Source: Xuetao's Macro Notes

Authors: Song Xuetao, Li Mengying

Commodity prices don't lie. Oil prices and copper prices truly reflect that America's inflation cycle and manufacturing cycle are picking up. The grand story of gold will not be broken for some time to come. Commodity de-dollarization is the primary principle of gold pricing.

Since the beginning of the year, there has been a considerable increase in globally priced commodity prices. Since the beginning of the year, the price of gold has increased by 16%, the price of oil by about 23%, and the price of copper by about 9%.

Moreover, recently they have all broken through some key positions. For example, copper has broken through 9,000 US dollars/ton, Brent oil has exceeded 90 US dollars/barrel, and gold has reached a record high. This is also the reason why the recent rise in commodity prices has attracted market attention.

Commodity prices, especially spot prices, simply reflect the fundamental supply and demand relationship. Futures prices include future supply and demand expectations and liquidity factors, and there are some deviations from spot prices.

Commodity stocks tend to have a greater degree of deviation, because stocks are second-order derivative pricing of demand and pay more attention to the slope and sustainability of demand, so commodity stock prices are often more nonlinear than commodity prices.

In addition, there is still a problem with commodity stocks. Whether it is gold or copper, a company usually produces more than one type of mineral, and the diversification of revenue sources also makes the trend of gold stocks and copper stocks not as simple as commodity prices.

Currently, the three commodities that the market is most concerned about — crude oil, copper, and gold — have such different pricing factors.

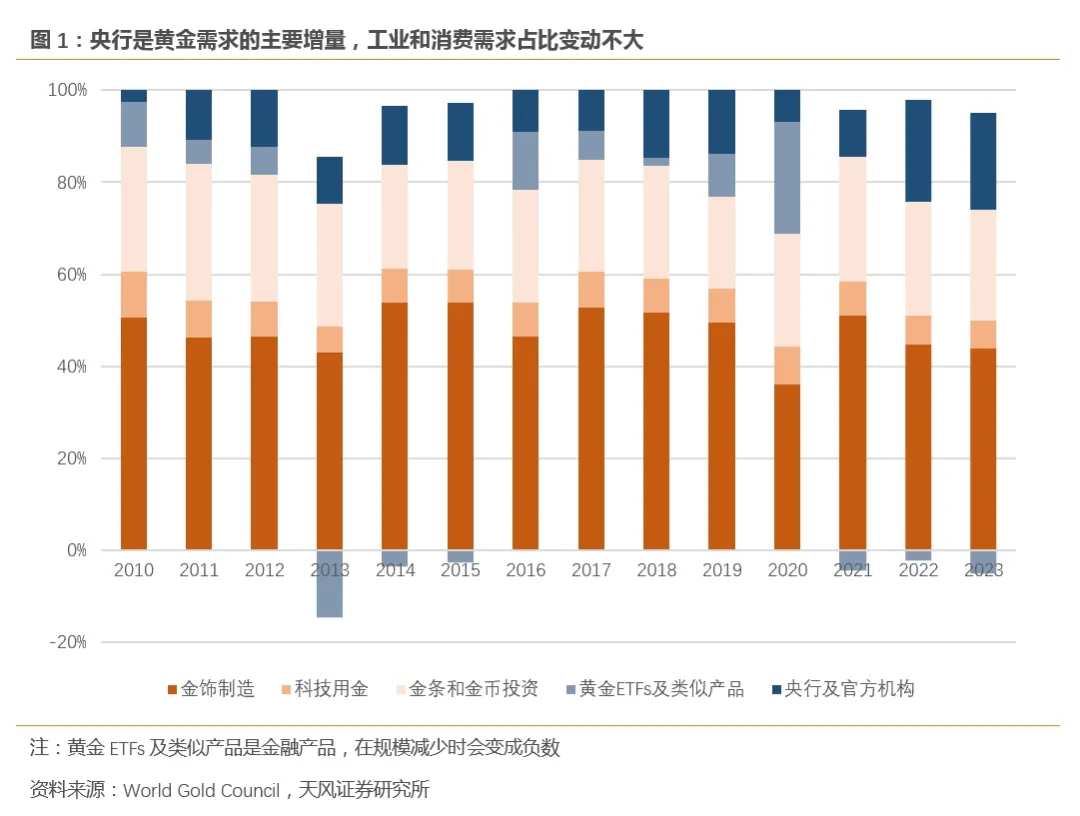

The price of crude oil almost always comes from its commodity properties. The price of gold also mainly comes from its financial attributes. Although gold also has some industrial and consumer demand, its share of total demand for gold hardly fluctuates.

However, copper is between crude oil and gold, and pricing has both commercial and financial attributes. Although copper's financial properties are not comparable to gold, it is still far superior to non-ferrous metals such as aluminum, zinc, and nickel.

Commodity attributes, financial attributes, plus monetary attributes unique to gold and silver — make up the pricing spectrum of commodities.

(1) Oil and copper, it's only strange if they don't rise

Crude oil is known as the “mother of inflation” because oil prices are highly correlated with US inflation expectations. When oil prices rise, US inflation expectations will follow.

Copper is known as the “mother of the cycle” because copper prices are highly related to the global manufacturing cycle. As the global manufacturing industry begins to replenish inventories, demand for core commodities such as automobiles, electronics, home appliances, and real estate chains will often drive up copper prices.

Therefore, crude oil is mainly related to US consumer demand, and copper is mainly related to the US manufacturing cycle. These two commodities respectively represent US inflation and cycle.

Copper and oil prices have recently broken through key positions, mainly because the US economy and inflation have not only exceeded market expectations, but also created new expectations of economic overheating and re-inflation.

Although China's manufacturing PMI also exceeded expectations in March, apart from the disturbances caused by seasonal adjustments, the main driver was a sharp rise in the new export orders index. The US manufacturing PMI has bottomed out and rebounded since the middle of last year. In March, the US ISM manufacturing PMI returned above 50.

As stated in our previous article — the US manufacturing cycle began a new boom cycle in the 3rd quarter of last year.

Beginning in the third quarter of last year, the US manufacturing inventory cycle showed signs of bottoming out. The wholesaler inventory ratio in most industries began to fall back from the top, indicating that the whole industry has entered a passive inventory removal cycle, while some industries that began removing inventory at the end of 2021 have already begun to actively replenish inventory in the fourth quarter of last year.

In addition to the recovery in the US manufacturing PMI, many data also show that the US economy is in the midst of a strong recovery. For example, new jobs continue to recover, wage growth is stable at 4% year over year, actual income of residents continues to improve, corporate profits remain strong, and non-residential investment is growing rapidly.

As a result, it is not surprising that oil and copper prices have risen.

(2) Under normal circumstances, this year is not a big year for oil prices

However, this year should not be a year where oil prices continue to be high.

On the demand side, the world needs more than 100 million barrels of crude oil every day, with the US first and China second. If American demand is good and Chinese demand is good, there is a tight balance between supply and demand.

US demand in the first quarter of this year increased by 400,000 b/d to 2020 million b/d over the same period last year, while China's demand remained low at about 15 million b/d in the first quarter, so there was not much pressure to increase the price of crude oil from the demand side.

On the supply side, US shale oil production was overproduced this year. According to the US Energy Information Administration (EIA), crude oil production in major US shale oil producing regions reached 9.7 million b/d, the highest level since December 2023.

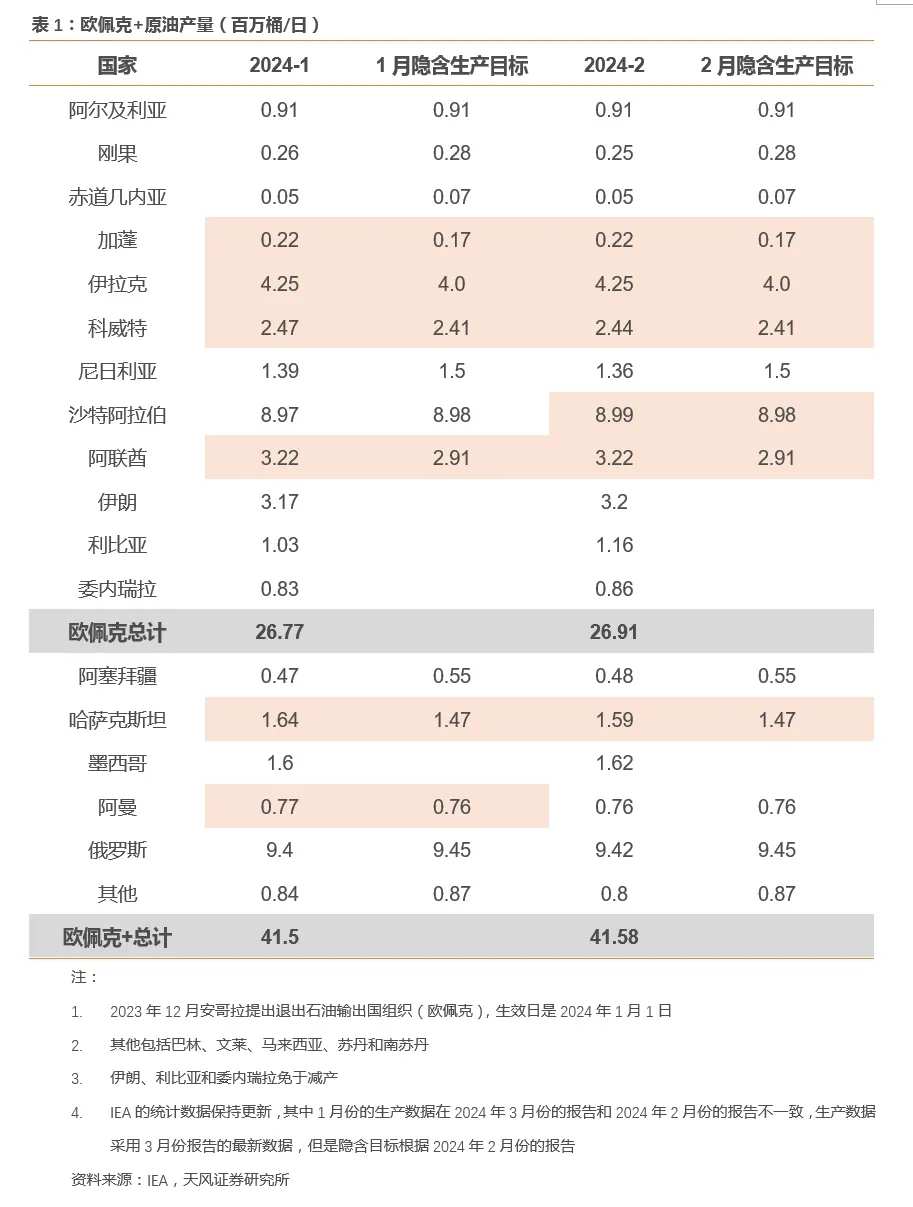

For the purpose of preserving oil prices, OPEC+ 2024Q1 reduced production by a total of 2.2 million b/d. In March of this year, it was announced that voluntary production cuts will be extended until the second quarter. However, in reality, OPEC+ did not cut production drastically, and some countries did not strictly implement production reduction plans, such as Gabon, Iraq, Kuwait, the United Arab Emirates, and Kazakhstan (see Table 1).

With crude oil slightly overproduction, U.S. crude oil inventories have gradually rebounded since the fourth quarter of last year. Strong consumer demand in the US will drive oil prices to rise slightly this year, but without the continued influence of supply factors, it will not support high oil prices throughout the year.

For the US, 780 US dollars/barrel is also a relatively comfortable oil price level. Because the cost of US shale oil is about 560 US dollars/barrel, oil prices above 60 US dollars are very friendly to US oil and gas companies.

However, oil prices must not be too high. The sensitivity of US inflation will rise after the oil price rises above 80 US dollars, so in the absence of supply conflicts, the US will try to keep oil prices around 780 US dollars. This basically determines the center of oil prices this year.

However, the factors fueling the recent rise in oil prices are mainly on the supply side, and some geopolitical events have escalated.

The first is Russia and Ukraine. Russia is the world's largest producer of crude oil, ranking third in the world in terms of production in 2023, with a daily production volume of more than 10 million barrels. Recently, Russia and Ukraine attacked each other's energy infrastructure, leading to an increase in supply risks.

The second is Palestine and Israel. The Mander Strait, which has received much attention in the Israeli-Palestinian conflict, is the entrance to the Red Sea and the throat of oil and gas shipping between Europe and Asia. If there is a problem with this line, the impact on the oil cloth is greater than WTI.

Last year, the Houthis attack deliberately circumvented oil tankers, but now Israel's attacks on Syria and Iran and possible retaliation have caused a sudden rise in concerns about the energy supply crisis caused by the conflict between Palestine and Israel.

Generally speaking, this year is not a big year for oil prices. 780 US dollars is a normal central level of oil prices, but this year's oil prices are also easily stimulated by uncontrollable geopolitical events, releasing huge volatility in the short term.

(3) Copper is a product with a story

Copper is a product with a story, and there are stories to tell on both the demand side and the supply side.

On the demand side, the long-term story of copper is the transformation of old and new energy systems. Because to reduce the share of non-fossil energy consumption, it is necessary to increase the proportion of energy converted into electricity once. Whether it is generating, transmitting, or using electricity, or electric vehicles replacing fuel vehicles, copper can tell a long-term story on the demand side, so there is a saying “copper is the oil of the new era.”

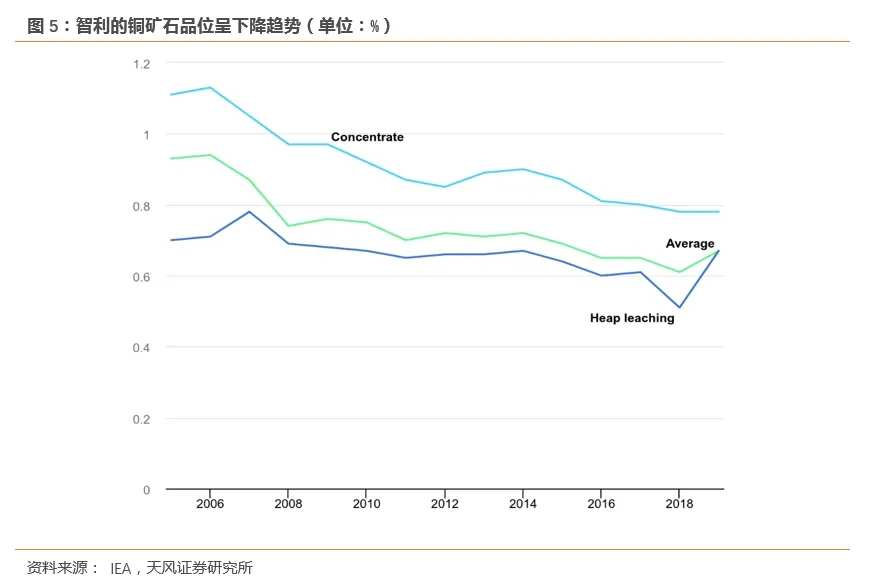

On the supply side, the long-term story of copper is that the grade of fine copper ore continues to decline. Over the past decade, copper grades in a few major producing countries have declined by an average of about 25%. As the grade decreases, so does the corresponding operating cost.

The short-term story of copper is that copper mining is usually distributed in South America, Africa and other places where the level of government governance is unstable, and supply is easily disrupted. For example, the Chilean copper trade union strike in 2021 triggered a sharp rise in copper prices, but it was also supported by a tight balance between supply and demand at the time, and after 2022, there was excess capital expenditure on copper, and copper prices were sluggish for a while.

Therefore, whether the supply-side story can be effective depends fundamentally on whether the demand side cooperates.

Starting in the second half of 2024, copper supply and demand may begin to be tight again. At this point, it is “story time” for copper again. Although China accounts for half of the world's copper consumption, due to the high concentration of the supply chain, the pricing power for copper is still dominated by overseas, and it has certain financial attributes.

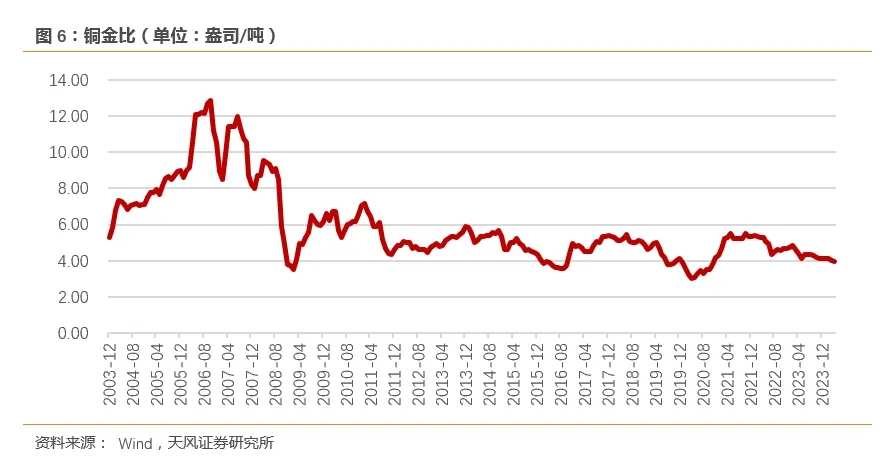

Due to financial attributes, the price ratio between copper and gold has a relatively fixed fluctuation range. Once the price of gold rises significantly, the copper price will follow even if it is not driven by liquidity. After the recent rise in gold prices, the price ratio of copper to gold has reached a low level in three and a half years, and the financial pricing of copper has begun to take effect.

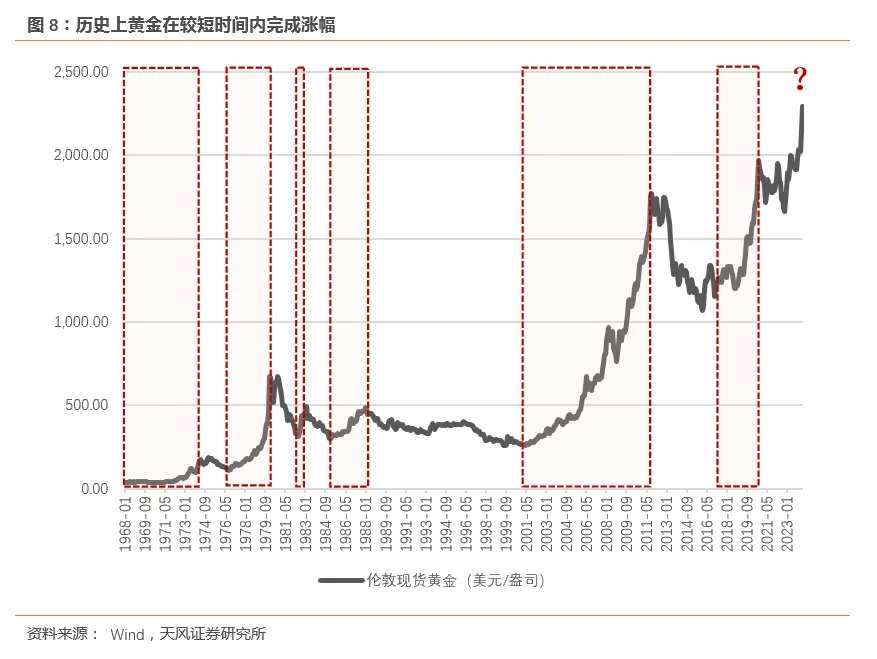

(4) When it comes to gold, you can't deny the importance of a “grand narrative”

Gold is both simple and complex.

The simplicity of gold is that the underlying logic is very clear — since February 24, 2022, gold will no longer be an equivalent substitute for the dollar.

When the US froze Russia's foreign dollar assets, the credit of the reserve currency system began to dissipate rapidly. Some important central banks have begun to reduce their monetary reserves and increase their gold reserves. The country where the central bank increased its gold reserves the most last year, while the developed country that increased its gold reserves the most was Singapore.

Because Singapore is a neutral country that is very sensitive to international trade and international order, there is a strong incentive to reduce its risk exposure to the modern monetary credit system. The alternative to the monetary credit system is the commodity credit system, and the era of “bartering for goods” has begun to return.

Therefore, there are always people who ask, if the Federal Reserve does not cut interest rates and the US dollar strengthens, why is gold still rising? Because gold and the US dollar are no longer equivalent substitutes, the real interest rate on US bonds is no longer an opportunity cost of holding gold. What determines the price of gold now is monetary attributes, that is, the long-term pricing logic of gold plays a major role, replacing the medium-term pricing logic that was effective in the past — financial attributes.

After adding the gold reserve increments of central banks to the gold quantitative pricing model last year, we discovered that central banks' gold reserves have the most power to explain the gold price trend after February 2022, rather than the US bond TIPS interest rate that was effective in the past.

The complexity of gold is that strategies are highly homogenized — as a result, historically, the rise of gold often completed most of its gains in a few moments, and then did not rise or fall most of the time.

Simply put, when gold is bad to choose.

On the one hand, gold is very efficient at pricing geopolitical events; it often basically completes the pricing of safe-haven properties within a day or two. On the other hand, the rapid rise in gold often occurs when it is unnoticed and the level of congestion is low, while when the level of attention is high, it is often very uncost-effective due to overcrowding.

This characteristic determines that if you want to buy gold when no one is paying attention or attention, when gold is paying a lot of attention, you need to treat it carefully.

From an investment perspective, gold should be treated as an important allocation asset. The holding period needs to match the debt period, and the position needs to match the risk budget and target return. The purpose of the allocation is to reduce the volatility of the portfolio and enhance the robustness of the portfolio. However, gold must not be treated as a short-term speculation target; expect a game event like stocks to catalyze, rise as soon as you buy it, and choose the right time.

(5) Summary: Product prices don't lie

The price of oil and copper is a true reflection of the recovery in the US inflation cycle and manufacturing cycle.

Oil is the simplest commodity, and its financial properties are not strong. No matter what kind of supply factor impacts it, it will quickly be projected onto the spot price. This year's oil prices are moderate and will not continue to be high, but in the short term, oil prices will jump due to geopolitics and general elections.

The “storyline” of copper gives copper prices more room to play out, such as rising long-term demand, tight long-term supply, and financial attributes, etc., but whether the story works depends on whether short-term demand matches. The beginning of a new cycle in the US manufacturing industry gave copper a basis for storytelling, and the rise in gold prices also brought financial support to copper. Without extreme geopolitical events, copper prices fluctuate more than oil prices.

The grand story of gold will not be broken for some time to come. Commodity de-dollarization is the primary principle of gold pricing, just like in the 70s of the last century. In March of last year, our model predicted that the price of gold would reach 2,423 US dollars in a year, and it is expected that this target position will soon be achieved.

Risk warning

US inflation exceeds expectations; geopolitical friction intensifies; OPEC+ production cuts exceed expectations

Editor/Somer