Source: Wall Street News

Author: Li Dan

The NASDAQ closed down 1.8%, and S&P fell more than 1% on both days, the biggest two-day decline since Silicon Valley Bank went out of business. The Dow fell six times in a row, and Salesforce fell more than 7% to lead the decline in constituent stocks. Tesla closed down 5.6% to an 11-month low, leading the decline of the “Seven Sisters” of technology. Nvidia closed down 2.5% after rising nearly 3% in early trading; Goldman Sachs closed up nearly 3% after reporting earnings; and the mining stock Alcoa rose nearly 4%. China's stock index rose more than 1% in early trading and then turned down, hitting a new low in February. NIO closed down more than 5%, and Xiaopeng Motors fell more than 3%. After the US retail data was released, the yield on ten-year US Treasury bonds rose more than 10 basis points, breaking 4.60% for the first time in five months; the US dollar index jumped to a new five-month high, and the yen hit a new low since 1990 for 4 days. Offshore RMB intraday gains recovered at 7.26. Bitcoin surpassed $4,000 and fell below $63,000 in the intraday period. Crude oil retreated, but after falling close to 2% in the intraday period, it smoothed out most of the losses. Gold rose nearly 3% in the intraday period, and the three-day earnings hit a record high. Lun Aluminum rose more than 2%, hitting a 14-month high, while Luntong rose more than 1%, and hit a new high in the past two years.

As announced on Monday, retail sales in the US rose 0.7% month-on-month in March, down from the 0.9% growth rate after the February revision, and still significantly stronger than the expected 0.4% growth rate. The commentator believes that the data shows the resilience of the economy and stimulates market expectations that the Federal Reserve is not in a hurry to cut interest rates.

After the retail data was released, the price of US Treasury bonds, which rebounded last Friday as risks in the Middle East intensified, fell at an accelerated pace, and yields returned to an upward trend. The benchmark 10-year US Treasury yield rose above 4.60% for the first time in five months. The interest rate sensitive two-year US Treasury yield rushed to the 5.0% mark, approaching the nearly five-month high set last week. Furthermore, the media said that J.P. Morgan Chase and Wells Fargo, which released financial reports last Friday, will issue senior corporate bonds, which may set off a wave of bonds issued by major Wall Street banks, and also promote a rise in US bond yields.

New York Federal Reserve Chairman Williams, the “top three” of the Federal Reserve, said on Monday that if inflation continues to slow, the Federal Reserve may start cutting interest rates this year. Goldman Sachs's performance is improving, and all support major US stock indexes to open higher. However, at a time when US bond yields are picking up, the situation in the Middle East once again hit US stocks hard, and the three major stock indexes turned down in the middle of the day. According to CCTV and other media reports, the Israel Defense Forces Chief of General Staff said that Iran's weekend attacks on Israel “will be responded to”; the Israeli government's wartime cabinet meeting on Monday determined that it would fight back against Iran and continue to meet on Tuesday to discuss counteractions.

The decline in tech giants put pressure on the market. The Nasdaq Index recorded its worst single-day performance since the US CPI slumped expectations of interest rate cuts in January, and S&P recorded the biggest two-day decline since the Bank of Silicon Valley went out of business last year. Nvidia, Microsoft, and Meta all fell after rising at least 1% in the intraday period. After the media said that Tesla would lay off more than 10% of its global workforce and set the highest layoff ratio in the company's history, Tesla fell by more than 5%, the biggest daily decline since poor fourth quarter results were announced at the end of January. However, Goldman Sachs maintained its upward trend and rebounded against the market, when profits and revenue surged by double digits in the first quarter. Mining stocks such as Alcoa rose after the US and British governments announced measures to restrict trading in Russian copper, aluminum, and nickel products.

On the foreign exchange market side, after the US retail data was released, the US dollar index quickly erased the daily decline and turned upward. After breaking through 106.00 for the first time since November last Friday, it further climbed to a five-month high. Non-US currencies generally declined in the intraday period, and the yen fell below 154.00 against the US dollar, hitting a new low since 1990 for four consecutive trading days. Investors remained highly wary of the Japanese government interfering in the foreign exchange market. Japan's finance minister, Suzuki Shun, said earlier on Monday that he is closely monitoring foreign exchange fluctuations and that the Japanese government is fully prepared to take action. Bitcoin accelerated its decline after Israel said it would respond to Iran's attack. It fell below 63,000 US dollars in the intraday period, down 4,000 US dollars from a daily high, and fell below the low level of more than three weeks created by 61,000 US dollars after not being able to escape the Iranian attack over the weekend.

Among commodities, the ban on trading of Russian metals between the US and Britain boosted the rise of various basic metals in London. Lunan aluminum spearheaded the rise, hitting a new high in more than a year, and Luntong continued to hit a new high for almost two years. With the risk of the escalation of the conflict between Israel and Iran, gold turned up in the intraday period. At one point, it rebounded nearly 3% from a daily low. Both spot gold and New York futures set new closing records; international crude oil failed to maintain last Friday's rebound, but after falling close to 2% in the intraday period, it smoothed out most of the decline.

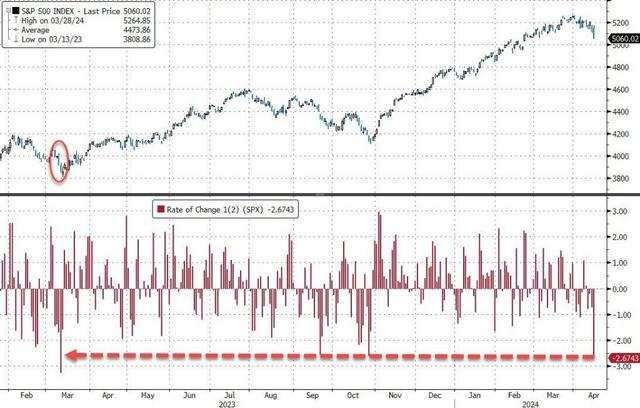

S&P created the biggest two-day decline since Silicon Valley Bank went out of business, the Dow fell six times in a row, Tesla led the decline, and technology's “Seven Sisters” surged after Goldman Sachs's earnings report, and mining stocks rose

The three major US stock indexes collectively opened higher and fell sharply in midday trading. The Nasdaq Composite Index, which rose more than 0.7% at the beginning of the session, turned down in early trading. It fell more than 1.9% in midday trading, and the S&P 500 index, which had risen nearly 0.9% in early trading, turned down at the beginning of midday trading and fell nearly 1.4% at one point. The Dow Jones Industrial Average rose slightly more than 400 points and rose nearly 1.1% at the beginning of the session. After the NASDAQ and S&P declined, it also turned down in midday trading. It once fell more than 320 points and fell nearly 0.9%, and finally closed down collectively for two consecutive trading days.

The NASDAQ closed down 1.79%, the biggest drop since the US January CPI was announced on February 13, at 15885.02 points, breaking the closing low since February 21. S&P closed down 1.2%, falling more than 1% for two consecutive days, and falling 2.6% for two days, the biggest two-day decline since Silicon Valley Bank went out of business on March 10, 2023, at 5061.82 points, breaking the closing low since February 21, and falling below the 50-day EMA for the first time in five months. The Dow fell for six consecutive trading days, falling 248.13 points, or 0.65%, to 37735.11 points, breaking the closing low since January 18.

The small-cap stock index Russell 2000, which is mainly value stocks, closed down 1.37%, falling for two consecutive days until February 13. The tech-heavy Nasdaq 100 Index closed down 1.65%, falling more than 1% on two days, breaking the low since February 21. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the NASDAQ 100 index, closed down 1.9%, falling nearly 2% on both days, breaking the low since March 15.

Among the constituent stocks of the Dow Index, the media said that after it negotiated the acquisition of data management company Informatica, cloud software giant Salesforce (CRM) closed down 7.3%, the biggest decline since December 2022, far exceeding that of Apple, which ranked second; Goldman Sachs had the highest increase.

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the tech giants “Seven Sisters” had mixed ups and downs in early trading and fell all at noon. Tesla had the worst performance when news of global layoffs spread. The stock price opened low. It fell nearly 5.7% in midday trading and closed down 5.6%, the biggest drop since the first day after the fourth quarter earnings report was announced on January 25, and fell two consecutive days until May 4, 2023.

Among FAANMG's six major technology stocks, Meta and Netflix, which rose more than 1% at the beginning of the session, closed down about 2.3% and 2.5%, respectively. Microsoft and Amazon, which had risen more than 1% at the beginning of the session, closed down nearly 2% and 1.4%, respectively, breaking the lows since March 11 and April 4, respectively; Alphabet, which had risen 1% in early trading, closed down 1.8% to a new one-week low; and Apple, which opened low, closed down 2.2%, falling to the closing high since March 20, which had risen by two consecutive gains last Friday.

Chip stocks generally turned down during the intraday period. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX, which fell back to March 19 last Friday, rose more than 1.7% at the beginning of the session. After turning down in midday trading, they closed down nearly 1.4% and 1.3%, respectively, and fell for two consecutive days until the closing of February 28. Among chip stocks, Nvidia, which closed down nearly 2.7% last Friday, rose nearly 2.8% in early trading, and closed down nearly 2.5% after turning down in midday trading, approaching the closing low since March 11, set on Tuesday, April 9. Intel and AMD, which plummeted more than 5% and 4% respectively on Friday, had mixed performance. Intel closed up 1.7%, while AMD closed down 1.8% after the initial decline; at the close, Arm fell more than 3%, Broadcom fell more than 2%, and TSMC US stocks fell more than 1%.

Bank stock indices had mixed ups and downs. The overall banking index, the KBW Bank Index (BKX), rose 2.7% at the beginning of the session, recovering 0.3% in midday trading, and rebounded after falling for three consecutive days to a low level since March 15; the regional bank index KBW Nasdaq Regional Banking Index (KRX) and the regional bank stock ETF SPDR S&P Regional Bank ETF (KRE) all closed down nearly 0.4%, both falling for two consecutive days.

Among the major banks, Goldman Sachs shares rose more than 2% in early trading and closed slightly higher than expected by 28% and 16%, respectively, after announcing transactions and investment banking, which surged by 28% and 16% year-on-year, respectively. Wells Fargo Bank, which closed down slightly by 0.4% after last Friday's earnings report, rose more than 2% at the beginning of the session and closed up 0.8%. Citi turned down in early trading and closed down 1.8%.

The US and Britain imposed a trading ban on Russian metals. Many mining stocks surged in early trading. Century Aluminum (CENX) rose more than 10%, Aluminum (AA) rose nearly 7%, Freeport-McMoRan (FCX) rose more than 3%, and 7.7%, 3.9%, and 1.1% respectively at the close, while Caesar Aluminum (KALU), which had risen nearly 4% in early trading, closed down nearly 0.4%.

Popular Chinese securities generally followed the mid-market decline. The Nasdaq Golden Dragon China Index (HXC) rose nearly 1.5% at the beginning of the session and closed down nearly 0.5%. After falling sharply by nearly 4.6% last Friday, it hit a new closing low since February 13. China's general ETFs KWEB and CQQQ closed down nearly 0.6% and slightly, respectively. The three new car builders turned down at the beginning of the market. At the close, NIO Auto fell by more than 5%, Xiaopeng Motor fell by more than 3%, Ideal Auto fell by more than 2%, while Xiaomi Fan alone rose by nearly 2%. Among other individual stocks, at the close of trading, Ehang Intelligence fell more than 3%, Station B fell nearly 2%, Baidu and Pinduoduo fell more than 1%, Alibaba dropped nearly 1%, and Tencent's fan list fell nearly 0.6%. After the media said that Liu Qiangdong would soon launch a live broadcast on the JD App and adopt a new format, JD rose more than 3% at the beginning of trading, closing up 0.1%, and NetEase rose slightly.

The 10-year US Treasury yield rose more than 10 basis points in the intraday period and rose above 4.60% for the first time in five months

The yield on the US 10-year benchmark treasury bond hit a new high since November last year on the third day of the last four trading days. After the US retail sales data was released, it quickly rose above 4.60% for the first time since November 2023. The US stock market rose above 4.66% in early trading, continuing to refresh the high level since November 13, 2023. It rose by about 14 basis points during the day, about 4.60% at the end of the bond market, and rose by about 8 basis points during the day.

The 2-year US Treasury yield, which is more sensitive to interest rate prospects, fell 4.89% when it was low in early Asian trading and rose 4.98% after retail data was released. It was extremely close to breaking 5.0% to 4.9929 in early trading, breaking 5.0% last Thursday and the high since November 14, 2023, set for two consecutive days. It rose nearly 10 basis points during the day, gradually rebounded by more than half of the increase in midday trading.

After retail data, the US dollar index jumped to a five-month high, and the yen hit a new low since 1990 for 4 days, Bitcoin once exceeded 4,000 US dollars

The ICE US Dollar Index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, fell below the daily low of 105.90 in the European stock market, fell nearly 0.2% during the day. After US retail sales were announced, the US stock rose again at the beginning of the session and rose above 106.20 in early trading. After hitting a new high since November 3, 2023 in the early trading session, it also refreshed its high since November 1, 2023. It also rose nearly 0.2% during the day. At the end of early trading, it turned down for a short time, and increased again at noon.

By the close of the US stock market on Monday, the US dollar index was above 106.20, up nearly 0.2% during the day; the Bloomberg US Dollar Spot Index, which tracks the exchange rate of the US dollar against ten other currencies, rose nearly 0.2% during the day, breaking the same high level since November 13, 2023 for three consecutive trading days, and the US dollar index for 4 consecutive days, making it the biggest four-day increase since February 2023.

Among non-US currencies, the yen continued to hit a new intraday low since 1990. USD/JPY rose above 154.40 in early trading, hitting a new high since 1990 for the fourth consecutive trading day, rising nearly 0.8% during the day, and US stocks closed above 154.20; EUR/USD had a lower side of 1.0620 in early morning trading, breaking the low since the end of October 2023 set last Friday, falling 0.2% during the day. US stocks closed above 1.0620; GBP/USD fell below 1.2440 in midday trading, approaching a new refresh on Friday 2023 November 17 At a low level since then, US stocks closed above 1.2440.

The offshore renminbi (CNH) basically maintained a downward trend against the US dollar on Monday. It only rose in the short term and reached a new daily high of 7.2548 in early Asian trading, rising 125 points during the day. European stocks fell to 7.2680 before the market, approaching the low level since March 25, which was refreshed last Friday, and then turned higher. At 4:59 Beijing time on April 16, the offshore RMB was 7.2590 yuan against the US dollar, up 83 points from the end of last Friday's session in New York, and rebounded after falling back last Friday.

Bitcoin (BTC) rose above $66,800 to a new daily high in early trading in European stocks. The decline accelerated after the opening of the US stock market. It fell below $63,000 to below $62,400 in midday trading, falling more than 4,000 US dollars and falling nearly 7% from the daily high. It failed to continue to break from the low level since March 20, which was refreshed at $61,000 over the weekend. US stocks hovered around the $63,500 line at the close of trading and fell more than 1% in the last 24 hours.

Crude oil retreated, but after falling close to 2% in the intraday period, it smoothed out most of the declines

International crude oil futures were generally declining on Monday; only the Asian market turned upward in the short term in early trading. When US stocks hit a new daily low in early trading, US WTI crude oil fell to 84.00 US dollars and fell nearly 1.9% during the day. Brent crude oil fell below 88.80 US dollars, fell 1.9% during the day, and then rebounded. US stocks were close to erasing all losses in midday trading.

In the end, crude oil, which rebounded last Friday, all closed down. WTI crude oil futures for May closed down $0.25, or 0.29%, to $85.41 per barrel, and began falling to the closing low since April 1, which was refreshed last Thursday; Brent crude oil futures for June closed down $0.35, or 0.39%, to $90.10 per barrel, holding the $90 mark, and closed above $90 for two consecutive days.

Lunan aluminum rose more than 2%, and copper hit a new high in the past two years, gold rallied nearly 3% in the intraday period, and the revenue reached a record high in three days

London basic metals futures mostly rose on Monday. Lun Aluminum, which led the rise, rose more than 2%, breaking the high level since February last year set by the rebound last Friday. Luntong and Lunn Lead also rose for two days. Luntong also rose more than 1%, continuing to hit a new high since June 2022, and Lunlead rose to a high level since November last year. After two days of continuous decline, Lunnickel rebounded and did not continue to fall below the four-week high level previously set by eight consecutive days of gains. Meanwhile, lunzine fell close to 2%, falling to the highest level since April last year, which had been rising for five days. Renxi, which rebounded last Friday to a high level since June 2022, also retreated.

When US stocks hit a new low in early trading, New York gold futures fell to 2340.2 US dollars, falling more than 1.4% during the day. Spot gold fell below $2,325 to a new daily low, falling more than 0.8% during the day, and continued to rise after turning higher in midday trading. By the close, COMEX gold futures rose 0.37% to 2,383 US dollars/ounce in June, setting a record high for three consecutive trading days.

Futures rose to a new daily high of $2404.3 at the end of the session, rising nearly 1.3% during the day. Spot gold rose above $2,387. Spot gold rose more than 1.8% during the day, up more than 2.7% and about 2.7% from the daily low, respectively, but failed to hit the new intraday record highs each set last Friday.

At the close of the US stock market, spot gold was above 2,380 US dollars, rising nearly 1.8% during the day, lower than the daily rate, breaking the record high set during the same period last Thursday.

Editor/Jeffy