To the annoyance of some shareholders, Lulu's Fashion Lounge Holdings, Inc. (NASDAQ:LVLU) shares are down a considerable 25% in the last month, which continues a horrid run for the company. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 47% in that time.

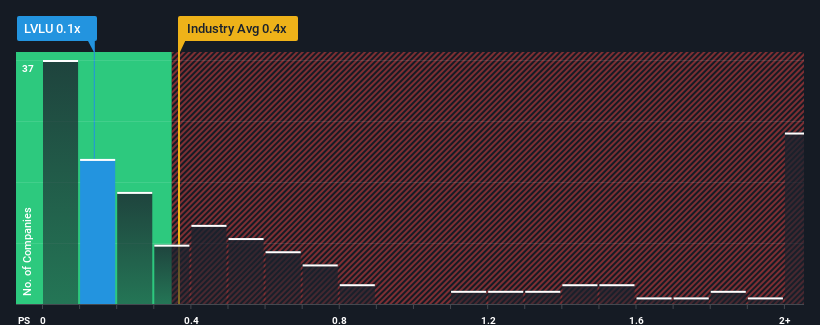

In spite of the heavy fall in price, it's still not a stretch to say that Lulu's Fashion Lounge Holdings' price-to-sales (or "P/S") ratio of 0.1x right now seems quite "middle-of-the-road" compared to the Specialty Retail industry in the United States, where the median P/S ratio is around 0.4x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

What Does Lulu's Fashion Lounge Holdings' P/S Mean For Shareholders?

Lulu's Fashion Lounge Holdings could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Lulu's Fashion Lounge Holdings will help you uncover what's on the horizon.How Is Lulu's Fashion Lounge Holdings' Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Lulu's Fashion Lounge Holdings' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a frustrating 19% decrease to the company's top line. Even so, admirably revenue has lifted 43% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Looking ahead now, revenue is anticipated to climb by 2.7% per year during the coming three years according to the four analysts following the company. With the industry predicted to deliver 5.6% growth per annum, the company is positioned for a weaker revenue result.

In light of this, it's curious that Lulu's Fashion Lounge Holdings' P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On Lulu's Fashion Lounge Holdings' P/S

With its share price dropping off a cliff, the P/S for Lulu's Fashion Lounge Holdings looks to be in line with the rest of the Specialty Retail industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Given that Lulu's Fashion Lounge Holdings' revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

You always need to take note of risks, for example - Lulu's Fashion Lounge Holdings has 3 warning signs we think you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.