S&P recorded the longest continuous decline in half a year, and the NASDAQ hit a new low in nearly two months; the Dow rebounded slightly, leading the rise in constituent stocks three days after the Joint Health report. Tesla, which was downgraded by Deutsche Bank, closed down 3.6% to a new low of over a year, and Meta closed up 1.5%; the chip stock index fell more than 1%, but Nvidia turned up after falling nearly 2% at the beginning of the market; after earnings reports, TSMC's US stock fell nearly 5%, and fell 7% after Netflix. The China Securities Index closed up 1%, stopping three consecutive declines. NIO rose more than 2%, and Xiaopeng Motors fell more than 3%. US bond yields picked up at an accelerated pace after the statements of the top three leaders of the Federal Reserve. The two-year yield rose to 5.0%, approaching a five-month high. The rebound dollar index rose to a new high; the rebounding futures “plummeted.” The yen is approaching its low level since 1990. The offshore renminbi fell more than 100 points in the intraday period and fell below 7.25. Bitcoin rebounded more than $3,000 in the intraday period to $64,000. Crude oil fell four times in a row and hit a new low for three weeks. After falling more than 1% in the intraday period, it turned higher. Renxi rose nearly 4%, hitting a two-year high with Luntong.

Following European lithography giant ASML (ASML), TSMC, which released financial reports, also hit chip stocks and continued to drag down the general market downside. The S&P 500 index recorded the longest continuous decline since the Federal Reserve turned dovish in October last year, fueling expectations of interest rate cuts this year.

TSMC announced that it achieved profit growth for the first time in a year in the first quarter, and its revenue guidance for the second quarter was higher than expected, but at the same time lowered the growth expectations of the semiconductor industry as a whole this year, with the exception of memory chips, as well as the expectations of the global foundry industry this year. Chip stocks declined further as a whole. The chip stock index, which fell more than 10% from last month's high, is in a deep adjustment range. At one point, TSMC's US stock fell more than 6%.

Tech giants have had mixed ups and downs. Meta rose more than 3% in the Meta market. It upgraded its big model, launched Llama 3, the strongest open source model, and Facebook and other social media included the “smartest” free AI assistant built on Llama 3; TSMC's biggest sales driver and AI benchmark, Nvidia's initial decline turned up by nearly 2%, after falling into the adjustment range and ushered in a subscription trough in early March; it is expected that after falling more than 20% in the next year, Tesla announced that users fell more than 4% in the first quarter; Growth far exceeded expectations, but After poor revenue guidance for the second quarter and warning of a slowdown in user growth, Netflix dived after the market.

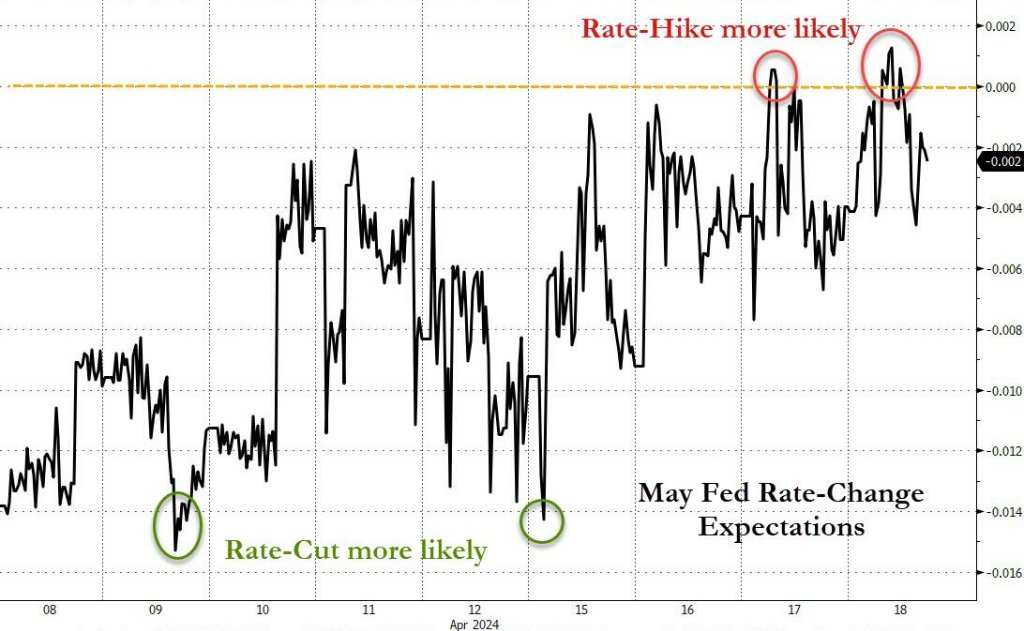

On the bond market side, the price of US Treasury bonds rebounded and the “one-day trip” declined, and yields returned to an upward trend. Some data released on Thursday shows that the US economy is stable: in April, the Philadelphia Federal Reserve manufacturing index far exceeded expectations and rose to a two-year high. The number of people applying for unemployment benefits for the first time last week did not rise but fell. At the same time, Federal Reserve officials “set the hawk” again: On Wednesday night, Federal Reserve Governor Bowman said that the progress in reducing inflation was slow and might even stagnate. On Thursday, the “top three” of the Federal Reserve and New York Federal Reserve Chairman Williams said he was not in a hurry to cut interest rates, and mentioned interest rate hikes twice, saying that interest rate hikes are not his benchmark forecast, but if the data is based, interest rates may be raised. After Williams's speech, the increase in US bond yields widened, and the interest rate sensitive two-year US Treasury yield rose to 5.0%, approaching the five-month high created by breaking this mark on Tuesday.

In the foreign exchange market, the US dollar index rebounded. After Williams's speech, the increase widened and reached a new daily high, starting to approach the five-month high set on Tuesday. Bank of Japan Governor Ueda Kazuo said that if the yen depreciates sharply boosts domestic inflation, the central bank may raise interest rates again. The intraday decline of the yen against the US dollar is still widening, approaching the low since 1990 set on Tuesday. Commentary said that market participants are wary that the Japanese government may interfere in the foreign exchange market at any time, but they expect Japan's entry threshold to be raised to 155. Bitcoin halving, the supply reduction stimulus event, has entered the countdown. Bitcoin is still rebounding unaffected by the US dollar. In the intraday period, it has risen by more than $3,000 to reach 64,000 US dollars, breaking the low of more than a month since falling below 60,000 US dollars on Wednesday.

Among commodities, when the US dollar rebounded, gold had limited recovery and failed to break the highest closing record set on Tuesday. After Williams spoke, New York futures even declined in the short term. International crude oil continued to fall, but there was a marked easing from Wednesday's decline, and the intraday decline of more than 1% was leveled off and turned upward. The comments said that the tension in the Middle East has eased somewhat, and the US sanctions against both oil-producing countries have affected oil prices. Venezuela lost an important license from the US to export oil. Although the US announced sanctions against Iran, OPEC's third-largest oil producer, the new sanctions did not affect Iran's oil industry.

S&P recorded the longest continuous decline in half a year, and Nvidia fell nearly 2% at the beginning of the market, then rose after earnings reports, and TSMC plummeted after the Netflix market.

The three major US stock indexes collectively opened higher and fell sharply in midday trading. The S&P 500 index fell close to 0.2% after falling at the beginning of the session, then quickly turned higher. The Nasdaq Composite Index fell nearly 0.6% after turning down at the beginning of the session, then turned up more than half an hour after opening. Both S&P and S&P rose nearly 0.7% when they hit a new high in early trading. After falling in midday trading, S&P fell 0.4%, and the NASDAQ fell 0.6%. The Dow Jones Industrial Average maintained an upward trend in early trading. It rose slightly over 330 points, rose nearly 0.9%, and turned down a few degrees in midday trading. It fell more than 70 points and fell nearly 0.2% at the low of the day, then turned slightly higher at the end of the session.

In the end, of the three major indices, only the Dow closed higher, up 22.07 points, or 0.06%, to 37775.38 points. It did not continue to approach the closing low since January 18, which was refreshed on Monday. The S&P and NASDAQ fell for five consecutive days. S&P closed down 0.22%, the longest losing streak since October last year, at 5011.12 points. The NASDAQ closed down 0.52% to 15,601.5 points, and both S&P set new closing lows since February 21 for four consecutive days.

The small-cap stock index Russell 2000, which is mainly value stocks, closed down 0.26%, falling for five consecutive days, breaking its low since February 5 on the 2nd. The tech-heavy Nasdaq 100 index closed down 0.57%, falling two consecutive days to its lowest level since February 1. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the Nasdaq 100 Index, closed down 0.52% and hit a new low since February 28 on the 2nd.

Among the constituent stocks of the Dow Index, healthcare giant UnitedHealth (UNH), which rose more than 5% after announcing earnings on Tuesday, had the highest increase for the third day, closing up nearly 3%. After announcing earnings on Wednesday, insurance company Travelers (TRV), which fell more than 7%, rebounded and rose nearly 1.9%, while Microsoft and Intel had the highest declines.

Of the major sectors of the S&P 500, only four closed down on Wednesday. IT, where chip stocks such as Microsoft and Intel are located, fell nearly 0.9%, Tesla's non-essential consumer goods fell 0.7%, industry fell 0.4%, and energy fell 0.2%. Among the seven sectors that closed, Meta's communications services led by nearly 0.7%, utilities rose 0.6%, and UnitedHealth's healthcare rose slightly.

Among the tech giants “Seven Sisters,” including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, only Meta had no decline throughout the day, and Tesla had the highest decline until the close.

Deutsche Bank analyst Emmanuel Rosner, who has been favored for a long time, downgraded the rating from buy to hold, and slashed the target price by 35% to $123, nearly 21% lower than Wednesday's close. Tesla fell by more than 4.3% at the beginning of the session, closing down nearly 3.6% for five days, breaking the closing low since January 25, 2023. Rosner pointed out that the low-cost model 2, which was originally expected to be launched by Tesla next year, now seems uncertain. This may change the investment theme of this individual stock, and warned that as Tesla increases its efforts in autonomous driving and AI technology, its stock investor base may experience a “painful transformation.”

Among the six major FAANMG technology stocks, Microsoft closed down 1.8% in early trading, down a low of 2 to March 6; Apple, which had been rising in early trading, fell nearly 0.6%, falling for 4 days, breaking the low since October 26, 2023 set last Wednesday; Amazon, which had risen slightly in early trading, fell more than 1.1%, falling continuously from 5 to March 26; Netflix, which will announce its earnings report for the first quarter on Thursday, then jumped 0.4% in early trading., which once fell more than 6%; on Wednesday it fell four times in a row to its lowest level since April 1 Meta rose nearly 3.7% in early trading and closed up 1.5%; Alphabet, which had a monopoly rise on Wednesday, fell more than 0.4% at the beginning of the session, turned up in early trading, and closed up nearly 0.4%, continuing to break out of the low since April 5, which was refreshed on Tuesday.

Chip stocks, which generally plummeted on Wednesday, failed to rebound. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX fell more than 2% at the beginning of the session, closing down about 1.7% and 1.8%, respectively. They fell for two consecutive days, breaking their closing lows since February 21. Among chip stocks, TSMC's US stock fell nearly 6.3% and closed down nearly 4.9% in early trading; Nvidia, which fell to its low level since March 1 on Wednesday, turned down 1.9% at the beginning of the session, then quickly turned up. It rose nearly 2.6% and closed up nearly 0.8% in midday trading; AMD, which turned into a short-term decline at the beginning of the session, closed up 0.7%; Intel closed down 1.8%; the media said it is expected to receive more than 6 billion US dollars in chip funding from the US Department of Commerce next week, Micron Technology rose more than 1% after early trading and then fell 3.8%; On Wednesday, it was announced that new orders for the first quarter surpassed expectations and fell sharply by 61% month-on-month, then plummeted nearly 7.1% of ASML (ASML) US stocks closed down nearly 2.1%.

The overall decline in AI concept stocks continued. Ultra-micro computers (SMCI), SoundHound.ai (SOUN), Astera Labs (ALAB), known as “Little Nvidia,” which sells data center interconnect chips, fell more than 3%, BigBear.ai (BBAI) fell more than 1%, Palantir (PLTR) fell 0.8%, Adobe (ADBE) fell 0.3%, Oracle (ORCL) fell more than 2%, and C3.ai (AI) rose more than 1%.

Popular Chinese securities generally rose. The Nasdaq Golden Dragon China Index (HXC), which has fallen three times and closed at a new low since February 13, closed 1% higher. KWEB and CQQQ closed up 0.8% and 0.6%, respectively. Among the new car builders, Nio Motors rose more than 2% at the close, Ideal Auto and Xiaomi fans alone rose more than 1%, while Xiaopeng Motors fell more than 3%. Among other individual stocks, by the close, NetEase rose nearly 3%, Tencent fans rose nearly 2%, Baidu and JD rose more than 1%, Ctrip rose nearly 1%, Station B rose nearly 0.4%, Pinduoduo rose 0.2%, and Alibaba rose less than 0.1%.

Bank stock indices continued to rebound. The overall banking index KBW Bank Index (BKX) closed up 0.7%, continuing to break out of the closing low since March 1, which was refreshed on Tuesday; the regional banking index KBW Nasdaq Regional Banking Index (KRX) closed up 0.6%, and the regional bank stock ETF SPDR S&P Regional Bank ETF (KRE) also rose about 0.6%, rebounding two days after breaking the closing lows since November 28 and November 30, 2023, respectively.

Among the major banks, Wells Fargo rose 2.7%, Bank of America rose 1.5%, J.P. Morgan Chase rose 0.7%, and Morgan Stanley closed up 0.2%. It continued to rise after the earnings report was released on Tuesday. Citi also rose 0.2%, while Goldman Sachs fell 0.2%.

Among the individual stocks that announced financial reports, Alaska Airlines (ALK) rose nearly 7% in early trading and closed 4% in early trading after reporting losses for the first quarter were lower than expected and the recovery in profit guidance for the second quarter rebounded above expectations; Alcoa (AA), which had higher first-quarter revenue than expected and losses per share was higher than expected, fell 4.8% at the beginning of the session, turned up in early trading and closed down 0.2%; the health insurance company Elevance Health (ELV), which reported higher earnings for the first quarter and raised its full-year guidance, rose more than 4% in early trading and closed 3.1%; Quarterly earnings and revenue were higher than expected, but Private equity investment giant Blackstone (BX), which is not much different from shareholders' cash back a year ago, fell more than 3% in early trading; credit institution Equifax (EFX), which had lower first-quarter results and second-quarter guidance than expected, fell more than 10% at the beginning of the session, closing down 8.5%. Real estate firm D.R. Horton (DH), which had better revenue and profit for the second fiscal quarter than expected, rose more than 5.8% at the beginning of the session and turned down nearly 2.1% in mid-session.

Among individual stocks with high volatility, DNA testing company 23andMe (ME) rose more than 50% in early trading and closed up 41.9% after the CEO revealed that the company was considering privatizing the company.

In terms of European stocks, financial reports from some companies continued to boost. The pan-European stock index, which recorded the biggest decline in nine months on Tuesday, rebounded slightly for two consecutive days. The European Stoxx 600 index continues to break away from its closing low since March 6, which was refreshed on Tuesday. The main European countries' stock indexes rose twice in a row, with the Spanish stock index rising more than 1%, leading the way.

Among the various sectors, the banking sector led the way with a closing rise of nearly 2.1%, mainly due to the fact that Bank of Italy, Bankinter, which is optimistic about future loan revenue growth, rose 5.3% after strong growth in the first quarter, and the Swiss listed industrial, energy and automation product giants rose by 5%; the telecommunications sector rose more than 0.8%. Among the constituent stocks, Tele2, which was higher than expected in the first quarter's service revenue and profits were higher than expected, closed up 6.7%; the industrial sector rose more than 0.6%, thanks to the announcement that profits for the first quarter were higher than expected and growth is expected to accelerate in the next few months ABB closed up 6.3%; while the technology sector fell nearly 0.8%. After Wednesday's earnings report, Europe's highest market-capitalization technology stock, which plummeted 6.7%, and the Dutch-listed ASML (ASML) European stock closed down 1.4%.

The price of US bonds fell back to a two-year yield of 5.0% in the intraday test, approaching a five-month high

The yield on the US 10-year benchmark treasury bond broke 4.56% before the European stock market. The yield on the European stock market continued to rise 4.60% at the beginning of the session. US stocks rose above 4.65% in midday trading and rebounded by more than 9 basis points from a daily low. It began to approach the high level since November 13, 2023, which rose 4.70% on Tuesday and refreshed for two consecutive days. It was about 4.63% at the end of the bond market. It rose more than 4 basis points during the day. The yield on other US bonds rebounded after falling back on Wednesday.

The 2-year US bond yield, which is more sensitive to interest rate prospects, fell below 4.91% in the Asian market, jumped above 4.97% at the beginning of the session, and rose 5.0% in the midday session, rising close to the high level since November 14, 2023, which was refreshed by 5.0% on Tuesday. It rebounded nearly 9 basis points from the daily low, about 4.99% at the end of the bond market, and rose by about 6 basis points during the last three days.

The dollar rebounded at an accelerated pace after the statements of the three leading members of the Federal Reserve, and the yen is approaching its low since 1990, Bitcoin rose more than $3,000 in the intraday period

The ICE Dollar Index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, fell below the daily low of 105.80 and fell nearly 0.2% during the day. US stocks basically maintained their gains after the pre-market rally. The increase widened after Williams's speech. In midday trading, it was close to the high level since November 1, 2023, which was refreshed at 106.50 on Tuesday, and rose more than 0.2% during the day.

By the close of the US stock market on Thursday, the US dollar index was above 106.10, up nearly 0.2% during the day; the Bloomberg US Dollar Spot Index, which tracks the exchange rate of the US dollar against ten other currencies, rose more than 0.1%, beginning to close to the simultaneous high since November 2023, which was refreshed on Tuesday, and the US dollar index rebounded after ending five consecutive gains on Wednesday.

Among non-US currencies, the yen fell back, approaching its low since 1990. USD/JPY was close to 154.70 in midday trading, approaching the high level since 1990 set for four consecutive days at 154.80 on Tuesday, rising nearly 0.2% during the day; EUR/USD approached 1.0640 after the US stock market closed and began falling to the low level since the end of October 2023, which was refreshed after Powell's speech on Tuesday; GBP/USD fell below 1.2440 in the US stock market and began to approach the low since November 17, 2023, which was refreshed on Tuesday.

The offshore renminbi (CNH) reached a new high of 7.2451 against the US dollar in early Asian trading, approaching the high level since April 10, which was refreshed at 7.2425 on Wednesday. European stocks maintained a downward trend after turning down before the market. US stocks reached a record low of 7.2539 in early trading, down 124 points from the daily high. At 4:59 Beijing time on April 19, the offshore RMB was 7.2496 yuan against the US dollar, down 56 points from the end of Wednesday's New York session, and fell on the second day of this week after rebounding on Wednesday.

Bitcoin (BTC) once dived close to $5,000 for an overall rebound on Wednesday. US stocks rose above $64,100 in early trading, rebounding more than $3,000 and up more than 5% from the intraday low of $60,900 in early trading, breaking away from the low since March 5 caused by falling below $60,000 on Wednesday. US stocks closed above $63,000 and rose nearly 4% in the last 24 hours.

Crude oil fell four times in a row to hit a new low for three weeks and then turned up after falling more than 1% in the intraday period

International crude oil futures hit a new low in early trading after European stocks declined before the market. US WTI crude oil fell below $81.60, Brent crude oil fell below $86.10, an average of nearly 1.4% during the day, and then turned up several times. When US stocks rose to a new high in midday trading, US oil was close to $83.50, up more than 0.9% during the day, and oil rose to $87.80, up nearly 0.6% during the day.

In the end, crude oil closed down slightly, falling for four consecutive days. The decline was significantly lower than Wednesday, which recorded the biggest drop since January 8. WTI crude oil futures for May, which fell more than 3.1% on Wednesday, closed up 0.04 US dollars, or 0.05% to 82.73 US dollars/barrel; Brent crude oil futures for June, which fell slightly more than 3% on Wednesday, fell 0.18 US dollars, or 0.21%, to 87.11 US dollars/barrel. Both days hit a low level since March 27.

Renshilun copper hit a new high in nearly two years, and futures that rebounded after the Fed official's speech “flashed down”

London basic metals futures mostly rose on Thursday, up at least 1%. Lunxi rose nearly 3.7%, leading the way for two consecutive days. Luntong, which had the same two consecutive gains, hit new highs since June 2022. Luntong closed above 9,700 US dollars for the first time in nearly two years. Lunnickel rose nearly 1.8%, rising for two consecutive days until the highest level since October last year. Lunan aluminum rose for five days and hit a new high since February last year for four days. Lead rose two times in a row, approaching the high level set on Monday since November last year. On Wednesday, lunzin rebounded to a high level since April last year and fell back.

New York gold futures fell as low as $2377.2 on the day of early Asian trading, and remained strong during the day. The US stock market hit a new high of $2,408 on the day, rising more than 0.8% during the day. It is still far from the record intraday high of nearly $2,450 last Friday. It turned down for a short time after Williams spoke in early trading in the US stock market.

By the close, COMEX June gold futures, which stopped rising four times in a row on Wednesday, closed up 0.4% to $2,398 per ounce. They are not close to the closing record set for the fourth day in a row by rushing to $2,410 on Tuesday.

Spot gold was close to a new daily high of 2,393 US dollars at the beginning of the market. It rose more than 1.3% during the day, and did not continue to fall below the historical intraday high set by rising above $2,430 last Friday. After Williams's speech, it fell below $2,370, returning most of its gains in the short term.

At the close of the US stock market, spot gold hovered at the front line of 2,380 US dollars, rising about 0.8% during the day, not close to the simultaneous record high set by slightly below the 2,390 US dollar mark on Tuesday.

editor/tolk