① In the first quarter, Xinhua Insurance achieved original premium income of 57.193 billion yuan, a year-on-year increase of -11.7%; ② In the first quarter, the comprehensive cost ratio of People's Insurance, Ping An Insurance, and Taibao Insurance may increase slightly year-on-year; ③ The industry expects a slight negative increase in net profit from listed insurers in the first quarter.

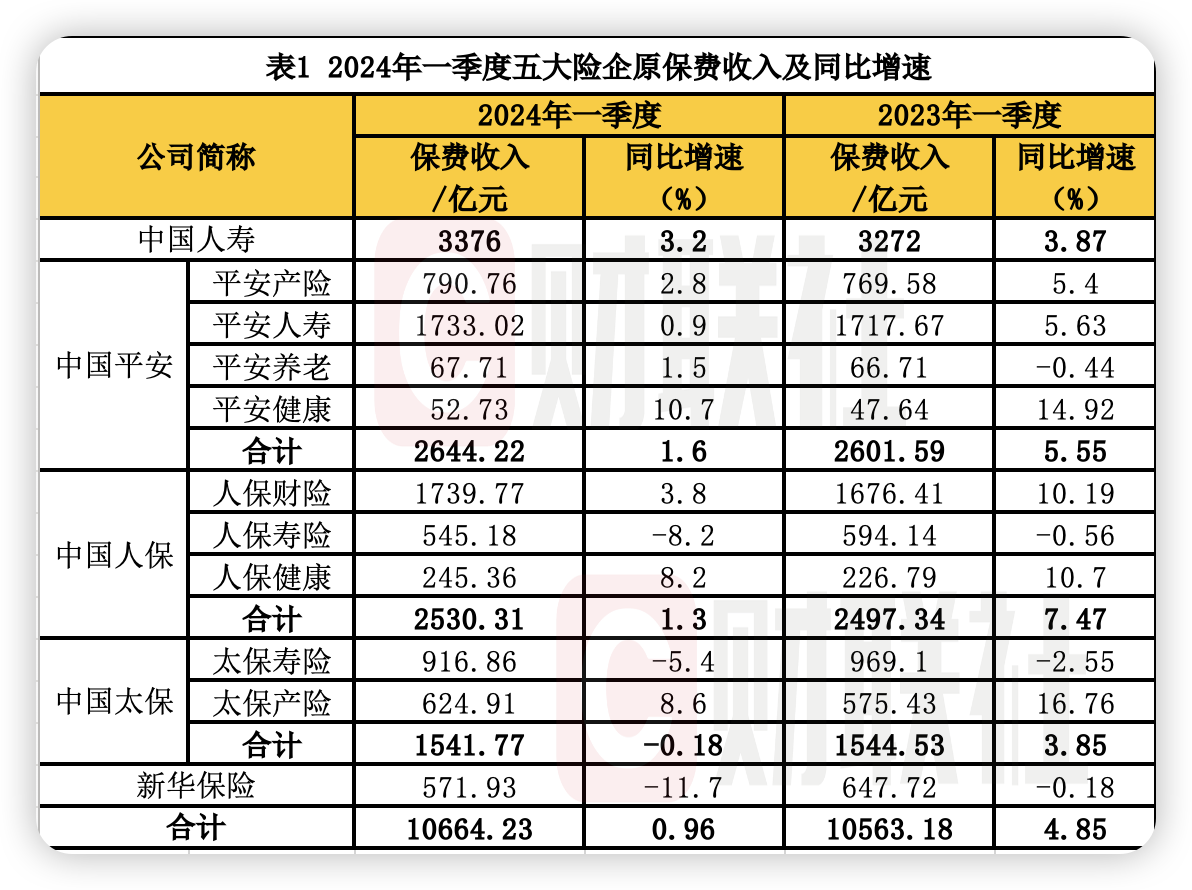

Financial Services Association, April 16 (Reporter Xia Shuyuan) Premium data for the first quarter of the top five A-share insurers has been released. According to statistics from the Finance Association reporter, the five A-share listed insurers obtained a total of 1066.423 billion yuan in original premium income, an increase of 0.96% over the previous year.

Specifically, the premium income of the five companies showed a “three rise and two drop” pattern. Among them, China Life Insurance, and China People's Insurance achieved original premium income of 337.6 billion yuan, 264.422 billion yuan, and 253,031 billion yuan respectively, corresponding to year-on-year growth rates of 3.2%, 1.6%, and 1.3%; China Taibao and Xinhua Insurance's original premium income was 154.177 billion yuan and 57.193 billion yuan, with year-on-year growth rates of -0.18% and -11.7%.

In terms of life insurance, the five companies Ping An Life, China Life Insurance, Taibao Life Insurance, and People's Insurance achieved a total original premium income of 714.299 billion yuan, a year-on-year decrease of 0.8%; in terms of financial insurance, the three companies, People's Insurance, Ping An Industrial Insurance, and Taibao Financial Insurance, achieved a total of 315.544 billion yuan in original premium income, an increase of 4.4% over the previous year.

Industry insiders predict that the top five A-share insurers were dragged down by equity market fluctuations in the first quarter, putting pressure on their net profit to their mother. On the one hand, after experiencing a correction in January, the equity market picked up in February-March, but the level of increase was still lower than the same period last year; on the other hand, the yield on 10-year treasury bonds fell to 2.29% in the first quarter. Bond assets included in current profit and loss financial assets are expected to reap good returns, partially hedging the decline in equity market earnings.

Against this background, the industry expects the net profit of the five insurers to increase slightly negatively in the first quarter, namely China Taibao -5.8%, China Ping An -10%, Xinhua Insurance -13.2%, China China Insurance -14.6%, and China Life Insurance -16.6%, respectively.

In the first quarter, the premiums of the top five personal insurance companies were “two rises and three drops”, and Xinhua Insurance continued its negative double-digit growth

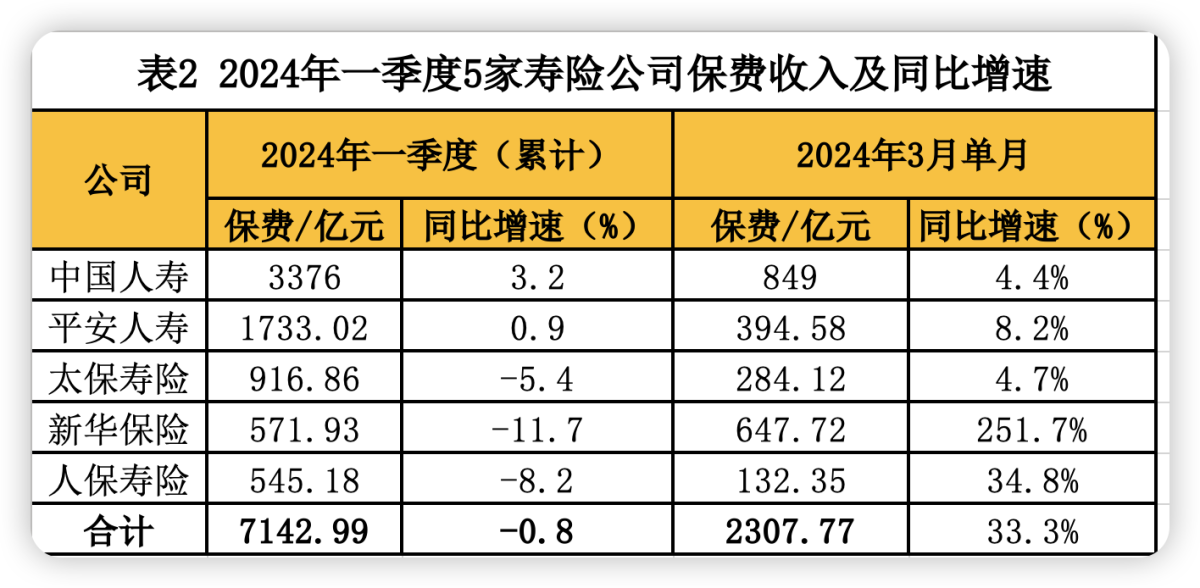

In the first quarter, the five major A-share personal insurance companies had a total original premium income of 714.299 billion yuan, an increase of -0.8% over the previous year.

Specifically, the five companies' premium income showed a “two rise and three drop” trend. Among them, China Life Insurance and Ping An Life achieved original premium income of 337.6 billion yuan and 173.3 billion yuan respectively, corresponding growth rates of 3.2% and 0.9%.

Taibao Life Insurance, Xinhua Insurance, and People's Insurance achieved original premium income of 91,686 billion yuan, 57.193 billion yuan, and 54.518 billion yuan respectively, with corresponding growth rates of -5.4%, -11.7%, and -8.2%, respectively.

However, looking at the single month of March, the five companies achieved total original premium income of 23.777 billion yuan, an increase of 33.29% over the previous year. Among them, Xinhua Insurance's original premium income in March was 64.772 billion yuan, an increase of 2.5 times over last year.

Xinhua Insurance said, “In March, premium income increased sharply from month to month, the scale and value of the individual insurance channel business increased, and the premium income structure was well optimized and improved. The company's business strategy for the first quarter focused on value growth and optimization of the business structure, and the year-on-year decline in cumulative insurance premium income narrowed.”

In response to the sharp increase in premiums in a single month in March, Liu Xinqi, chief financial analyst at Guotai Junan Securities, analyzed that in March-April, small and medium-sized banks in many places followed up lowering deposit interest rates. It is expected that customers will have strong demand for insurance products with good payout properties to meet their capital protection and savings needs.

Looking at the channel, although the manpower of individual insurance teams has declined slightly, production capacity per capita continues to increase under the high-quality transformation of channels, further boosting the growth of new orders. In particular, some insurers will increase sales of long-term payment products, which will drive the improvement of individual insurance value rates. As far as banking insurance channels are concerned, reporting new orders will be pressured in the short term, and significant improvements in fee rates will help increase the value ratio of listed insurers.

As new orders and value ratios improve, the new business value of listed insurers is expected to achieve a double-digit year-on-year increase in the first quarter, namely China Taibao (31.1%) > Xinhua Insurance (29.1%) > China Life Insurance (21.2%) > China Ping An (17.3%).

Looking ahead to the second quarter, Liu Xinqi said, “Listed insurers will continue to promote wealth management products such as annuity insurance and increased lifetime life, and appropriately increase sales of 5/6 year payment products to meet customers' medium- to long-term savings regulations. At the same time, in order to promote the achievement of annual value targets, insurance companies will gradually switch to selling health insurance products with higher value rates.”

The premium growth rate of the three financial insurance companies narrowed year-on-year in the first quarter, and the comprehensive cost ratio may rise slightly year-on-year

In the first quarter, the “old three” financial insurance businesses grew steadily, achieving a total of 315.544 billion yuan in premium income, an increase of 4.4% over the previous year.

Specifically, the premium growth performance of the three companies was divided, and the growth rate was narrower than in the same period last year. Among them, Taibao Industrial Insurance achieved premium income of 62,491 billion yuan, leading the year-on-year growth rate of 8.6%, but down 8.16 percentage points from the 16.76% growth rate in the same period last year.

People's Insurance and Ping An Insurance achieved premium income of 173,977 billion yuan and 79.076 billion yuan respectively. Corresponding year-on-year growth rates were 3.8% and 2.8%, down 6.39 percentage points and 2.6 percentage points respectively.

Looking at insurance types, in the first quarter, People's Insurance Auto Insurance achieved a total premium income of 69.24 billion yuan, an increase of 1.9% over the previous year; non-car insurance premium income was 104.737 billion yuan, an increase of 5.04% over the previous year.

Among them, Yijian Insurance's premium income was 56.813 billion yuan, up 6.2% year on year; agricultural insurance premium income was 19.064 billion yuan, down 3.2% year on year; liability insurance premium income was 11.603 billion yuan, up 1.3% year on year; and credit guarantee insurance premiums were 1,741 billion yuan, up -7.6% year on year.

Qiu Jian, chief insurance researcher at the China United Insurance Group Research Institute, told the Finance Association reporter that overall, financial insurance premiums grew steadily in the first quarter, but the growth rate was narrower than in the same period last year. It was mainly affected by macroeconomic factors such as low consumer willingness to spend, compounded by leading companies implementing “integration of reporting and banking” and the decline in automobile sales.

It is worth noting that financial insurance companies' comprehensive payout rates increased in the first quarter due to increased compensation due to low temperatures, rain, snow, and freezing disasters. “In the first quarter, natural disasters in China were dominated by low temperature rain, snow and freezing disasters, earthquakes, and geological disasters. In particular, the worst low temperature rain, snow and freezing disaster occurred during the Spring Festival travel season since 2009. As a result, direct economic losses increased dramatically over the same period last year, and financial insurance companies' payout rates may have increased.”

In this context, the industry expects the comprehensive cost ratio of financial insurance to rise slightly year-on-year in the first quarter, respectively 96.3% for Human Insurance, up 0.6 percentage points; Taibao Financial Insurance 98.6%, up 0.2 percentage points year on year; and Ping An Insurance 99%, up 0.3 percentage points year on year.