① Tencent Holdings was bought by Fu Pengbo, while Meituan was favored by Zhao Feng and Rao Gang; ② In terms of A-shares, the three fund managers had different preferences for old and new energy stocks.

Financial Services Association, April 18 (Reporter Zhou Xiaoya) Ruiyuan Fund's report card for the first quarter of 2024 revealed that buying Hong Kong stocks became the common choice of its fund managers.

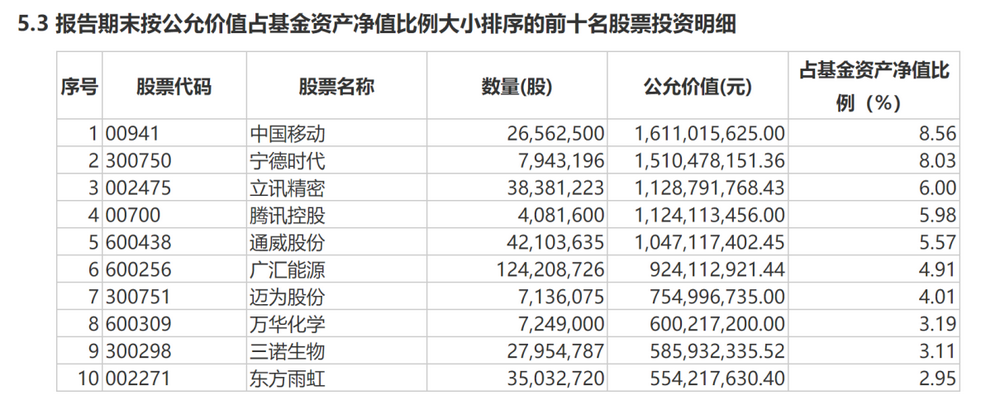

However, as the most heavily held stock, China Mobile Hong Kong shares were held and reduced by Ruiyuan Growth Value managed by Fu Pengbo and Zhu Yi, Ruiyuan Equilibrium Value managed by Zhao Feng for three years, and Ruiyuan Steady Progressive Allocation managed by Rao Gang and Hou Zhenxin for two years. Meanwhile, Tencent Holdings was bought by Fu Pengbo in the heavy stock market, while Meituan was favored by Zhao Feng and Rao Gang.

In terms of A-shares, the three fund managers have different preferences for old and new energy stocks. Fu Pengbo added a position on Guanghui Energy and reduced his holdings in the Ningde era, while Zhao Feng increased his position on the second-largest stock from the Ningde era.

Overall, the scale of the three products has shrunk. By the end of March this year, Ruiyuan's growth value had fallen back to the 20 billion yuan mark, to 18.813 billion yuan; Ruiyuan's three-year equilibrium value and Ruiyuan's two-year stable allocation holdings were 11.83 billion yuan and 8.424 billion yuan respectively. On January 29 of this year, Ruiyuan Fund purchased 50 million yuan for each of Ruiyuan's growth value and Ruiyuan's equilibrium value for three years.

Fu Pengbo: Taking the initiative to reposition heavy stocks, Tencent enters the top ten new heavy positions

According to Ruiyuan Growth Value's 2024 quarterly report, the stock position reached 90.25%, up 1.76 percentage points from the end of the previous quarter. The increase in Hong Kong stock positions was even more significant, rising from 17.67% at the end of last year to 20.11% at the end of the first quarter of this year, an increase of more than 2 percentage points.

Judging from the distribution of positions in the industry, Hong Kong stock positions in communication services, medical care and other industries have risen. Tencent Holdings Hong Kong Stock is the only new individual to enter the top ten largest stocks. The number of shares held was 4.0816 million shares, an increase of nearly 50% over the previous month. This is also another time since the 2019 interim report that Tencent Holdings was once again weighed by Ruiyuan's growth value.

San'an Optoelectronics withdrew from the top ten heavy-held stocks. The stock had previously been heavily traded for two and a half years. At the end of last year, it was the 7th most heavily held stock. Fu Pengbo and Zhu Yi also mentioned in the fund's quarterly report that in the first quarter, they mainly reduced their holdings of the top 20 companies with a net worth share.

China Mobile still maintains the top position, but the number of holdings decreased by 7.050,500 shares to 26.562,500 shares, and its share of holdings also declined to 8.56%. Furthermore, the number of shares held by the four major stocks, including Ningde Times, Tongwei Shares, Wanhua Chemical, and Dongfang Yuhong, has all declined.

However, not all heavy stocks have been reduced. The number of shares held by Lixun Precision, Guanghui Energy, and Maiwei shares have all increased. Fu Pengbo and Zhu Yi said that individual energy stocks bucked the trend and increased their holdings during the pullback. Furthermore, some companies benefiting from export chain growth and benefiting from equipment replacement upgrades were added from the bottom up. The number of shares held by Sannuo Biotech also increased slightly from month to month, but the share of holdings declined.

Looking ahead to the second quarter, they believe that the A-share market is still expected to have some structural opportunities, and the valuation level of sector indices is still below the historical average. With the disclosure of listed companies' annual reports and quarterly reports, improvements in fundamentals and changes in the economy in the second quarter may have a stronger and more clear guiding effect on investment throughout the year, and the mix will continue to be adjusted dynamically.

Zhao Feng: Reducing China Mobile's positions for 4 consecutive quarters, increasing the Ningde era

Similar to Fu Pengbo's move, Zhao Feng also reduced his holdings of China Mobile, the largest stock in the first quarter of this year. This is the fourth quarter in three consecutive years that Ruiyuan Equilibrium Value has reduced its holdings of this stock. As of the end of the first quarter of this year, the fund's holdings of China Mobile were 17.6 million shares, a decrease of 2.4 million shares over the previous month.

The number of shares held by individual stocks such as Tencent Holdings, Siyuan Electric, Sannuo Biotech, and China Resources Beer has also declined. Zhao Feng mentioned in a quarterly report that individual stock holdings have been reduced in companies related to fixed asset investment, as well as companies with unattractive static valuations and difficult to determine future growth.

Meanwhile, Ningde Times, Wanhua Chemical, and Weiming Environmental Protection were increased. The quarterly report shows that attractive valuations are the reason why some new energy companies have increased their holdings, while companies with low valuations and stable and predictable fundamentals have also increased their positions.

Overall, the fund's stock position up to the end of the first quarter of this year was generally consistent with the previous quarter, at 89.85%, and the Hong Kong stock position was slightly increased. Two individual stocks, including Meituan and China Financial Insurance, were bought into the top ten largest positions. From an industry perspective, Hong Kong stock positions in the consumer goods industry have increased.

Looking ahead to the later stages, Zhao Feng anticipates that as demand growth slows down, listed companies will be more rational about expansion and will pay more attention to profitability and shareholder returns, which will improve the profit quality and level of return of Chinese listed companies.

Rao Gang: Bond supply generally does not change the trend; we are optimistic about allocation value in the medium to long term

As a debt-biased hybrid fund, Ruiyuan's steady allocation for two years, managed by Rao Gang and Hou Zhenxin, showed a slight recovery in stock positions in the first quarter of this year, to 30.66%.

Rao Gang and Hou Zhenxin mentioned in the fund's 2024 quarterly report that during the liquidity shock in the equity market at the beginning of the year, on the one hand, when the prices of dividend assets and growth assets were greatly differentiated in the short term, the position structure was rebalanced according to the expected level of return. On the other hand, they also actively seized opportunities and increased positions in some high-quality targets with solid fundamentals and cheap valuations, thus increasing equity positions slightly compared to the end of last year.

Among them, the Hong Kong stock position increased significantly, from 13.99% at the end of last year to 17.71% at the end of the first quarter of this year. Specifically, Hong Kong stocks such as ICBC and Tencent Holdings were increased, and Meituan entered the top ten most heavily held stocks; China Mobile's Hong Kong stock holdings declined, but the share of holdings increased month-on-month. In terms of A-shares, Baosteel, Ningde Era, and Tonglian Precision have also increased their holdings.

In terms of debt conversion, the fund's position declined slightly. The main thing is that the utility convertible bonds previously held for a long time met the conversion conditions in stages as the underlying shares rose, so the reduction in holdings achieved good returns. Currently, it still mainly holds undervalued debt conversion types.

In terms of pure debt, Rao Gang mentioned that after long-term interest rates declined markedly in the first quarter, the leverage and longevity of bond assets was moderately reduced. In his view, although special treasury bonds will be issued around the second quarter, and the choice of issuance method may have a phased impact on the market, bond supply generally does not change the trend, and bond assets still have good allocation value in the medium to long term.

Looking ahead to the future market, he said that in the case where the rate of government bond issuance within the first quarter budget is low, the second quarter may gradually move closer to normal seasonality, thereby increasing the degree of fiscal influence on economic momentum. The transmission chain of “bond issuance - fiscal expenditure - physical workload” is also worth paying attention to.