We Think You Can Look Beyond Wolong Resources Group's (SHSE:600173) Lackluster Earnings

We Think You Can Look Beyond Wolong Resources Group's (SHSE:600173) Lackluster Earnings

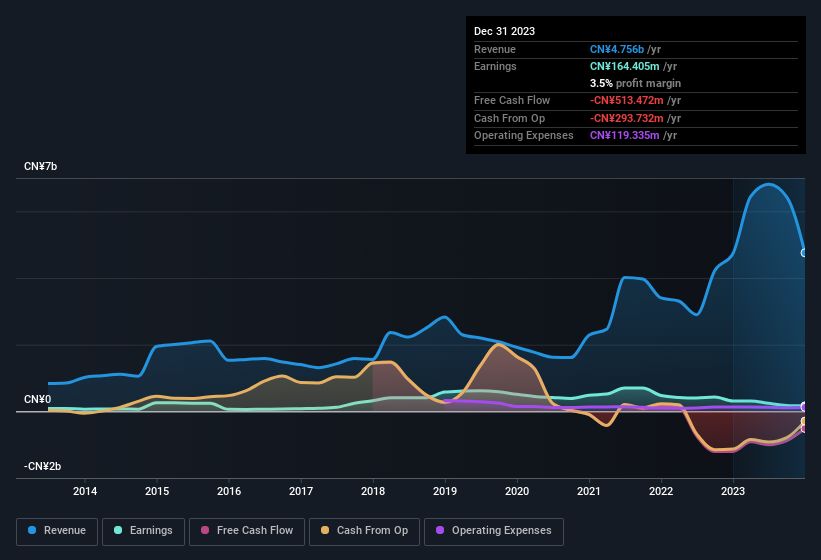

The market was pleased with the recent earnings report from Wolong Resources Group Co., Ltd. (SHSE:600173), despite the profit numbers being soft. Our analysis suggests that investors may have noticed some promising signs beyond the statutory profit figures.

尽管利润数字疲软,但市场对卧龙资源集团有限公司(SHSE: 600173)最近的收益报告感到满意。我们的分析表明,除了法定利润数字外,投资者可能已经注意到一些令人鼓舞的迹象。

Examining Cashflow Against Wolong Resources Group's Earnings

根据卧龙资源集团的收益研究现金流

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

许多投资者尚未听说过现金流的应计比率,但它实际上是衡量公司在给定时期内自由现金流(FCF)在多大程度上支持利润的有用指标。为了获得应计比率,我们首先从一段时期的利润中减去FCF,然后将该数字除以该期间的平均运营资产。该比率向我们显示了公司的利润超过其FCF的程度。

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

因此,当公司的应计比率为负时,这实际上被认为是一件好事,但如果其应计比率为正,则是一件坏事。虽然正应计比率表明非现金利润达到一定水平不是问题,但高应计比率可以说是一件坏事,因为它表明纸面利润与现金流不匹配。引用Lewellen和Resutek在2014年发表的一篇论文,“应计额较高的公司将来的利润往往会降低”。

For the year to December 2023, Wolong Resources Group had an accrual ratio of 0.23. Unfortunately, that means its free cash flow fell significantly short of its reported profits. Over the last year it actually had negative free cash flow of CN¥513m, in contrast to the aforementioned profit of CN¥164.4m. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of CN¥513m, this year, indicates high risk. Having said that, there is more to the story. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

在截至2023年12月的一年中,卧龙资源集团的应计比率为0.23。不幸的是,这意味着其自由现金流远低于其报告的利润。在过去的一年里,它实际上有 负面的 自由现金流为5.13亿元人民币,而上述利润为1.644亿元人民币。在去年自由现金流为负的背景下,我们想象一些股东可能会怀疑其今年5.13亿元人民币的现金消耗是否表明存在高风险。话虽如此,故事还有更多。应计比率至少部分反映了不寻常项目对法定利润的影响。

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Wolong Resources Group.

注意:我们始终建议投资者检查资产负债表的实力。点击此处查看我们对卧龙资源集团的资产负债表分析。

How Do Unusual Items Influence Profit?

不寻常的物品如何影响利润?

Wolong Resources Group's profit suffered from unusual items, which reduced profit by CN¥90m in the last twelve months. If this was a non-cash charge, it would have made the accrual ratio better, if cashflow had stayed strong, so it's not great to see in combination with an uninspiring accrual ratio. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. If Wolong Resources Group doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

卧龙资源集团的利润受到不寻常项目的影响,在过去的十二个月中,利润减少了9000万元人民币。如果这是非现金支出,如果现金流保持强劲,本来可以改善应计比率,因此,再加上平淡无奇的应计比率,就不太好了。尽管由于不寻常项目而产生的扣除首先令人失望,但有一线希望。我们调查了数千家上市公司,发现不寻常的物品本质上往往是一次性的。而且,毕竟,这正是会计术语的含义。如果卧龙资源集团不看到这些不寻常的支出重演,那么在其他条件相同的情况下,我们预计其利润将在来年增加。

Our Take On Wolong Resources Group's Profit Performance

我们对卧龙资源集团盈利表现的看法

In conclusion, Wolong Resources Group's accrual ratio suggests that its statutory earnings are not backed by cash flow, even though unusual items weighed on profit. Based on these factors, it's hard to tell if Wolong Resources Group's profits are a reasonable reflection of its underlying profitability. So while earnings quality is important, it's equally important to consider the risks facing Wolong Resources Group at this point in time. When we did our research, we found 4 warning signs for Wolong Resources Group (2 are a bit unpleasant!) that we believe deserve your full attention.

总之,卧龙资源集团的应计比率表明,尽管不寻常的项目打压了利润,但其法定收益没有现金流支持。基于这些因素,很难判断卧龙资源集团的利润是否合理地反映了其潜在的盈利能力。因此,尽管收益质量很重要,但考虑卧龙资源集团目前面临的风险同样重要。当我们进行研究时,我们发现卧龙资源集团有4个警告标志(2个有点不愉快!)我们认为值得你全神贯注。

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

在这篇文章中,我们研究了许多可能损害利润数字效用的因素,以此作为企业的指南。但是,还有很多其他方法可以让你对公司的看法。有些人认为高股本回报率是优质业务的好兆头。因此,你可能希望看到这份免费收藏的拥有高股本回报率的公司,或者这份内部人士正在购买的股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。