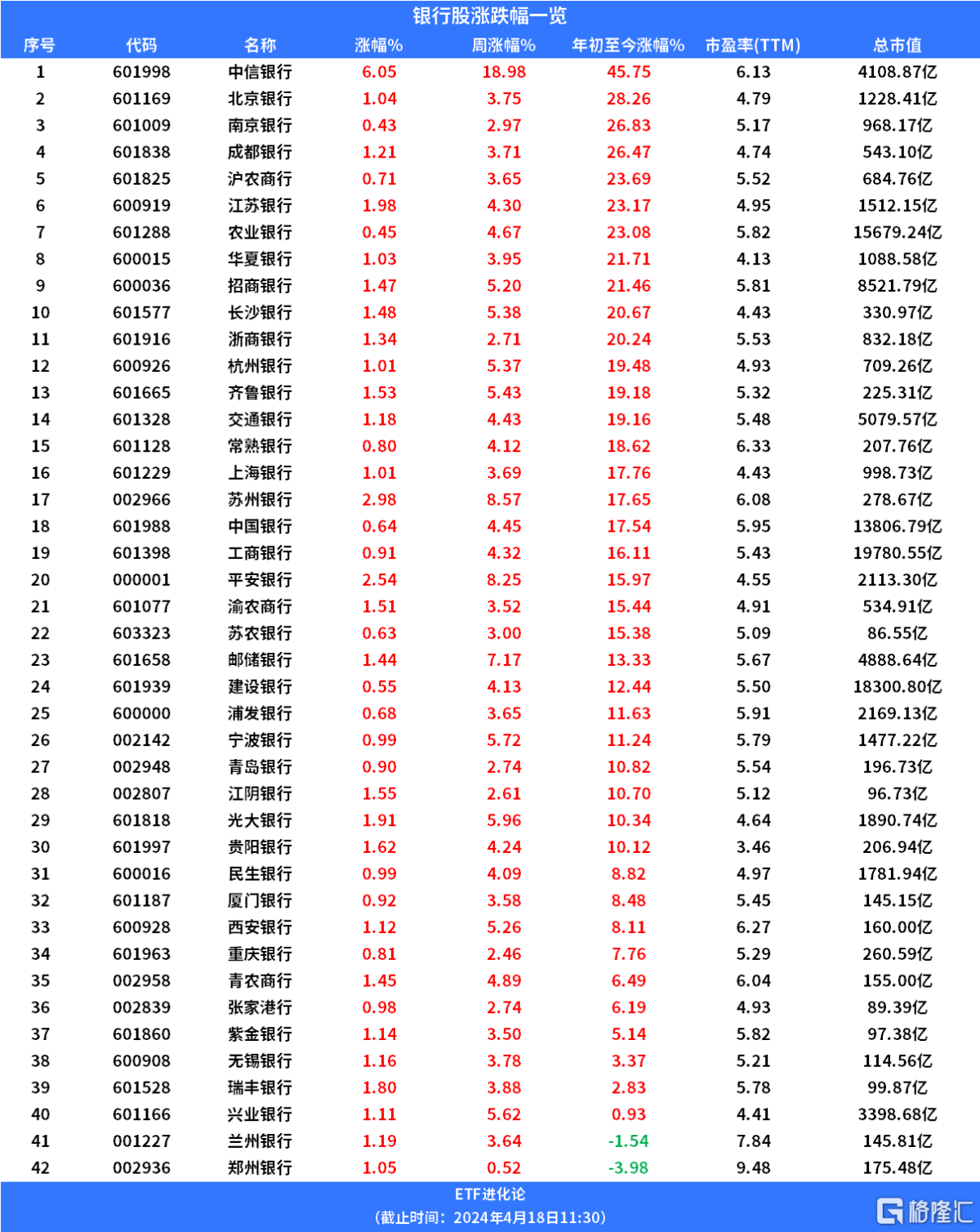

The banking sector rose, with 42 bank stocks collectively flourishing. China CITIC Bank rose more than 6%. Bank of Jiangsu, Agricultural Bank, Zheshang Bank, Everbright Bank, Bank of Communications, etc. followed suit. The stock prices of China CITIC Bank, China Construction Bank, Bank of China, and Agricultural Bank hit record highs in the intraday period.

In terms of ETFs, the China Merchants Fund Bank ETF preferred to increase by more than 2%. Bank ETF Tianhong, Bank ETF E-Fangda, Wells Fargo Fund ETF, Bank ETF Huaxia, Wells Fargo Fund ETF, Penghua Fund, China Securities Bank ETF, China Southern Fund Bank ETF, Hua'an Fund Bank ETF Index Fund, Huatianfu Fund Banking ETF, and Huabao Fund Bank ETF rose.

Bank ETF Tianhong, bank ETF E-Fangda, bank ETF Huaxia, and banking ETF have increased by more than 17% this year.

Bank ETFs track the China Securities Bank Index. The China Securities Bank Index selects securities of listed companies belonging to the banking industry from the Shanghai and Shenzhen markets, reflecting the performance of the banking industry. There are 42 constituent stocks, including China Merchants Bank, Industrial and Commercial Bank, Bank of Communications, Bank of Jiangsu, Agricultural Bank, Ping An Bank, Minsheng Bank, Bank of China, Bank of Beijing, etc.

The top ten weights of the China Securities Bank Index

Huijin bought bank stocks to inject strength into the market. On the evening of April 12, the four major state-owned banks, Industrial and Commercial Bank, Agricultural Bank, Bank of China, and China Construction Bank, issued an announcement stating that as of April 10, the controlling shareholder Central Huijin Investment Co., Ltd. (“Huijin Company”) had increased its holdings by 287 million shares, 401 million shares, 330 million shares, and 714.51 million shares through the Shanghai Stock Exchange trading system, totaling more than 1 billion shares.

Earlier, on October 11, 2023, ICBC, Agricultural Bank, Bank of China, and China Construction Bank issued separate announcements stating that they were increased by the controlling shareholder Central Huijin Investment Co., Ltd. As a controlling shareholder, the increase in Huijin's holdings shows the firm confidence of state-owned capital in developing financial enterprises and maintaining market stability.

Looking at the fundamentals of bank stocks, Huachuang Securities compiled the results of 21 banks that disclosed their results as of the end of the first quarter.

As of March 31, 2024, 21 of the 42 listed banks have disclosed their 2023 reports. Of these, 6 state-owned banks have already disclosed their 2023 reports, with the exception of SPF and Huaxia, 9 listed stock banks have disclosed their 2023 reports (SPF has disclosed express reports), 3 urban commercial banks have disclosed their annual reports (Qingdao, Chongqing, Zhengzhou), and 5 agricultural commercial banks have disclosed their annual reports (Changshu, Wuxi, Jiangyin, Ruifeng, Chongqing).

List of bank performance growth rates disclosed in annual reports (as of the first quarter of 2024)

The cumulative revenue growth rate remained stable throughout the year, and other non-interest income supported revenue. According to the disclosed annual reports of 21 listed banks, the overall revenue and profit due to mother growth rates of 21 banks in 2023 were -0.9% and 1.6%, respectively. The revenue growth rate was the same as in the previous three quarters, while the profit growth rate declined by 1.1 pct.

Among them, the sectors where the revenue growth rate weakened marginally compared to the previous three quarters were state-owned banks (cumulative growth rate -0.1 pct) and agricultural and commercial banks. The revenue growth rate of stock banks and urban commercial banks was marginally higher than in the third quarter. In particular, Bank of Qingdao and Bank of Chongqing, the cumulative revenue growth rate increased 5.3 pct and 2.0 pct to 7.1% and -1.9%, respectively. Bank of Qingdao had strong interest spreads and resilience in the fourth quarter of '22. growth.

Most national banks achieved negative annual revenue growth under downward pressure from interest spreads. Among China stock banks, banks that achieved positive annual revenue growth include Bank of China (+6.4%), Bank of China (+4.3%), Postbank (+2.3%), Bank of Communications (+0.3%), and Agricultural Bank (+0.0%).

Listed bank performance attribution

The cumulative growth rate on the profit side declined slightly, mainly due to a marginal weakening due to fewer provisions and increased efforts. With the marginal weakening of the positive contribution of provisions to profits, the profit growth rate of most banks declined compared to the previous three quarters. The banks that marginally increased their profit growth rate compared to the previous three quarters include Bank of China, Minsheng Bank, Bank of Chongqing, and Bank of Jiangyin. The cumulative profit growth rate of some banks declined by more than 5 pct. Mainly, some stock banks consolidated their provision plans for non-credit assets.

Net interest spreads are still a drag on performance growth, making it difficult to make up for the volume. The reduction in other non-interest income and provisions is the main driving factor supporting profit growth.

Overall, the biggest suppressing factor on the overall revenue of the banking industry in 2023 is still interest spreads. Judging from the annual reports of 21 listed banks, the narrowing of net interest spreads dragged down profit growth by -14.6%, and the overall annual scale increase was +11.8%. Net interest income was still -2.8% year-on-year for the whole year, and the growth rate fell 0.9 pct month-on-month, making it difficult to make up for the volume.

Furthermore, under the influence of the continuous decline in interest rates in the 2023Q4 bond market, compounded by the relatively low base in 2023Q4, other non-interest income increased by 28.5% year-on-year, and the growth rate increased by 13 pcts compared to the previous three quarters, which provided good support for the performance. Most banks continue to contribute positively to profits by reducing asset impairment losses. With the exception of Societe Generale, Everbright, and the Bank of Zhengzhou, which have increased their provision plans, all other bank provisions have fed back profits, and overall, agricultural and commercial banks are more aggressive.

By sector, handling fees and commission income have dragged down the performance of stock banks more clearly than the average of listed banks. Since 2023, demand for wealth management-related businesses such as funds and financial management has been insufficient, and escrow and underwriting rates have declined markedly. The agency insurance business, which performed relatively well in the first half of the year, was also affected by the “integrated reporting and banking” policy, and the share of revenue from stock banks is higher. The drag on in recent years is even more obvious. Overall net transaction fees and commission revenue for 21 banks in 2023 fell 6.4% year on year. The growth rate continued to decline by 2 pcts compared to the previous three quarters. Bank fee revenue is expected to continue to be under pressure in 2024. Agricultural and commercial banks are making more efforts to feed back profits. The overall provision coverage rate of agricultural and commercial banks remains high (all above 300%), and there is more room for backfeeding.

Regarding the banking industry, the Huachuang Securities Research Report stated:

The bank's continuous and stable dividends provide a sufficient safety cushion for investment bank stocks. Judging from the bank's historical dividend situation, the China Stock Bank's historical dividend level has remained above 30% for a long time, and China Merchants Bank and Ping An Bank exceeded expectations in 2023 and raised their dividend rates to 33.9% and 30%. Considering that the current overall asset quality of the industry has reached a historically high level, it provides a very sufficient safety cushion for future bank performance growth, and bank profit growth will remain steady in the future. Also, from the perspective of dividend rates, although the overall PB of the banking sector has risen from the previous low, it is still at the historical quantile level of 8.22%. The dividend rate is still 5.24%, and most of the dividend ratios for individual stocks are above 5%, which has long-term allocation value.

Looking ahead, in 2024, bank operations face the same changes, opportunities and challenges coexist. The overall operating fundamentals of listed banks are stable, profits are growing reasonably, and two main lines are proposed in terms of investment style:

1) Short-term allocation attributes: Focus on stable major banks+high quality regional commercial banks with high dividends. Under the operation of economic stocks, the market risk appetite is still mainly based on risk aversion. Individual bank stocks with “undervalization+high dividends” as “allotted” assets are still attractive to capital seeking steady returns, as well as long-term capital.

2) Long-term preferred business model: the bottom embraces core assets. After 1-2 years of adjustments, the current valuations of all types of banks within the banking sector have declined to historic lows. The valuations are all at their historical low levels, and there is limited room for further decline. For banks with excellent business models, valuations now tend to be reasonable or even undervalued, and their long-term fundamental performance and expectations have entered an appropriate allocation range.

Wanlian Securities released a research report stating that from a long-term perspective, the banking industry's overall profit growth may have entered the bottom range, and profit stability will gradually be reflected. Also, from the perspective of dividends, an increase in the dividend rate is conducive to an increase in bank stock valuations. However, due to cost-limited endogenous supplementation of the bank's own business model, it meets regulatory requirements for sufficient capital and promotes future business and scale expansion. Consider the current dividend rate and valuation level of bank stocks in a comprehensive manner. Short-term sector defensive properties are still quite obvious. The subsequent gradual recovery of the economy and improvement in credit risk may bring about a new round of market catalysis.