Source: Securities Times Author: Qin Yanling

For the first time on record, the inversion between personal housing loan interest rates and corporate loan interest rates has come to an end.

According to the latest data from the People's Bank of China, interest rates on newly issued loans remained at a historically low level in March 2024. Among them, the weighted average interest rate for new corporate loans in March was 3.75%, 1 basis point lower than the previous month and 22 basis points lower than the same period last year; the interest rate for new personal housing loans was 3.71%, 15 basis points lower than the previous month, and 46 basis points lower than the same period last year.

It is worth noting that this is the first time since public records became available that interest rates on newly issued personal housing loans were lower than the weighted average interest rate for newly issued corporate loans.

Interest rates on personal housing loans were lower than interest rates on corporate loans for the first time

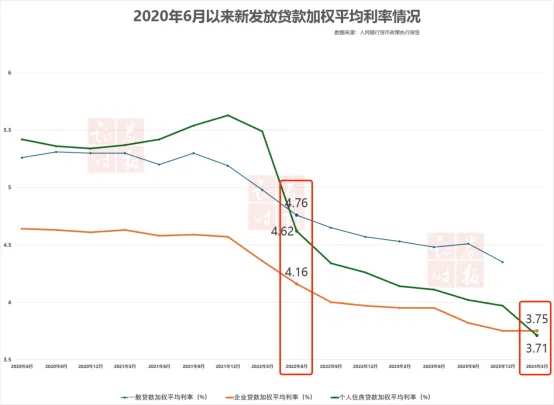

In the monetary policy implementation report for the second quarter of 2020, the People's Bank of China disclosed the weighted average interest rate for corporate loans for the first time. The report at the time showed that in June 2020, the weighted average interest rate for corporate loans was 4.64%, down 0.48 percentage points from December of the previous year, clearly exceeding the LPR decline in the same period, which is conducive to reducing corporate financing costs.

Since then, the weighted average interest rate on loans to newly issued enterprises has declined steadily. According to the monetary policy implementation report published by the People's Bank of China on a quarterly basis, the weighted average interest rate for corporate loans remained around 4.5% to 4.65% from June 2020 to December 2021.

Entering 2022, the weighted average interest rate for all loans has decreased.

The first monetary policy implementation report of this year (first quarter of 2022) indicates that in recent years, the People's Bank of China has achieved remarkable results in promoting the improvement of the modern monetary policy framework through measures such as improving market-based interest rate formation and transmission mechanisms.

In August 2019, the People's Bank of China issued an announcement to reform and improve the loan market quoted interest rate (LPR) formation mechanism. The reformed LPR is formed by quoting banks comprehensively considering market interest rate trends and market-based quotes based on reference to medium-term loan facilitation (MLF) interest rates.

“(After the LPR reform) not only raised the degree of marketization of loan interest rates, but also formed a transmission mechanism of 'market interest rate+central bank guidance → LPR → loan interest', and the transmission efficiency of monetary policy has improved markedly.” The People's Bank of China pointed out that since then, interest rates for new loans have basically been priced with reference to LPR.

In the same report, the People's Bank of China also stated that since the LPR reform in August 2019, the weighted average interest rate for corporate loans fell from 5.32% in July 2019 to 4.36% in March 2022, with a cumulative decline of 0.96 percentage points, exceeding the 0.55 percentage point decline in LPR during the same period, which has strongly contributed to a marked and continuous decline in actual loan interest rates, which has greatly alleviated the problem of difficult and expensive financing for small and micro enterprises that have been plagued for a long time.

In terms of interest rates on personal housing loans, in June 2022, the average interest rate for newly issued personal housing loans was 4.62%. For the first time since public records were made, it was lower than the weighted average interest rate for general loans.

The People's Bank of China pointed out that throughout 2022, the cost of corporate financing and personal consumer credit declined steadily. The annual weighted average interest rate for corporate loans was 4.17%, down 0.34 percentage points from the previous year. The average interest rate for new personal housing loans issued in December was 4.26%, down 1.37 percentage points from December of the previous year.

Since then, the cost of corporate financing and personal consumer credit has continued to decline. By September 2023, the weighted average interest rate for newly issued corporate loans fell to 3.82%, while the weighted average interest rate for newly issued personal housing loans reached around 4%, reaching 4.02%. By December 2023, the weighted average interest rate for newly issued corporate loans and the weighted average interest rate for personal housing loans had all dropped below 4%.

In March 2024, interest rates on newly issued personal housing loans fell below the weighted average interest rate for newly issued corporate loans for the first time since public records were made, reaching 3.71%.

There is still room for lower interest rates on personal housing loans

Interest rates on new personal housing loans continue to fall, as a result of the combined effects of the market and policy.

From a policy perspective, in November 2022, the People's Bank of China and the former Banking Insurance Regulatory Commission jointly issued the “Notice on Accomplishing the Current Financial Work to Support the Stable and Healthy Development of the Real Estate Market”, or “Financial Rules 16”, which clearly states that all regions are supported to implement differentiated housing credit policies based on national policies, reasonably determine the down payment ratio and lower limit of loan interest rate policies for local personal housing loans, and support rigid and improved housing needs.

In January 2023, the People's Bank of China, in conjunction with the former Banking Insurance Regulatory Commission, also issued the “Notice on Establishing a Long-Term Mechanism for Dynamic Adjustment of Interest Rate Policies for the Issuance of Personal Housing Loans for the First Home”, which proposes that cities where sales prices of newly built commercial residential homes have declined for 3 consecutive months from month to month can maintain, lower or cancel the lower limit of the local first housing loan interest rate policy in stages. It provides policy space for lowering interest rates on personal housing loans.

In September 2023, the People's Bank of China and the General Administration of Financial Supervision made further policy arrangements. Starting from September 25, 2023, borrowers of commercial personal housing loans with the first housing unit in stock can apply to the lending financial institution, and the financial institution will issue a new loan to replace the first commercial personal housing loan for the first home in stock. Since then, various banks have successively announced the adjustment rules.

According to data from the People's Bank of China, by the end of September 2023, interest rates on stock mortgages of over 22 trillion yuan had been lowered. The adjusted weighted average interest rate was 4.27%, an average drop of 73 basis points, reducing borrowers' interest expenses by 160 billion to 170 billion yuan each year, benefiting about 50 million households and 150 million people. At the same time, out of 343 cities across the country (prefecture level and above), 119 cities that meet the conditions for easing the lower limit of the first home loan interest rate policy have all relaxed the lower limit. Of these, 95 have lowered the lower interest rate limit for the first home loan. The lower limit implemented by these cities is 10-40 basis points lower than the national lower limit; 24 have lifted the lower limit.

Recently, the number of cities that have phased out the lower interest rate limit for commercial personal housing loans for the first housing unit has shown a clear upward trend. More than 10 cities, including Qingdao, Nanchang, Jining, Chaozhou, Yantai, and Shanwei, announced that starting April 1, the lower interest rate limit for commercial personal housing loans for the first housing unit will be phased out.

Currently, industry researchers believe that there is still room and possibility for interest rates on personal housing loans to be lowered in the future.

Chen Wenjing, director of market research at the China Index Research Institute, believes that overall, lowering mortgage interest rates is currently one of the important measures to release demand for home purchases, and it is expected that more cities will follow suit in the future.

Wang Qing, chief macro analyst at Dongfang Jincheng, also said that the next step is to push the real estate industry to achieve a soft landing. In addition to easing purchase restrictions in an orderly manner, the key is to guide residents' mortgage interest rates to an effective decline, and to send a clear policy signal to the market. That is, until the property market recovers steadily, the process of lowering mortgage interest rates will not stop, and the decline will increase more and more. This is a key measure to reverse current expectations in the property market, and it is also the main driving force for the next step in stabilizing the property market policy. The price of LPR for a term of 5 years or more was drastically lowered in February, which has already released a policy signal in this regard.

edit/lambor