Key Insights

- Gorman-Rupp's Annual General Meeting to take place on 25th of April

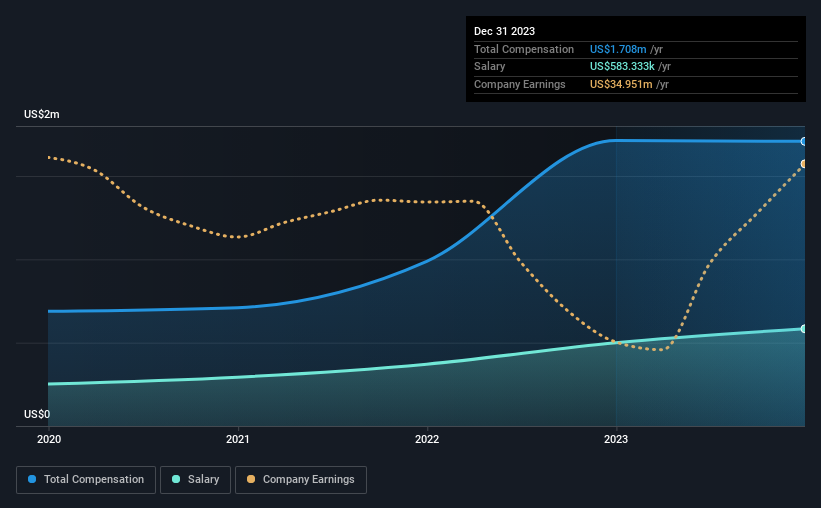

- CEO Scott King's total compensation includes salary of US$583.3k

- The overall pay is 56% below the industry average

- Gorman-Rupp's EPS grew by 11% over the past three years while total shareholder return over the past three years was 14%

The decent performance at The Gorman-Rupp Company (NYSE:GRC) recently will please most shareholders as they go into the AGM coming up on 25th of April. The focus will probably be on the future strategic initiatives that the board and management will put in place to improve the business rather than executive remuneration when they cast their votes on company resolutions. In our analysis below, we discuss why we think the CEO compensation looks acceptable and the case for a raise.

Comparing The Gorman-Rupp Company's CEO Compensation With The Industry

At the time of writing, our data shows that The Gorman-Rupp Company has a market capitalization of US$945m, and reported total annual CEO compensation of US$1.7m for the year to December 2023. That's mostly flat as compared to the prior year's compensation. We think total compensation is more important but our data shows that the CEO salary is lower, at US$583k.

On comparing similar companies from the American Machinery industry with market caps ranging from US$400m to US$1.6b, we found that the median CEO total compensation was US$3.9m. This suggests that Scott King is paid below the industry median. Moreover, Scott King also holds US$1.5m worth of Gorman-Rupp stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$583k | US$500k | 34% |

| Other | US$1.1m | US$1.2m | 66% |

| Total Compensation | US$1.7m | US$1.7m | 100% |

On an industry level, around 15% of total compensation represents salary and 85% is other remuneration. Gorman-Rupp is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

On an industry level, around 15% of total compensation represents salary and 85% is other remuneration. Gorman-Rupp is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

The Gorman-Rupp Company's Growth

Over the past three years, The Gorman-Rupp Company has seen its earnings per share (EPS) grow by 11% per year. Its revenue is up 27% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has The Gorman-Rupp Company Been A Good Investment?

With a total shareholder return of 14% over three years, The Gorman-Rupp Company shareholders would, in general, be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

Overall, the company hasn't done too poorly performance-wise, but we would like to see some improvement. If it manages to keep up the current streak, CEO remuneration could well be one of shareholders' least concerns. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for Gorman-Rupp that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.