Will the Federal Reserve cut interest rates again? The US government will not only have to pay trillions of dollars in interest in the future; it will not even be able to sell treasury bonds that have always been stable.

US CPI data last week triggered the market to sell off US bonds one after another. After the US Treasury's auction of 10-year treasury bonds cooled down, investors' sell-off of US bonds intensified further, driving 10-year US bonds to a high level of 4.5%.

If the Federal Reserve does not cut interest rates, the US government's debt issuance and financing environment will deteriorate further.

Interest on debt could become the biggest financial burden for the US government

Investors' first impression of the US CPI data last week is that inflation has not been completely contained, and the Federal Reserve may keep interest rates high in the next few months or even years.

James Aubin, Chief Investment Officer of Sierra Mutual Funds, said:

“The US CPI data for March, which exceeded expectations, changed investors' views on the direction of the Federal Reserve's policy, and the market's narrative logic changed.”

Interest rates that remain high for the US federal government mean that the interest costs of borrowing new bonds have remained high.

According to the US Congressional Budget Office (CBO), interest expenses on US Treasury bonds in fiscal year 2023 were as high as $659 billion. The trend of rising interest rates on US bonds will even continue. It is estimated that in the next ten years, the US government's total treasury bond interest expenditure will reach a record $12.4 trillion.

Bank of America analyst Michael Hartnett even predicted that interest on US debt will reach 1.6 trillion US dollars by the end of 2024, surpassing social security spending and becoming the largest single government expenditure.

According to Torsten Slok, chief economist at Apollo Global Management, a record $8.9 trillion in treasury bonds (about one-third of America's outstanding debt) will expire in 2024 alone.

In an environment of high interest rates, there is a lot of pressure on the US government to repay its debts.

The supply of US Treasury bonds is getting bigger and harder to sell!

The steady rise in debt and interest, compounded by the continuing fiscal deficit, has forced the US government to continue to issue debts and borrow money to fill the hole. The Federal Reserve's delay in cutting interest rates will worsen the US government's debt problem.

Bill Merz, head of capital market research at Bank of America, said:

“Since the US federal government has been in deficit for years, it can only be covered by issuing bonds. The current high level of interest rates has led to a rise in interest costs, forcing the US government to continue to increase the number of treasury bonds issued to finance.”

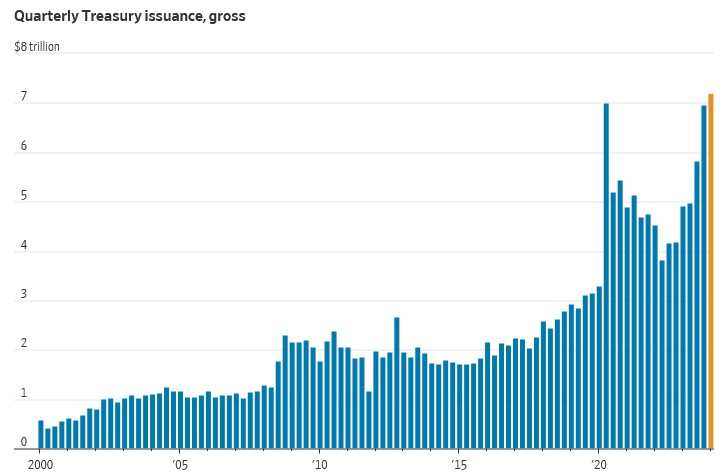

Since 2020, the US has been continuously freeing itself on the path of issuing bonds, and almost every quarter the guarantee costs 4 trillion dollars to be suppressed.

In the first quarter of this year, the US issued 7.2 trillion US dollars of treasury bonds, setting the highest quarterly bond issuance record in history. At the time, it had not even issued that many debts to cope with the impact of the COVID-19 pandemic.

As the issuance of US bonds accelerates, and there are even signs of oversupply, investors are almost unable to buy them.

This is one of the reasons why the US Treasury's auction of treasury bonds is getting cold recently.

The Federal Reserve, Japan, and Europe are all basic markets for buying US bonds

Although the recent auction of US bonds has taken a cold, and some investors chose to wait and see, the basic market for buying US bonds has always been around, such as the Federal Reserve, as well as Japanese and European investors.

Of America's $34 trillion debt, about 22% is government debt, and the remaining 78% is public debt. Of this portion of public debt, US creditors account for about 70%, and international creditors account for about 30%.

Among US creditors, the Federal Reserve is the biggest player; the rest are mutual funds, pension funds, banks, and insurance companies. However, the Federal Reserve's traditional art is to use QE and QT to control debt purchase plans, and then adjust the balance sheet to achieve the goal of controlling market liquidity.

Due to the recent signs of slowing down the contraction in the minutes of the March meeting of the Federal Reserve, FOMC members generally agree to halve the scale of the monthly downsizing. This is a small benefit for supporting the price of US bonds.

However, international investors such as Japan and Europe like to buy US bonds. On the one hand, it is because Japan and many countries in the Eurozone have long had trade surpluses with the US, and there is no place to store current account surpluses in US dollars. The most convenient thing is to go back and buy US debt. In addition to improving international relations, you can get some interest.

On the other hand, Japan and the European Central Bank have a year-round zero interest rate or even negative interest rate policy, so that the yield on their own bonds is far less than that of US treasury bonds. Their own bonds are uncontentious; they can only invest in the US. In particular, after the US experienced an interest rate hike cycle of nearly 2 years, the yield on 10-year US bonds has already exceeded 4%, and US bonds suddenly became fragrant.

The US Treasury Department is expected to announce the third quarter bond issuance plan at the end of April. At that time, we can see if the appetite for US debt issuance has grown again.

edit/new