① On Tuesday, Federal Reserve Chairman Powell's latest “hawkish” speech gave the US Treasury yield another dose of adrenaline; ② As the “quiet period” before the Fed's May monetary policy meeting officially begins this weekend, the delay in the Fed's interest rate cut during the year has almost been “settled”...

Financial Services Association, April 17 (Editor: Xiaoxiang) On Tuesday, Federal Reserve Chairman Powell's latest “hawkish” speech gave another dose of adrenaline to soaring US Treasury yields. And as the “quiet period” before the Federal Reserve's May monetary policy meeting is about to officially begin this weekend, the delay in the Fed's interest rate cut during the year has almost been “settled”...

Federal Reserve Chairman Powell said at a panel discussion with Bank of Canada Governor MacLem at Washington Wilson Center on the same day that strong inflation in the first quarter brought new uncertainty about whether the Federal Reserve could lower interest rates this year without any signs of economic slowdown.

His speech suggested that after the CPI data was stronger than expected for the third month in a row, the Fed's outlook had clearly changed, which seemed to have dashed hopes that the Fed might pre-emptively take action to cut interest rates.

Federal Reserve officials have previously stated that they hope to have more confidence to prove that inflation is returning to target levels, and are optimistic that another month or two of data may reach this standard.

Powell said in his latest speech on Tuesday that recent data clearly did not give us more confidence; on the contrary, these data suggest that it may take longer than expected to gain that confidence. If the inflation rate continues to rise above the Fed's 2% target, the Fed is likely to keep interest rates at current levels for a longer period of time.

Powell also said, “We think the policy is ready to deal with the risks we face. Right now, given the strong job market and the progress made so far in terms of inflation, it is appropriate to allow more time for restrictive policies to work.”

This is Powell's first public speech since both non-farm payrolls and CPI surpassed expectations in March. At the same time, it was his last public appearance before the Federal Reserve's May interest rate meeting.

There is no doubt that Powell's above statement is in stark contrast to what he said at the congressional semi-annual hearing in March. Powell threatened at the time that Federal Reserve officials were “not far away” from gaining the confidence needed to lower interest rates in the middle of the year. One or two more positive price readings may be enough for officials to conclude that interest rates can be readjusted to a lower level.

Now, after a series of hot US inflation reports and economic data, Powell's “confidence” also seems to have been erased quite a bit.

It is worth mentioning that prior to Powell's speech, Federal Reserve Vice Chairman Jefferson also pointed out overnight that with interest rates maintained at current levels, inflation is expected to continue to slow down, but if inflationary pressure continues, it is necessary for interest rates to remain high.

Jefferson said that although considerable progress has been made in reducing inflation, the task of the Federal Reserve to keep the inflation rate reaching the 2% target is “unfinished.”

Interest rate market pricing is becoming more and more believable: the delay in interest rate cuts has been “settled”

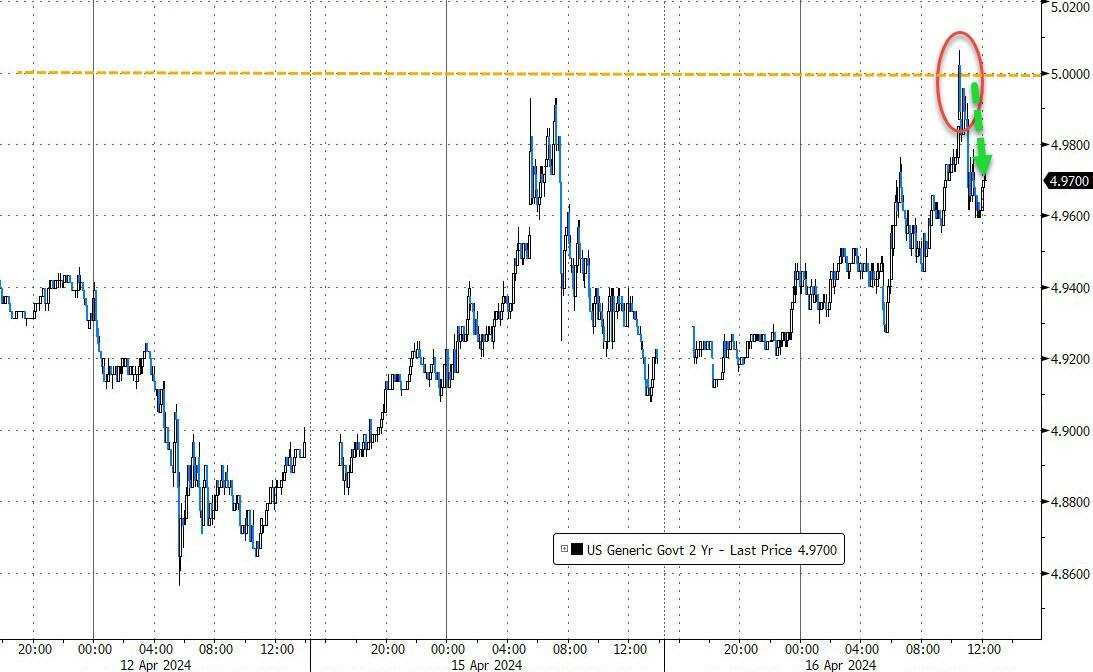

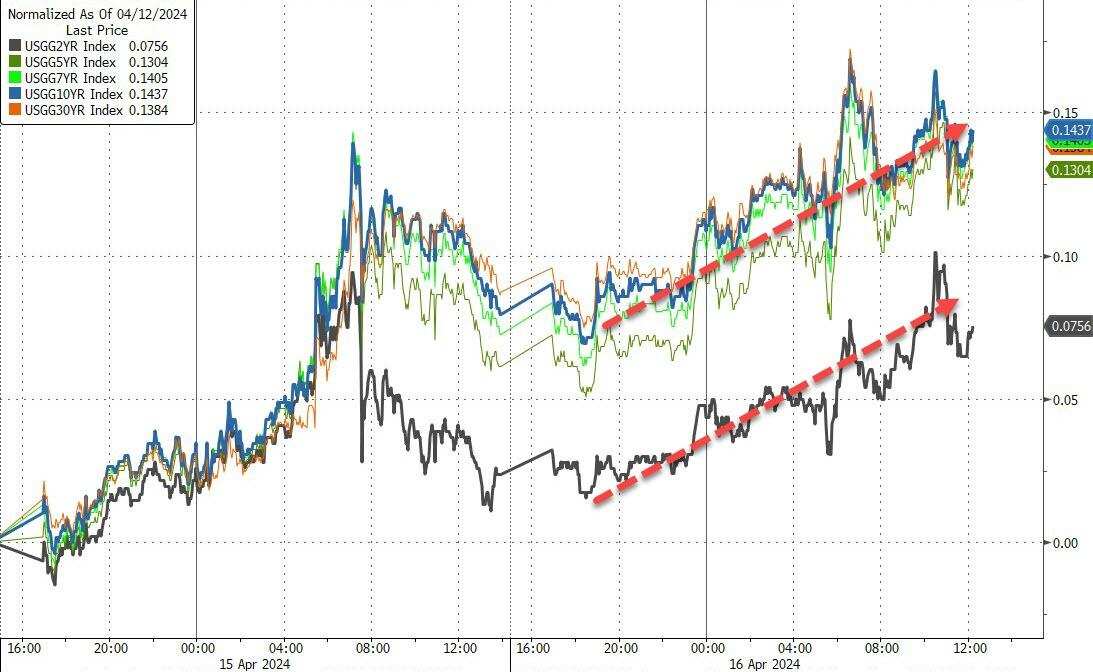

After Powell hinted that the Federal Reserve would not rush to cut interest rates, overnight US bond yields continued to hit new highs during the year. The 2-year US bond yield once again rose to 5% intraday, reaching the highest level since November last year. Interest rate swap contract traders linked to the Federal Reserve session expect further easing to decrease this year.

By the end of the New York session, the 2-year US Treasury yield had risen 1.8 basis points to 4.929%, the 5-year US Treasury yield had risen 5.8 basis points to 4.625%, the 10-year US Treasury yield had risen 7.8 basis points to 4.607%, and the 30-year US Treasury yield had risen 8.5 basis points to 4.72%.

Previously, the 2-year US Treasury yield once broke through the 5% mark on April 11, but the PPI data released later stopped the decline in treasury bonds caused by the CPI the day before. In October of last year, the 2-year US Treasury yield hit a high of 5.257%, the highest level since 2006. At the time, traders believed that the Federal Reserve might maintain high interest rates for a long time.

George Goncalves, head of US macro strategy at Mitsubishi UFJ Financial Group, said that the market is clearly weak and will not counter any hawkish signal.

Evercore analyst Krishna Guha said, “Powell's remarks clearly indicate that the Federal Reserve is now looking ahead to the situation after June. His remarks are consistent with 'Plan B', which began cutting interest rates twice in July this year, but there is also a possibility that continued disappointment with inflation may cause interest rates to last longer.”

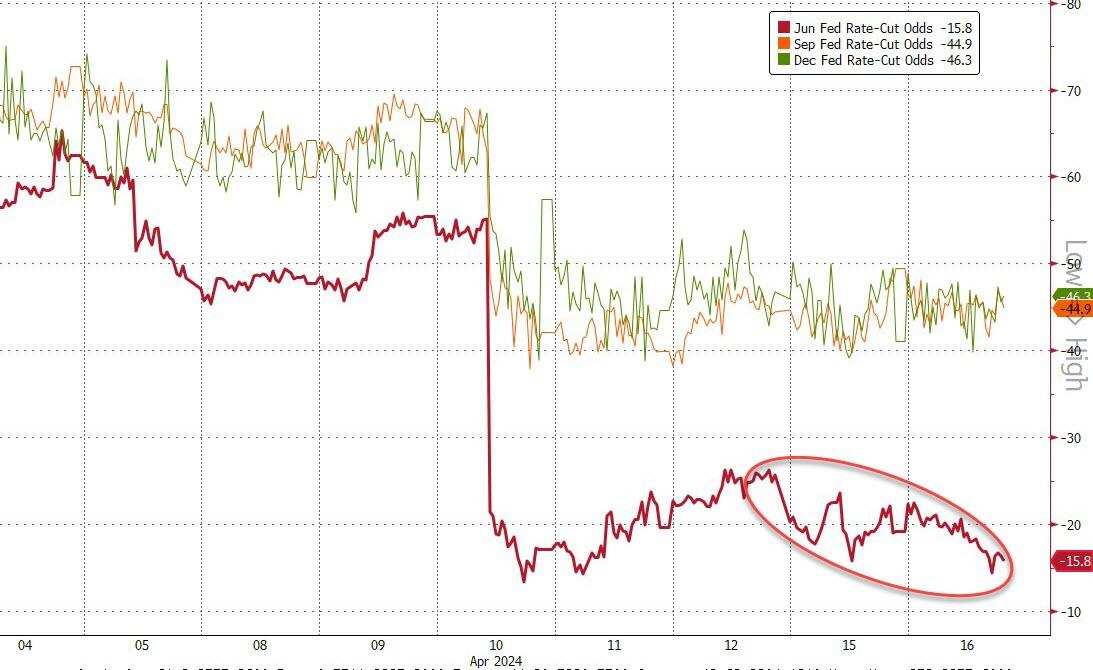

Market expectations for the Fed to cut interest rates declined further after Powell's latest comments. Interest rate market traders currently expect interest rate cuts of about 38 basis points during the year, lower than 43 basis points at the close of Monday. The probability of interest rate cuts in June has also been reduced to only 15%!

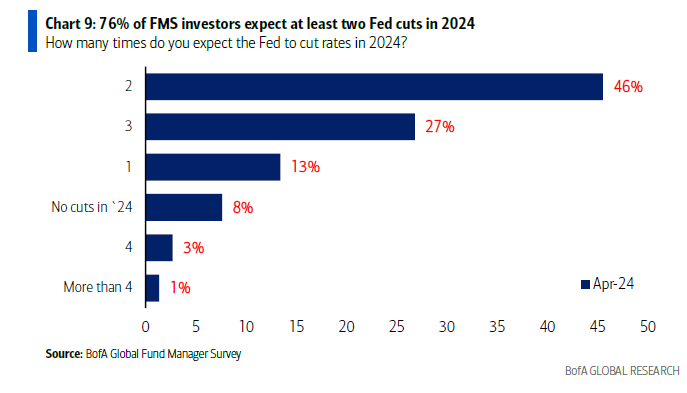

According to the latest monthly fund manager survey released by Bank of America on Tuesday, nearly half of the respondents now expect only two interest rate cuts this year...

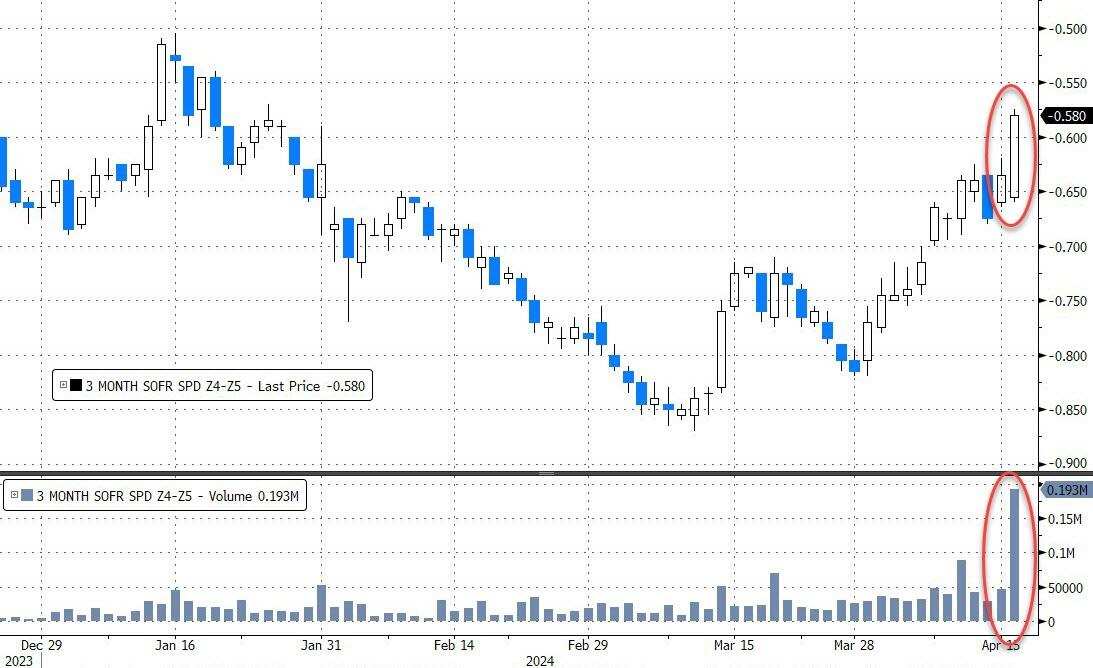

In fact, as expectations of interest rate cuts continue to subside overall, the prospects for even next year's interest rate cuts are now becoming even bleaker. The price comparison between the SOFR contract at the end of this year and the end of next year shows that the Federal Reserve's interest rate cut next year has also narrowed to 58 basis points; it has only been fully priced to cut interest rates twice.

Lawrence Gillum, chief fixed income strategist at LPL Financial, said that since last week's inflation data was higher than expected, investors in the bullish US bond market have been almost speechless, which has increased the market's attention to the statements made by Fed policymakers. Gillum said, “No one wants to stand on the opposite side of the current trend, which means that yields are likely to continue to rise.”

Tom Porcelli, chief US economist at PGIM Fixed Income, pointed out, “The market is very sensitive to monthly data no longer meeting expectations. If we believe that the improvement in inflation will not be linear, then we must adapt to volatile market conditions.”

Editor/Somer