 times to a closing low since February 13; Meta closed down 4.1%, falling back to its closing low since February 21; Amazon closed down nearly 2.6%, falling 6 to a closing low from March 18; Microsoft closed down nearly 1.3%, falling for 3 days in a row; Apple closed down 1.2%, closing low since April 26, 2023; Alphabet closed down 1.1%, breaking the low since April 5 set on Tuesday.

Chip stocks generally accelerated their decline in midday trading and outperformed the general market. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX closed down about 4.1% and 4% respectively, falling three times to closing low since February 1, and fell 9.2% and 9% respectively this week. Among chip stocks, Nvidia, which rebounded on Thursday, opened low and fell 10.7% at the end of the session, closing down 10%, the biggest daily decline since March 16, 2020. The market capitalization evaporated about US$21.2 billion in one day, creating the second largest single-day market capitalization decline of US listed companies, second only to Meta, which shrunk by US$232 billion on February 3, 2022, to a record low since February 21, falling 13.6% this week; TSMC US shares, which closed down nearly 4% in early trading on Thursday, closed down 3.5% this week; Arm closes close 17%, AMD fell 5.4%, Micron Technology fell 4.6%, and Intel 2.4%.

Overall, AI concept stocks continued to decline, and also underperformed the market. After announcing that financial results for the third fiscal quarter will be released on April 30, the “demon stock” ultra-microcomputer (SMCI), which has risen more than 160% since the beginning of this year, closed down more than 23%. At the close, Astera Labs (ALAB), known as “Little Nvidia,” which sells data center interconnect chips, fell more than 9%, SoundHound.ai (SOUN) fell more than 7%, BigBear.ai (BBAI) fell more than 5%, Palantir (PLTR) fell more than 3%, and Adobe (ADBE) fell 1.7%. Oracle (ORCL) fell nearly 1%, and C3.ai (AI), which turned down in mid-day trading after turning higher at the beginning of the session, fell 0.7%.

Popular Chinese securities generally declined. The Nasdaq Golden Dragon China Index (HXC), which stopped three consecutive declines on Thursday, closed down about 1%, approaching the closing low since February 13 set on Wednesday. It has fallen by about 2.1% this week, falling for two consecutive weeks. KWEB and CQQQ closed down around 0.6% and 1.8%, respectively. Among the new car builders, Ideal Auto fell 9.6%, NIO Auto fell 5%, Xiaopeng Motors fell nearly 3.8%, and Xiaomi Fan fell more than 3%. Among other individual stocks, Pinduoduo and Jingdong fell more than 1% in early trading, Station B fell less than 1%, and Baidu fell slightly. Alibaba narrowed most of its losses at the beginning of the market, while NetEase rose slightly, and Tencent fans rose slightly.

Among individual stocks with high volatility, media giant Paramount Global (PARA) closed up 13.4% after Sony Pictures Entertainment and investment management company Apollo Global Management discussed the possibility of joint acquisition; mobile technology company Ibotta (IBTA), which surged more than 17% on the first day, fell 8.6% in the intraday market and closed down 5.1%.

In terms of European stocks, the pan-European stock index, which rebounded slightly for two consecutive days, fell, and some companies' financial reports improved, curbing the decline in European stocks. The European Stoxx 600 index closed down less than 0.1%, close to its closing low since March 6, which was refreshed on Tuesday. Major European stock indexes showed mixed results. The British and Italian stock indexes rose for three days; the German and Spanish stock indexes, which had risen two times in a row, fell, and French stocks, which had risen two times in a row, were largely flat.

Among the various sectors, technology closed down about 1.8%. Among the constituent stocks, Asmack (ASML), Europe's highest market-capitalization technology stock listed in the Netherlands, fell 2.3%; automobiles fell nearly 0.8%, affected by Volvo, which sold part of its holdings by Geely, the second-largest shareholder; while Telecom rose 1.1%. Among the constituent stocks, Finnish company Elisa, whose EBITDA profit rose nearly 4% in the first quarter, led by 4.4%; the luxury goods giant's personal and household goods rose 0.6%, thanks to the announcement that sales in the first quarter exceeded expectations and sales growth exceeded expectations in North America and Europe After that, France Listed beauty giant L'Oréal closed up about 5%.

The Stoxx 600 index fell 1.18% this week, falling for four consecutive weeks, falling more than 1% for another week after last week, extremely close to the biggest weekly decline since January 19, which was caused by last week's decline. Stock indices from various countries had mixed ups and downs. The Dutch stock index, where Asmack is located, fell more than 2%, leading the decline. German stocks and British stocks fell more than 1%, falling for three weeks, while French, Italian and Western stocks, which had been falling for two weeks, rose slightly.

Among the various sectors, technology led the decline by 5.8%. Asma recorded decline of more than 9.5% this week, when it was announced that orders for the first quarter were far lower than expected. Last week, oil and gas, which rose nearly 4%, fell more than 3%, basic resources, which rose more than 4% last week, fell more than 1.5%, while personal and household goods rose more than 1.8%. Telecom increased by 0.7% this week due to higher prices on Friday.

Ten-year US Treasury yields smoothed out most declines after diving more than 10 basis points in the Asian market

The yield on the US 10-year benchmark treasury bond dived below 4.50% in early trading in the Asian market. It fell 4.50% in the intraday market for the first time since last Friday, April 12, and continued to recover. European stocks weighed 4.60% in early trading. US stocks were close to leveling off all declines in early trading, and are still far from the high level since November 13, 2023, which was updated for two consecutive days. By the end of the bond market, it was about 4.62%, falling about 1 basis point during the day. The yield rebounded on Thursday and fell about 1 basis point during the week. 10 basis points, three weeks of continuous improvement.

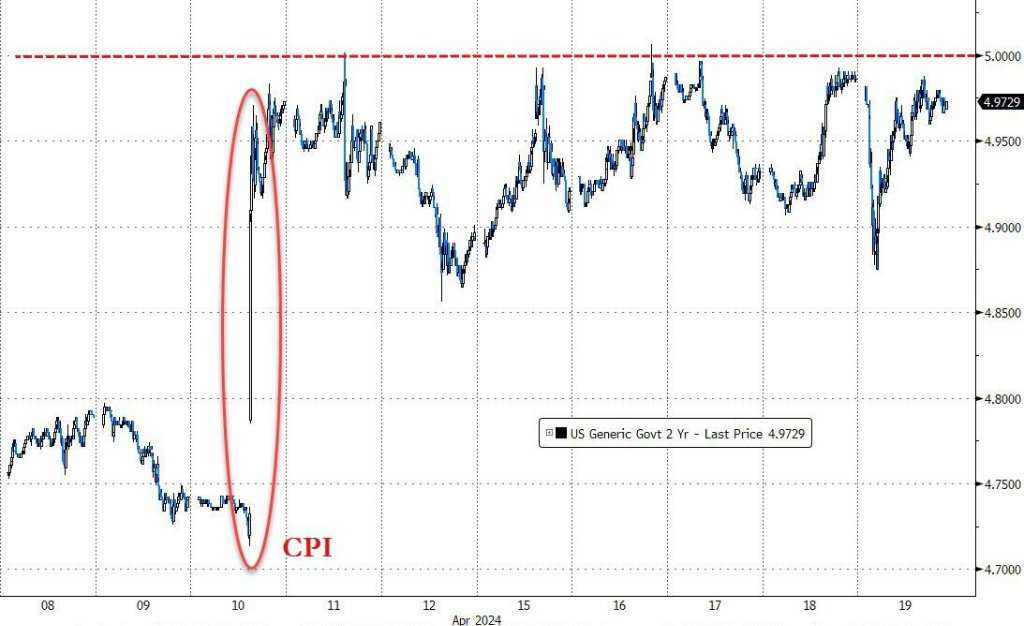

The 2-year US Treasury yield, which is more sensitive to interest rate prospects, broke 4.88 in early Asian trading and fell by about 11 basis points during the day. The US stock market rose in the short term and 4.99% in early trading, and continued to rise close to the high level since November 14, 2023, which was refreshed by 5.0% on Tuesday. It had all been up or above 5.0% in the last four days. By the end of the bond market, it was about 4.99%. By the end of the bond market, it had generally remained flat at the same time of Thursday, rising by about 9 basis points for 4 consecutive weeks.

The US dollar index fell a few times during the day, and the yen returned to intraday gains. Bitcoin once rebounded by nearly $6,000 after falling below the 60,000 mark

The ICE dollar index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, rose above 106.30 in early Asian trading, close to the high level since November 1, 2023, which was refreshed for two consecutive days after rising 106.50 on Tuesday. After European stocks declined before the market, only European stocks rose in the short term in early trading. US stocks fell below 105.90 at a fresh low in early trading.

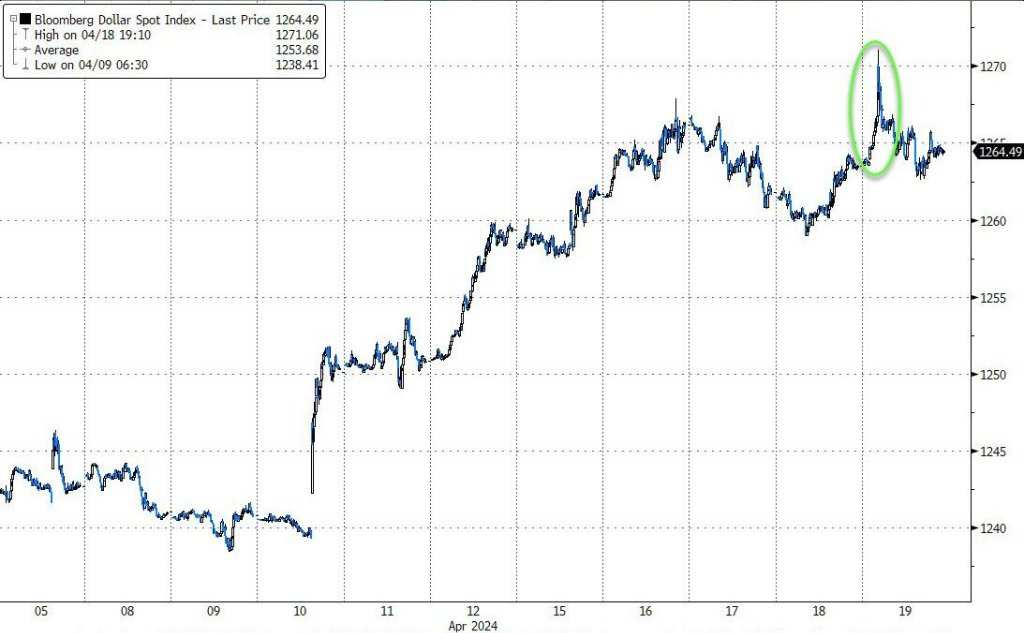

By the close of the US stock market on Friday, the US dollar index was above 106.10. After rebounding on Thursday, it had risen 0.1% this week; the Bloomberg US Dollar Spot Index, which tracks the exchange rate of the US dollar against ten other currencies, rose less than 0.1%. After ending five consecutive gains on Wednesday, it continued to rise 2 times in a row since November 2023, which was refreshed on Tuesday. The increase was far less than last week when it rose by more than 1%.

Among non-US currencies, the yen surged higher and fell on Friday. The US dollar was close to 154.70 to 154.67 in early Asian trading, close to the high level since 1990, which was set at 154.80 on Tuesday. After the attack on Iran broke out, the Asian market dived below 153.60, smoothing out the gains during the week. It fell nearly 0.7% during the day, and continued to rebound. The US stock market closed down all losses; EUR/USD was down 1.0610 in early Asian trading, close to Powell's speech on Tuesday The lowest level since the end of October 2023, which was updated to 1.0600 in the next test, It fell 0.3% during the day, and before European stocks opened, the decline of GBP/USD increased after the opening of the US stock market. It fell below 1.2370 in midday trading, breaking the low since November 2023 set on Tuesday, and fell more than 0.5% during the day.

The offshore renminbi (CNH) plummeted against the US dollar in early trading and rebounded soon after. The Asian market hit a fresh daily high of 7.2457, rising 172 points from the daily high, approaching the high level since April 10, which was refreshed on Wednesday, and has since declined several times. At 4:59 Beijing time on April 20, the offshore RMB was 7.2512 yuan against the US dollar, down 16 points from the end of Thursday's session in New York. It has been falling for two days. It has continued to rise 161 points this week, rebounding after falling back last week, and has continued to rise in the third week of the last four weeks.

Bitcoin (BTC) fell below 59,700 US dollars in early Asian trading, breaking its low since the end of February, and soon rebounded. European stocks rose above 65,400 US dollars and rose nearly 10% from the intraday low. US stocks fell 65,000 US dollars in early trading, and US stocks fell above 64,000 US dollars at the close of the day and hovered around 64,200 US dollars. At the end of the day, US stocks were above 64,000 US dollars and hovered around 64,000 US dollars.

Crude oil rose more than 4% in the intraday period, then turned down more than 1% and barely closed up and still fell nearly 3% throughout the week

International crude oil futures surged higher in early Asian trading. At the time of the day's high, US WTI crude oil rose close to $86.30 and rose about 4.3% during the day. Brent crude oil rose above $90.70, rising nearly 4.2% during the day, and continued to decline. European stocks turned down $81.80 and oil fell below $86.20. They all fell about 1.1% during the day, falling about 5.2% and 5% respectively from the intraday high. US stocks turned down in the short term after rising early trading.

In the end, crude oil collectively closed higher for the first time in the last five trading days. WTI crude oil futures for May closed up about 0.5% to $83.14 per barrel, breaking away from the closing low since March 27, which was refreshed on Wednesday after closing slightly on Thursday; Brent crude oil futures for June, which had been falling for four days, closed up 0.20% to $87.29 per barrel, leaving aside the closing low since March 27, which was refreshed on Thursday.

US oil fell more than 2.9% this week, and oil fell by about 3.5%, mainly due to the announcement of the US EIA crude oil inventory falling more than 3% on Wednesday. Crude oil fell for two weeks in a row this week. It fell for the eighth week in the last 14 weeks. It was also the 16th week in 28 weeks since the outbreak of the Israeli-Palestinian conflict. After surging more than 10% in the first quarter, it has declined for two weeks in the past three weeks in the second quarter.

Lunxi rose nearly 5%, rose nearly 10% in a week, and Luntong reached a two-year high, gold fell several times after rising more than 1% in the intraday period and still closed at a record high

London basic metals futures closed higher across the board on Friday, up at least 1%. Lunxi rose more than 4.7%, leading the way for three consecutive days, hitting new highs since June 2022 for the third day, while copper, lentin lead, and nickel all rose for 3 consecutive days. Lun Ni rose more than 4%, closing at the $19,000 mark for the first time since September last year; Luntong, which hit a two-day high for nearly two years, closed above 9,800 US dollars for the first time since April 2022; after Monday, Lunqian hit a new high since November last year. Lunan aluminum rose more than 2%, rising for six days in a row, hitting a new high since June 2022. Lunzinc smoothed out Thursday's decline and refreshed the high since April last year set on Wednesday.

These metals have all been rising this week. Lunxi has risen by nearly 10%, copper has risen by more than 4%, and lunzine has risen nearly 0.9%, all for three weeks; Lun aluminum has been rising for about 7%, six weeks in a row; Lun lead has risen nearly 2%, four weeks in a row; and Lun nickel, which has declined slightly last week, has risen by more than 8%.

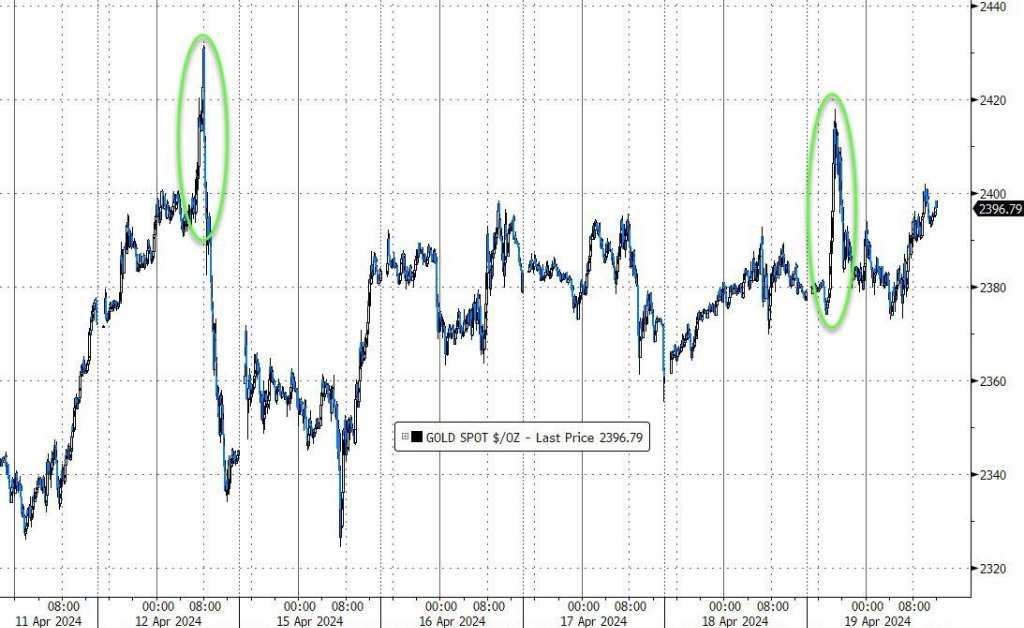

New York gold futures were as low as $2386.8 in early Asian trading and fell nearly 0.5% during the day. After news of the Israeli attack came out, they jumped above $2,430 and reached a new daily high of $2433.3. Beginning close to the record intraday high set last Friday, rising nearly 1.5% during the day. Since then, Asian and European stocks have all declined in intraday and early US stocks. After that, the US stock market maintained gains after rising again in early trading.

In the end, COMEX's June gold futures closed up 0.66% to $2413.8, rising for two consecutive days, breaking the highest closing record set on Tuesday, and a record high for the third day of this week. It has been rising 1.67% throughout the week, rising for three consecutive weeks. It has been rising for the 20th week within 28 weeks since the outbreak of the Israeli-Palestinian conflict, but the increase was far less than the previous week ending April 5, which had a cumulative increase of 4.78% during the week.

Spot gold rose in early Asian trading. It was close to 2,418 US dollars, breaking the intraday high level since last Friday, April 12. It rose 1.6% during the day and continued to decline thereafter. European stocks turned down several times in the intraday period, falling below $2,373 during the day, falling close to 0.3% during the day, falling nearly 1.9% from the daily high. The increase in early trading of US stocks expanded and climbed to $2,390. At the close, spot gold was slightly below $2,390, up about 0.4% during the day. The close still broke the record high set on Tuesday.

Editor/Jeffrey