4月17日,摩根士丹利分析师Rie Nishihara领导的团队在报告中指出,对企业盈利而言,日元贬值通常是利好因素。如果日元持续疲软,美元兑日元汇率维持在155的高位,

4月17日,摩根士丹利分析师Rie Nishihara领导的团队在报告中指出,对企业盈利而言,日元贬值通常是利好因素。如果日元持续疲软,美元兑日元汇率维持在155的高位,Morgan Stanley believes that a fall below 152 of the yen exchange rate will be a turning point in the Japanese stock trend and will have three major negative effects: 1. The impact on consumer spending; 2. The widening gap between export companies and domestic demand companies is particularly unfavorable to small and medium-sized enterprises; 3. The return rate for overseas investors will decline.

Expectations of the Federal Reserve's interest rate cuts fell again and again, and the spread between the US and Japan rose. The US dollar hit a record high against the Japanese yen this week since 1990. As of press release,$USD/JPY (USDJPY.FX)$The exchange rate is 154.255, and market intervention in the Bank of Japan's re-entry into the market continues to heat up.

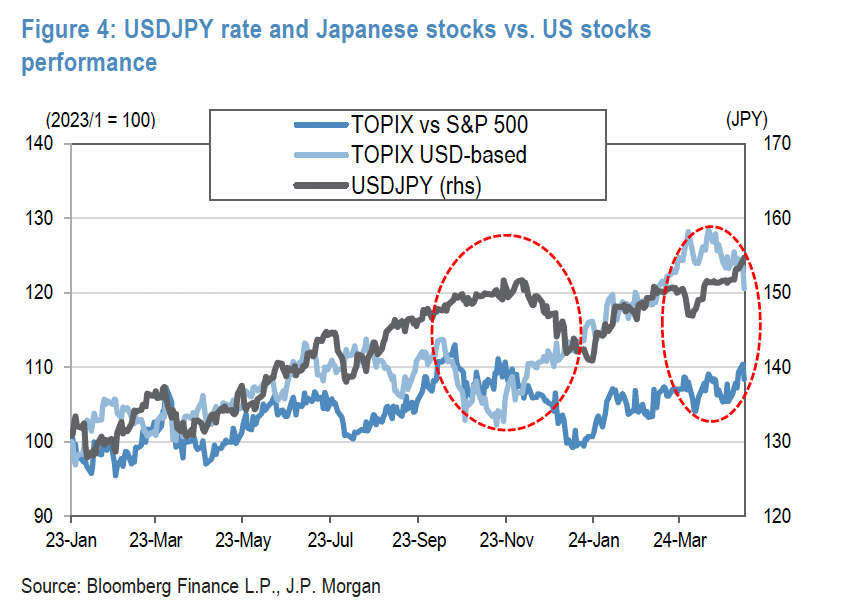

Since 2023, the sharp depreciation of the yen has pushed up the pricing of Japanese stocks, making yen assets a global value depression and attracting overseas capital to flow into Japanese stocks. So now the question is, if the yen continues to depreciate, how much momentum will there be for Japanese stocks to rise?

On April 17, a team led by Morgan Stanley analyst Rie Nishihara pointed out in a report that the depreciation of the yen is usually a favorable factor for corporate profits. If the yen continues to weaken and the USD/JPY exchange rate remains at a high level of 155, the profit expectations of Japanese companies may rise due to exchange rate factors, shifting from a decline in current forecasts to growth.

On April 17, a team led by Morgan Stanley analyst Rie Nishihara pointed out in a report that the depreciation of the yen is usually a favorable factor for corporate profits. If the yen continues to weaken and the USD/JPY exchange rate remains at a high level of 155, the profit expectations of Japanese companies may rise due to exchange rate factors, shifting from a decline in current forecasts to growth.

However, Morgan Stanley stressed that when the yen exchange rate fell below 152, the Japanese stock market began to outperform the US stock market, which may have a negative impact on the Japanese stock market. The excessive weakening of the yen has had the following three major adverse effects on the stock market: first, the impact on the real economy (that is, consumer spending); the second is the widening gap between enterprises and households, and between export companies and domestic demand companies, which is particularly bad for small and medium-sized enterprises; and third, the return rate of overseas investors has declined.

On the same day, Ken Kobayashi, chairman of the Japan Chamber of Commerce and Industry, said at a press conference that Japan's financial authorities should consider coordinating foreign exchange intervention with other countries to support the yen. Kobayashi pointed out that Japanese SMEs are suffering from rising costs of imported raw materials because the exchange rate of yen against the US dollar hit its lowest point in nearly 34 years.

The weakening yen boosted corporate performance to a certain extent

Morgan Stanley believes that it will be difficult for inflation to fall or keep US interest rates high for a long time, which means that the yen will continue to weaken. On the one hand, the depreciation of the yen will reduce the export costs of Japanese exporters, such as manufacturing companies and electronic equipment companies, and will drive corporate profit growth. Japanese companies' profit expectations may rise due to exchange rate factors:

Judging from the linear relationship between the yen exchange rate and corporate profit, the EPS and yen exchange rate of the earnings per share of the constituent stocks of the Japan Tokyo Stock Exchange Index shows that every time the yen exchange rate falls (that is, depreciates) by a certain margin, corporate profits will improve by a certain percentage.

If the USD/JPY exchange rate actually remains at 155 yen in fiscal year 2024, it is estimated that EPS will receive a boost of about 8% based on the fixed sensitivity assumption described above.

Judging from the 2023 net profit rankings of listed Japanese companies, the performance of leading Japanese companies is basically related to overseas revenue. In particular, the Japanese automobile industry, represented by Toyota, is expected to increase net profit to 2.9 trillion yen in fiscal year 2023, accounting for 60% of the increase in net profit from Japanese stocks. Take Toyota as an example. The yen depreciated in fiscal year 2023 (23.04-24.03), and Toyota expects that depreciation will increase profits by about 540 billion yen.

Therefore, Morgan Stanley believes that under a scenario where the yen is weak for a long time, the strong US economy will continue to be driven by overseas demand, and that the performance of companies driven by external demand will outperform those related to domestic demand in Japan.

The yen exchange rate reached 152 or a turning point in the trend of Japanese stocks

However, Morgan Stanley emphasized in another report that if the yen depreciates more than the US dollar against the yen exchange rate of 152, it may turn into a negative factor in the Japanese stock market. If the exchange rate of the US dollar against the yen exceeds 157, the increase in import prices due to the depreciation of the yen may completely offset the increase in real wages.

According to the report, excessive depreciation of the yen may have a negative impact on the Japanese economy and stock market through the following channels: (1) negatively impact the real economy (households and small and medium-sized enterprises) by curbing consumption; (2) widening the gap between enterprises and households, export companies and domestic demand enterprises, which is particularly bad for small and medium-sized enterprises; and (3) reducing the dollar-denominated return of overseas investors:

First, we believe that the real economy will be adversely affected, as rising prices of imported goods depress the real income of households. Based on the sensitivity of import cost inflation to the US dollar to the yen exchange rate so far, we have calculated that 157 yen is a break-even exchange rate, that is, the 3.7% basic wage increase decided in spring wage negotiations was completely offset by import cost inflation (actual wages did not rise). In other words, if the yen depreciates more than 157 yen between the US dollar and the yen, actual income will not rise or may even fall as a result of the spring wage increase agreement, which will seriously drag down the Japanese economy and the Japanese stock market.

The second reason is the problem of the widening gap between businesses and households and between businesses. Excessive depreciation of the yen is beneficial to exporting companies, but it is bad for households, widening the gap between businesses and households. We expect that the negative impact on small and medium-sized enterprises will be particularly serious. SMEs account for 99.7% of the total number of Japanese companies and account for 70% of the number of employees, so if the burden of excessive depreciation of the yen increases the pressure to raise wages, it may drag down the overall economy.

The third reason is the decline in the return of overseas investors in the Japanese stock market in dollar terms. The market still expects the yen to appreciate (as of April 17, the market generally expects the USD/JPY exchange rate to be 143 yen by the end of 2024), and we believe that most global investors will not invest in the Japanese stock market on the basis of hedging currencies. When overseas investors bought large amounts of Japanese stocks in January-February, the exchange rate of the US dollar to the yen was 140-150 yen. Due to the depreciation of the yen, the return on investment in US dollars fell by about 6%.

edit/new